Luna Innovations: The Financials Looks Steady

Summary

- LUNA recently announced its FY22 and Q4 FY22 results.

- The technical chart of LUNA appears unsteady, indicating further decline.

- The Liso purchase worked out well for them. It aided them in expanding their business reach in Europe.

- I assign a hold rating on LUNA.

deepblue4you

Luna Innovations Incorporated (NASDAQ:LUNA) develops and manufactures fiber optic test and control products worldwide. They provide optical test and measurement products, which include optical backscatter reflectometers. They also offer polarization control products, including instruments to manage and control polarization; tunable lasers; ODiSI sensing solution; and products of TeraMetrix terahertz that offer precise single and multi-layer thickness and caliper thickness measurements. They recently posted their FY22 and Q4 FY22 results. In this report, I will analyze its financial performance and give my views on its growth potential. The technical chart of LUNA looks weak, and the valuation seems high for now. As a result, I give LUNA stock a hold rating.

Financial Analysis

LUNA recently posted its FY22 and Q4 FY22 results. The revenue for FY22 was $109.4 million, a rise of 25.1% compared to FY21. I think the primary cause of the increase was their acquisition of Lios, which led to a rise in the utilization of their terahertz technology as well as their strength and communications test products. The gross profit margin for FY22 was 60.7% which was 59% in FY21. I believe the revenue mix led to a rise in gross profit margin. The net income for FY22 was $9.2 million, a rise of 571.4% compared to FY21.

The revenue for Q4 FY22 was $31.7 million, a rise of 30.8% compared to Q4 FY21. Strong growth in the company's terahertz products and legacy businesses, in my opinion, was the primary driver of the rise. The gross profit margin for Q4 FY22 was 61% which was 58% in Q4 FY21. I believe since product sales made up a larger percentage of its total sales this quarter than they did in Q4 2021, the increase in gross profit margin was mainly the result of the mix. The net income for Q4 FY22 was $853 thousand, a decline of 45.8% compared to Q4 FY21. In my opinion, the primary causes of the net income decline were increased expenses and higher spending on R&D. I thought LUNA's financial performance in FY22 was quite impressive; both revenue and net income considerably increased. They benefited from the Lios purchase, and in FY22, demand for their terahertz products rose considerably.

Technical Analysis

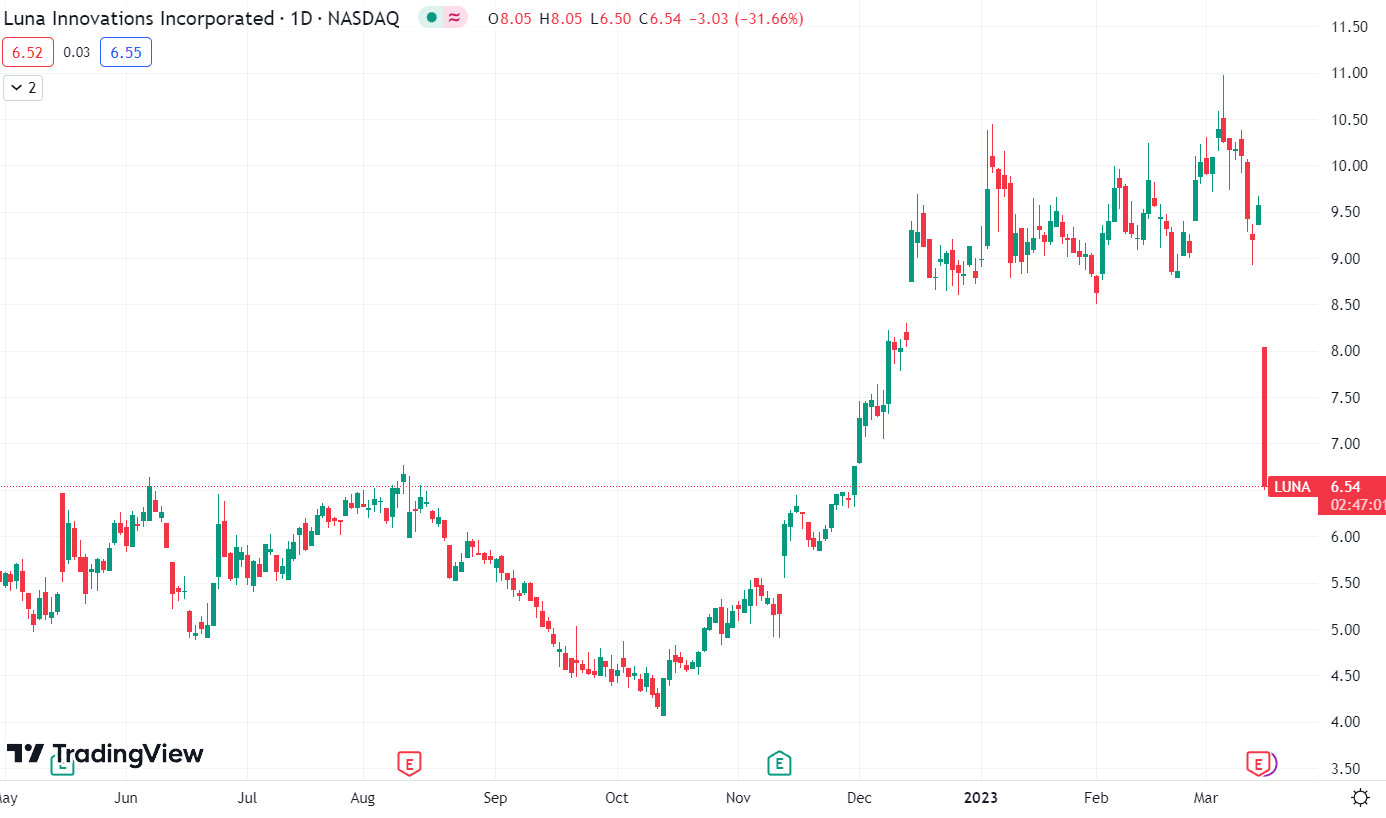

Trading View

LUNA is trading at the level of $6.5. Since December 2022, the stock had been ranging between $8.6 and $10, but it recently experienced a significant breakdown. Currently, at $6.5, it can move up by 25% from current levels if it demonstrates the strength and forms a green candle close to the support zone. The next support zone is at $5, so if it can't hold the level, it could fall as low as $5. In light of the stock's current bearish outlook, in my view, it is best to stay away from it. Only when the stock creates a green candle in the daily time frame near $6.5 should one consider opening long positions.

Should One Invest In LUNA?

Seeking Alpha

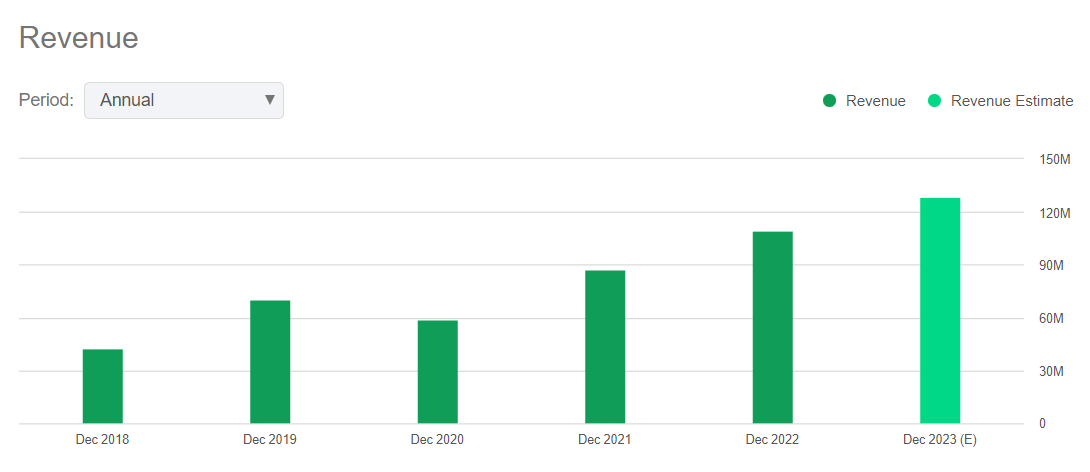

The revenue estimate for FY23 is around $128.3 million, which is 17.2% higher than FY22 revenue. Since FY21, their revenues have increased considerably as a result of strong performance. I think they will meet their revenue goals because the management is committed to expanding the business and is doing so in a number of ways. By selling Luna Labs last year and acquiring Lios Sensing, they have shifted their attention to fiber optics and sensing systems, which has been profitable for them. Because Lios is located in Germany, it assisted them in expanding their presence in the European market. Their growth trajectory appears to be steady, and the management is making efforts to accelerate growth.

Talking about the valuation. I will use two valuation metrics to judge its valuation. The first ratio is the P/E ratio, calculated by dividing share price by EPS. They have a P/E (FWD) ratio of 23.8x compared to the sector ratio of 19.47x. It shows that they are overvalued. The second ratio is the Price / Sales ratio, calculated by dividing a firm's market capitalization by its sales over the past 12 months. They have a Price / Sales (FWD) ratio of 1.9x; generally, a ratio above one suggests that the company is overvalued. So after looking at both ratios, I believe they are currently overvalued.

Risk

Their capacity to switch to a revenue mix that includes revenues from the provision of services or from licensing, especially after its sale of Luna Labs in March 2022, will determine their business strategy and future growth. Product sales and these earnings might be more scalable than those from contract research. In order to reflect a larger portion of its total revenues, they intend to expand its sales of commercial products, its licensing income, and its provision of non-research services to clients. However, suppose they are unable to increase their product sales, service revenue, or contract research income through licensing. In that case, they cannot implement their business plan or expand their market share.

Bottom Line

Their revenue and net income grew significantly in FY22. The Liso acquisition and sale of Luna labs proved to be beneficial for them. They are expanding its business internationally, and the acquisition of Liso has helped them broaden its steps into the European markets. The only problem is that the technical chart of LUNA looks weak, and the valuation metrics suggest that they are currently overvalued. Hence after analyzing all the aspects, I assign a hold rating on LUNA.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.