QABA: Volatility Is Significant But Outperformance Should Not Be Ignored

Summary

- QABA invests in community banks across the United States.

- This ETF appears to outperform during periods of enhanced market sentiment and fear. That said, this is no ordinary time period.

- QABA is a Sell for now, but I plan to follow this small, undercovered ETF closely for a potentially strong upgrade once the dust settles on the current crisis.

Tippapatt/iStock via Getty Images

The First Trust Nasdaq ABA Community Bank ETF (NASDAQ:QABA) may offer quality exposure to community banks with potentially smaller declines in the face of economic downturn. However, the state of the financial sector is currently front-page news, and that is rarely a good entry point for investors. That doesn't mean the storm won't blow over soon. However, I still need more evidence that prices are turning around from the historic selloff we've seen in recent weeks. Only then will I be able to assess the reward/risk tradeoff as being anything better than weak. Therefore, I give this ETF a Sell rating. That said, it won't take much sustained upward price movement for me to rekindle my interest in this high-potential long-term growth industry.

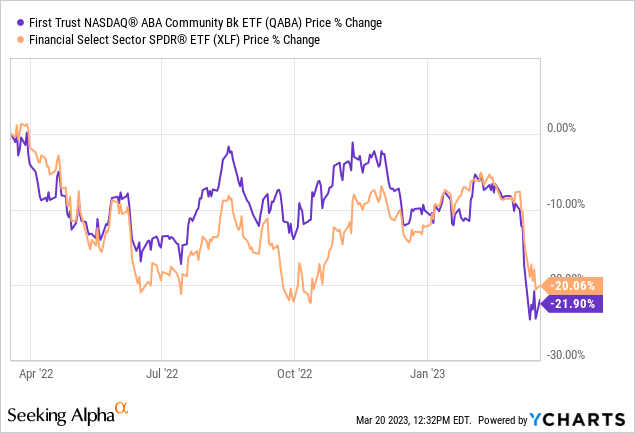

QABA is not a procyclical ETF like the Financial Select Sector SPDR ETF (XLF), whose holdings are more centered on larger investment banks. For this reason, QABA experienced smaller declines during the 2022 bear market compared to XLF. However, QABA also dipped back below XLF at the beginning of 2023. This shows that this ETF is overall not as sensitive to market sentiment and speculation of corporate reinstatement as alternatives like XLF. For the same reason, QABA may not see proportional increases in the event of economic recovery. This could be in or against one's favor, depending on one's tolerance to headwinds created by market downturn.

Strategy

QABA tracks the NASDAQ OMX ABA Community Bank TR USD Index and uses a full replication technique. This could work to minimize the tracking error and increase transparency, providing investors with accurate, genuine exposure to the designated industry. This ETF invests in growth and value stocks exclusively within the United States public equity markets.

Holdings Analysis

QABA invests purely in financial stocks within the United States. These financial stocks are primarily focused on smaller community banks. Therefore, this ETF may provide more narrow geographical exposure as these banks' influence is mostly limited to smaller towns and communities.

The top 10 holdings in this ETF account for 25% of total holdings and the top 25 comprise 47% in a fund of 152 securities, making QABA somewhat top-heavy. However, despite being top heavy, allocations are quite dispersed, with not one single stock comprising more than 4% of the total fund. After financial securities' recently displayed susceptibility to market speculation and fear, lesser concentration risk may give this ETF an edge.

Strengths

QABA could potentially profit from elevated interest rates, as rate hikes could increase deposit rates and the demand for loans. Both of these situations could enhance interest income within the community banks held in this ETF.

Community Banks also tend to hold fewer risky assets compared to larger banks, making them potentially less volatile. Risky assets include but are not limited to cryptocurrencies, emerging market bonds, and high-yield (junk) bonds. This could possibly explain QABA's outperformance during last year's bear market, where risky assets performed quite poorly.

Weaknesses

QABA is not positioned to profit from potentially reinstated mergers and acquisitions (M&A) activity in 2023 in the same way as ETFs with greater exposure to capital markets. ETFs like the iShares U.S. Regional Banks ETF (IAT) have similar caveats.

This ETF also has greater costs than the broader market and other financial ETFs, with an expense ratio of 0.60%. QABA also has an AUM of just over $100mm, which is lower than any ETF I have written about previously. Both of these factors make QABA an underfollowed, lower-liquidity ETF as compared to many I cover.

Opportunities

Community banks remain an important part of more regional economies and could increase in popularity as consumers shift toward local services. The magnitude of long-term growth in this ETF may ultimately hinge on timely economic recovery and community banks' ability to stay abreast of technological advancements in the banking industry.

QABA's price could increase in the event that investors continue buying cheap after the recent price decline. A sharp rebound could then enhance this ETF's earnings and potentially make it more attractive.

Community banks held in QABA could also benefit from trends in supporting local businesses rather than larger enterprises. Recent statistics suggest that since the onset of COVID-19 in early 2020, there has been a shift in consumer preferences toward smaller, local businesses. These trends could potentially continue in the medium to- long term. Community banks could therefore become a consumer preference, not to mention their propensity for building personal relationships with clients.

Threats

Despite its ability to partially hedge market downturn, this ETF is certainly not immune to macroeconomic headwinds generated by speculative catastrophes. It's evident in the graphs above that QABA experienced a price decline similar to XLF following bank runs in the last two weeks. This indicates that QABA is not just susceptible to downturns within its own holdings, but also any banks that might be affiliated. Therefore, this ETF remains somewhat volatile and the risks span beyond just its own holdings.

Community banks may also struggle to keep up with technological innovations in the banking industry. Recent innovations include online banking, artificial intelligence, and blockchain. Community banks often have fewer resources and staff with the technological expertise required to implicate increasingly complex technological features. Consequently, community banks are also often forced to rely on third parties for support. This may increase operational risk and generate compliance issues. Failure to keep pace with trends could lead investors away from QABA and instead towards funds with larger, more powerful institutions.

Though it's generally more difficult, community banks are still capable of implementing technological solutions. However, investors should be aware of their potential inferiority to more leading and developed banks in this regard. QABA may struggle to benefit from increased corporate activity in the long term compared to other financial ETFs. However, this ETF may also hedge some of the losses created by market downturn. This makes QABA potentially more defensive, which could be better for those that are more loss-averse or skeptical of the financial sector's growth forecast.

Conclusions

ETF Quality Opinion

I see QABA in a guilt-by-association situation with its broader sector. It is also a very underfollowed ETF. I'm the first Seeking Alpha contributor to write on it since mid-2018! But I think it's a great follow for me, and I am keeping it on my watchlist.

ETF Investment Opinion

QABA is a Sell for now, because there's too high a risk of further price erosion, versus the upside potential. However, I can see myself becoming much friendlier toward it, once we have more clarity on what the future of community banking will look like.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.