PGZ: With Regional Bank Weakness, CRE Is In Trouble (Rating Downgrade)

Summary

- The Principal Real Estate Income Fund is a closed end fund focused on fixed income.

- PGZ has a significant amount of mezz CMBS collateral.

- Regional banks are an important source of CRE loans, accounting for around 80% of the market.

- With many institutions now focused on survival and liquidity, we are going to see tighter lending standards and lower credit appetite.

- This translates into lower CRE valuations and lower profitability for equity tranches across the sector.

Daenin Arnee/iStock via Getty Images

Thesis

The Principal Real Estate Income Fund (NYSE:PGZ) is a closed end fund focused on fixed income. We covered this fund before here, where we were pointing out the CEF was approaching its Covid lows. We were arguing that once a bottoming-out forms, there is the potential for significant upside. That was all before the regional banks collapsed. In our humble opinion the dynamic has changed significantly in the Commercial Real Estate ('CRE') sector now, with significant weakness to come.

An informed reader needs to be aware of the massive maturity wall facing the CMBS market:

Debt Maturity Wall (SL Greene Preso)

As we can see from the above graph there are quite a few loans coming for renewal this year. What is the process when debt comes due?

- borrower goes back to the bank/sponsor to get another loan

- property is re-evaluated at market prices

- IF the lender agrees to take on the risk, a new loan is minted at a loan-to-value pegged on the new valuation and with a new market rate

- the most important aspects to note here are the valuation and the new market rate

Why do we think the regional banking crisis has changed the market dynamics significantly? Well:

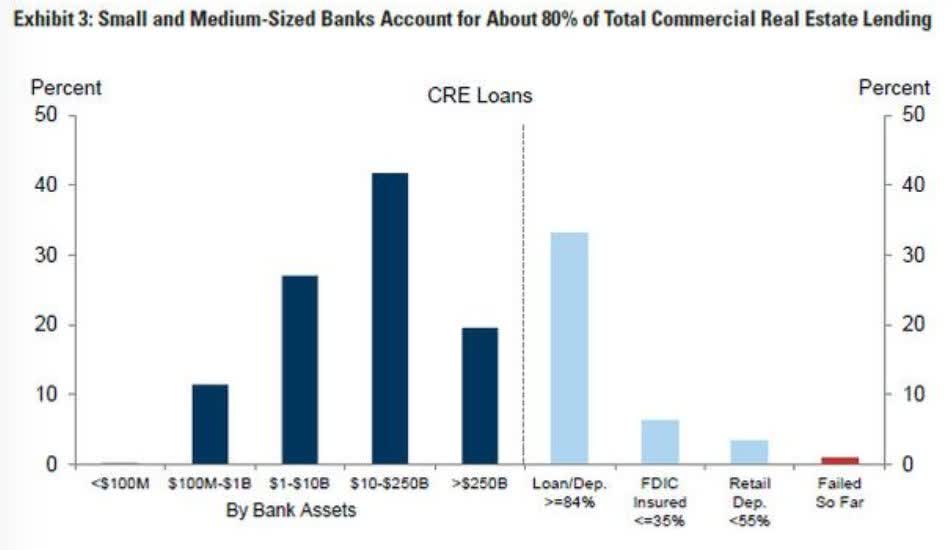

CRE Loans Originations (FactSet)

As per the above graph we can see the extreme preponderance for regional banks to make CRE loans. They account for 80% of the CRE lending! As an example, now failed Signature bank accounts for an astounding proportion of the NYC CRE market:

Trepp data estimated that a whopping $25.5 billion of the bank’s $35.2 billion commercial real estate loan portfolio was tied to New York City properties, and that Signature Bank covered 12 percent of bank lending in commercial real estate in New York. Signature had previously noted in its 2022 10-K that all of the real estate collateral for the loans in its portfolio is located within the New York metropolitan area.

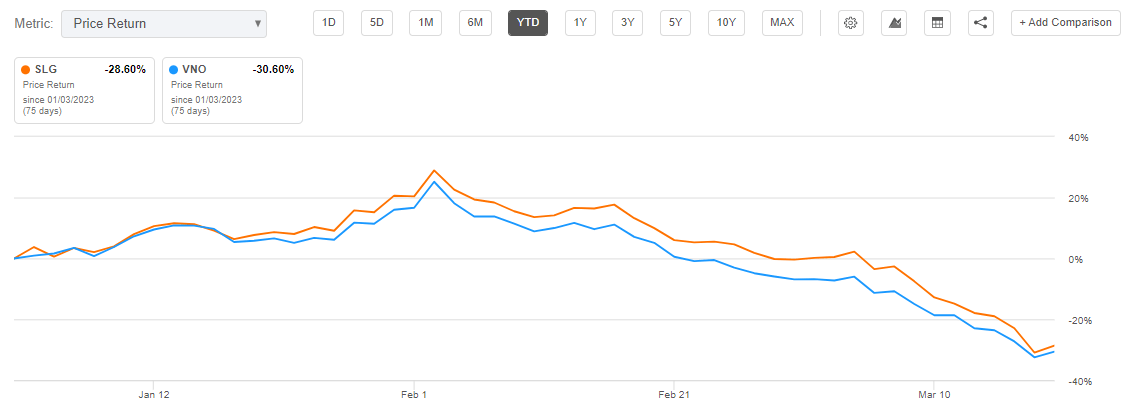

This simply means that when loans come due in the NY metro area there will be less competition/appetite to re-finance them, which translates into lower valuations and lower profitability for the equity sponsor. We can get a live view of this thesis through the performance of two premier NYC Office Reits:

Returns Office Reits (Seeking Alpha)

Both (SLG) and (VNO) are down around -30% year to date, embedding the lower profitability implied by the latest market developments.

Regional Banks as tenants

There is also a secondary, less discussed aspect brought about by the banking crisis. Many regional banks do not own their main office buildings, but have done sell and lease-back transactions:

Trepp’s report— compiled as regional bank’s stock prices went into freefall this week—also includes other regional banks that could present potential tenancy risk to CMBS loan collateral, such as Comerica Bank, Huntington Bancshares, Western Alliance Bancorporation and Signature Bank.

Utilizing the properties as both headquarters and branches, First Republic Bank, KeyBank and Charles Schwab Corporation are top tenants in Trepp’s list of CMBS office loans to watch, with those loans ranging from $170 million to $565 million in size.

To translate this into English - if a bank becomes insolvent, it is highly likely that it will not utilize its former prime, expensive office building, which in turn results in lower rents for the building.

We feel this is more of a secondary effect, and will not affect the market as much as the tightening conditions that will be created by regional banks not lending anymore.

PGZ Collateral

The CEF is overweight mezz CMBS securities:

Collateral (Fact Sheet)

We can see that over 63% of the collateral is represented by CMBS bonds. While many of them are seasoned (i.e. they have been outstanding for a long time), they represent mezzanine pieces in a debt structure.

When lending gets tough in the CRE space and valuations come down, the propensity for the structures to 'attach' (i.e. generate full losses for mezz tranches) is higher.

A retail investor needs to understand these pieces of debt are highly structured and an investor needs to run an asset by asset cash-flow model with specific considerations in order to better understand the structure and residuals (Trepp does this for example).

As we have seen from the Credit Suisse experience, at the moment the market does not really have a bid for illiquid, distressed assets. There will be a lot of pain in the sector before valuations re-set to more conservative levels.

Conclusion

In our prior article we were hoping for a bottoming process to start for PGZ, which would have created conditions for a Buy rating. Unfortunately the latest developments in the market are at the opposite side of the spectrum. With three regional bank defaults, and potentially more coming, the entire sector is under tremendous pressure. Rather than focusing on lending rates and profitability, regional banks are now concentrated on survival and liquidity. Small and medium sized banks account for over 80% of the total CRE lending, and we are going to see the impact of tighter standards and lower credit appetite. With a significant wave of CMBS re-financings this year, valuations and profitability are coming down. Many of the bonds in the PGZ collateral pool are mezz CMBS tranches which could suffer impairments if properties are valued at distressed levels. Instead of a bottom here, we feel there is more weakness to come. We are moving to Sell for PGZ now.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.