DRDGold: Strong Torque To Rising Gold Prices

Summary

- The business model of DRDGOLD eliminates some of the risks faced by a typical miner.

- The relatively high AISC base of the company translates into higher torque in a rising gold price environment.

- The company is dealing with electricity supply problems in South Africa.

ayala_studio

The business of metals' production doesn't always come along with a mine. There are companies that don't own or operate any mines, but instead are specialized in tailings processing. One such company that I covered before is Amerigo Resources (OTCQX:ARREF) (ARG:CA), which extracts copper from mine waste. This business model is significantly less risky as it eliminates all sorts of risks related to operating a mine and usually offers significant torque to the price of the particular metal, due to relatively high AISC. In this article I'll present the case for DRDGOLD (NYSE:DRD) - a gold producer from South Africa, which extracts the material from tailings. The business model of the company has proved its resilience as shareholders have been receiving a dividend for 16 years in a row. Supported by its strong balance sheet with a net cash position, DRDGOLD is working towards reducing its energy dependence on Eskom. The relatively high AISC of US$1,432/lbs, while making the company vulnerable to falling gold prices, offers significant torque in a rising Au price environment.

Company overview

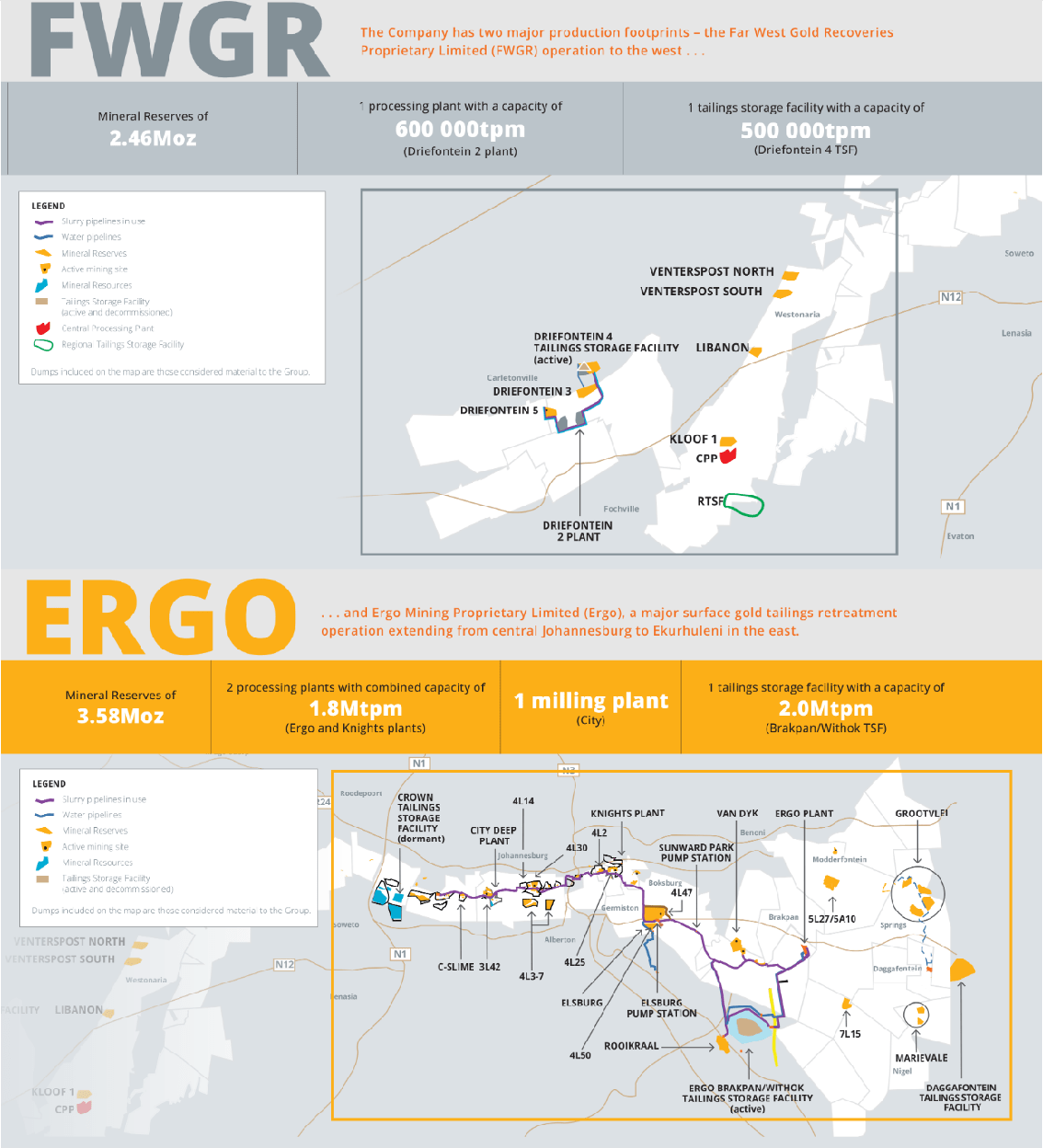

DRDGOLD's subsidiaries (DRDGold)

With corporate history dating back to the end of the 19th century, DRDGOLD has transformed from a typical miner into a tailings processing company. From 2020, the majority shareholder in the firm with 50.1% share is the PGMs major Sibanye Stillwater (SBSW). I deem this relationship as a positive as having a large and stable company as a backer could make improve access to capital. The operations of DRD are split between two subsidiaries - Ergo (1.8mtpm capacity) and Far West Gold Recoveries (0.5mtpm capacity) with combined processing capacity of 2.3mtpm.

Recent performance

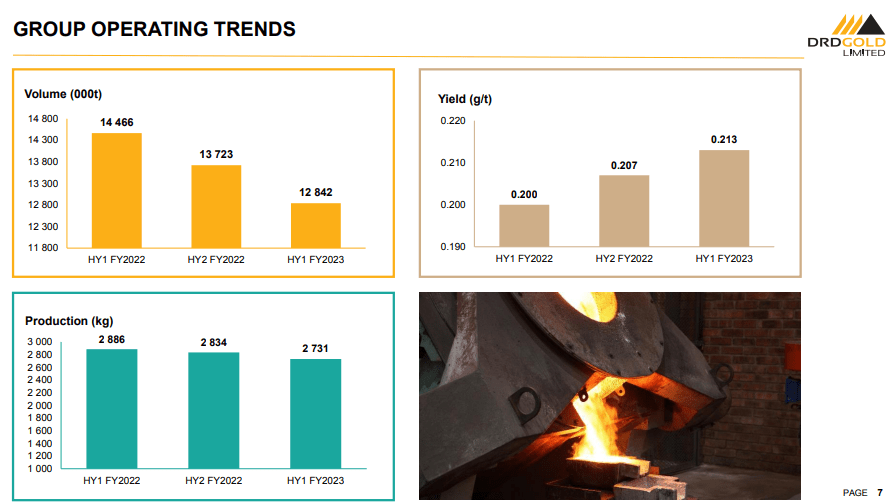

DRDGOLD's production highlights (DRDGold)

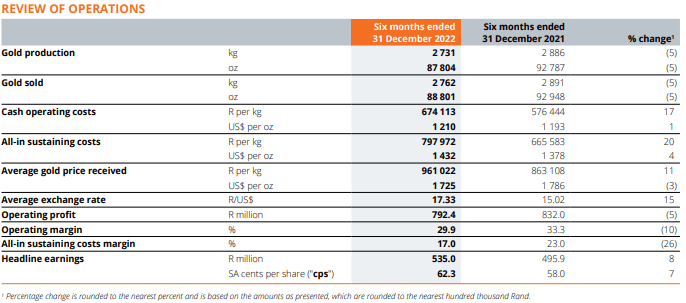

In the last 6 months of 2022 or H1'23 (DRDGold reports on a 6 months basis and its fiscal year starts and ends in June) the company processed 12.8m tonnes (-11.2% YoY) of tailings as electricity supply disruptions at Ergo led to lower volumes. However, rising gold grade to 0.213 g/tonne (+6.5% YoY) partially offset the drop in volumes and as a result gold production fell only by 5.4% YoY to 2,731kg or 87.8koz.

Financial highlights (DRDGold)

While realized gold price was also lower at US$1,725/oz (-3.4% YoY), lower depreciation and higher financial income led to an improved bottom line of ZAR535m (+7.9%). However, the depreciation of the ZAR to the USD led to inferior H1'23 earnings (US$30.9m, compared to US$33.0m in H1'22). The company also paid dividend of ZAR0.20/share (1ADR=10shares) or around US$0.11/ADR, bringing the annualized dividend yield to a bit below 2.5%. In terms of financial strength, the company is in a very solid position with no interest bearing debt and ZAR2.4B (US$138.0m) of cash and equivalents as of 31 December 2022.

Considerable gold price torque

As it can be seen from the performance table above, AISC of the company stands at US$1,432/oz as of H1'23. This figure is higher than what the average gold miner achieves and could pose a risk to DRD if gold prices deteriorate. However, in the opposite scenario of rising gold prices, DRD could outperform the industry. Let's take the example of one of the relatively low cost producers - Dundee Precious Metals (OTCPK:DPMLF) to demonstrate this in a hypothetical scenario. DPM's latest AISC amounts to US$1,008/oz, which on a realized price of US$1,725 will result in US$717/oz AISC margin. In the case of DRD this respective margin amounted to US$293/oz. If the realized price of gold humps to US$2,000/oz, holding all else equal will increase DRD's AISC margin by 93.9% to US$568/oz, while that of DPM should jump by 38.4% to US$992/oz. In terms of share price movements, it's logical to bet that companies will higher magnitude of margin improvements should yield superior returns.

Valuation discussion

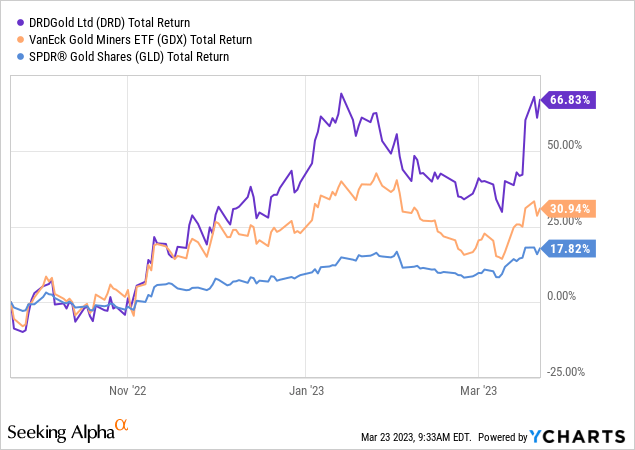

The data clearly indicates that in a rising gold price environment, DRD significantly outperforms the sector, represented by the VanEck Vectors Gold Miners ETF (GDX) as well as the commodity itself represented by the SPDR Gold Trust ETF (GLD).

While I'll refrain from putting an exact price target on DRD, my outlook for gold is bullish as central banks are beginning to deal with cracks in the financial sector, caused by the rate hikes, which makes me to believe that a pivot to quantitative easing is on the horizon. If gold breaches the US$2,000 level and goes towards its 2020 highs, it's not unreasonable to expect DRD to do the same.

Risks

As DRDGOLD itself stands on solid financial footing, I asses the risks to be mainly coming from the macro environment. Electricity supply issues have been something that the whole South African mining sector has to deal with. In that regard, DRD is executing an investment plan that will reduce its dependence on Eskom for electricity supply. DRD intends to self-fulfill part of its energy needs through photovoltaic power on site and batteries to store power.

Conclusion

DRDGOLD offers investors significant torque on the gold price. The company has an established dividend payment history and is currently yielding around 2.5%, which makes it an option for income oriented investors as well. While electricity supply has been unreliable and has hurt processing volumes, DRD is trying to reduce its dependence on Eskom through building its own photovoltaic power plant.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in DRD over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.