PacWest Bancorp: Fear Is Off The Charts, Time To Buy

Summary

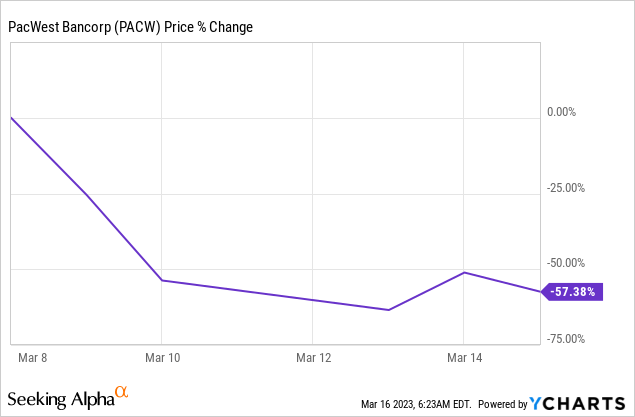

- PacWest Bancorp has lost 57% of its value in the last week.

- However, the fear barometer is off the charts, potentially indicating a situation in which high-risk investors could earn significant alpha.

- The Fed's deposit backstop is an effective way, in my opinion, to prevent deposit flights from small and mid-sized community banks.

- PACW stock trades at a massive 60% discount to BV.

JHVEPhoto

Shares of community bank PacWest Bancorp (NASDAQ:PACW) went through a major revaluation to the downside in the aftermath of the Silicon Valley Bank collapse last week. As I indicated in my work on First Republic Bank (FRC) -- Buy the Bloodbath -- there is currently a huge opportunity in the community banking sector to capitalize on the fear stoked by the shutdown of Silicon Valley Bank in California and Signature Bank in New York. The Fed has provided a liquidity facility to the banking sector over the weekend which I believe is an effective measure to reduce the risk of deposit flight. As one of the most heavily punished community banks, I believe PacWest Bancorp is set for a major upward correction once fear is no longer ruling the market!

Fear is off the charts

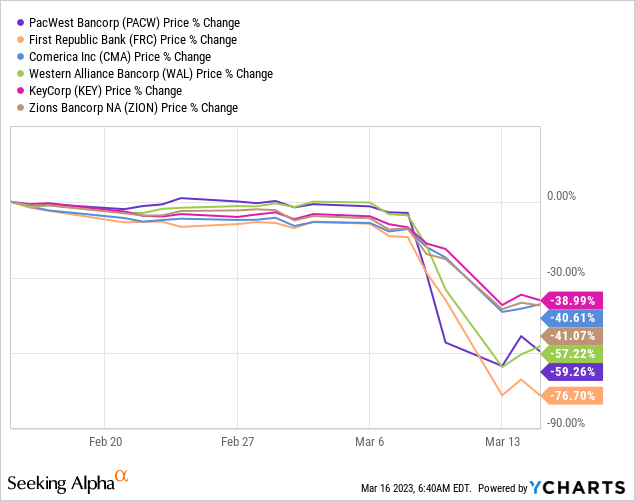

PacWest Bancorp has lost more than half of its value last week, making it the second-biggest valuation loss in the industry group. Only First Republic Bank lost a bigger chunk of its valuation.

The key catalyst for the value destruction in the community banking market has been the collapse of three banks recently: crypto-focused Silvergate Bank, venture-focused Silicon Valley Bank and Signature Bank. The last two of those represented the second and third-largest bank failures in U.S. history. The reason behind Silicon Valley Bank failure was that the bank invested heavily while its deposit base was shrinking, in mortgage-backed securities which lost value as the Fed raised rates. SVB realized a $1.8B loss which resulted in a major confidence crisis in the banking sector that quickly spread to the community banking market. The resulting market sell-off chiefly affected smaller and mid-sized community banks that are not considered systemically important and that also, like Silicon Valley Bank, have a focus on providing capital to venture-backed businesses, like PacWest Bancorp.

As a result, large banks like Bank of America are seeing major deposit inflows while community banks have seen outflows. The Fed was forced to step in over the weekend and did so quite effectively, in my opinion: the Fed allowed small banks to pledge high-quality assets like U.S. Treasuries, agency debt and mortgage-backed securities as collateral in exchange for short term cash, thereby greatly reducing the probability of a deposit run.

PacWest Bancorp is a well-managed community bank with a venture focus

In a liquidity and deposit update from March 9, 2023, PacWest Bancorp said that it had deposits of $33.2B as of 3/9/23 compared to $33.9B as of 12/31/2022, showing a decline of only 2%.

Deposit outflows likely increased in the wake of SVB's shutdown, but the Fed created the Bank Term Funding Program over the weekend which allows financial institutions to access a liquidity pool to fund withdrawals. PacWest Bancorp likely saw additional deposit outflows on Friday and Monday, but I believe the situation, given the availability of the Fed's liquidity facility, may not be as bad as feared.

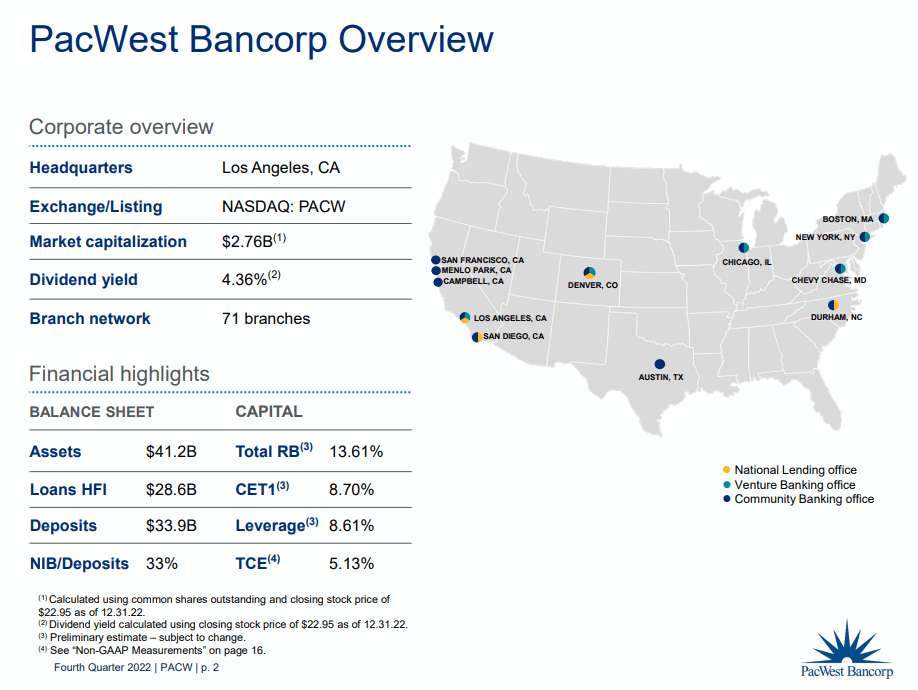

PacWest Bancorp was excessively punished in the last four days for its exposure to venture-backed companies as well as its limited operating footprint in a number of coastal markets. PacWest Bancorp is a smaller community bank with $41.2B in assets as of December 31, 2022 and just 71 branches.

Source: PacWest Bancorp

PacWest Bancorp was also punished because of its venture-focus. The bank had $11B in deposits from start-ups, which were also a core focus of Silicon Valley Bank. Venture deposits have steadily declined in FY 2022, however, due to higher yields available on U.S. Treasuries.

Source: PacWest Bancorp

Steep valuation discount, potential alpha opportunity

First Republic Bank and PacWest Bancorp were the two most heavily punished mid-sized banks last week which, in my opinion, suggests that investors may be too much driven by fear after the failure of Silicon Valley Bank.

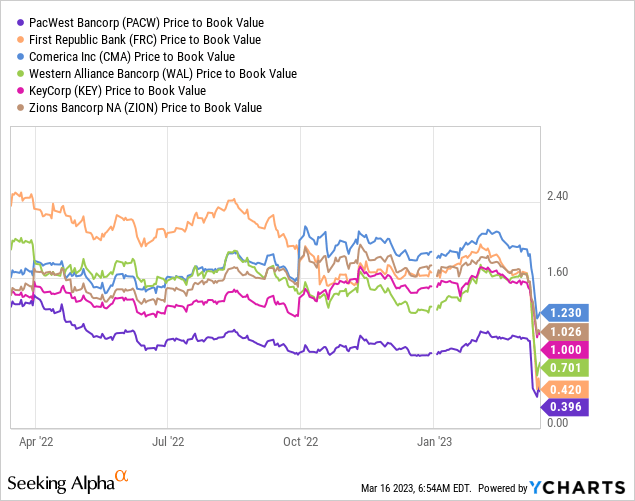

PacWest Bancorp's book value as of December 31, 2022 was $28.71 per-share, showing an increase of 2.3% compared to the September-quarter. Shares of PacWest Bancorp are currently valued at a 60% discount to book value... which is the largest in the valuation chart below.

Risks with PacWest Bancorp

The biggest risk for PacWest Bancorp is that depositors will move their deposits over to systemically important banks such as Bank of America or JPMorgan Chase just because of fear. Non-SIB banks may have no issue funding deposit withdrawals due to Fed-provided liquidity, but their deposit bases and asset values may decline steeply in the short term. However, I believe the Fed's deposit backstop will prove to be an effective way to safeguard the community banking system as every financial institution can now get emergency access to cash, if the need arises.

Final thoughts

Fear is a powerful motivator and often it signals that investors are too bearish. PacWest Bancorp is a high-risk, but also high-potential bet on the recovery of the community banking market and the broader U.S. financial system. PacWest Bancorp was a growing and well-run community bank just last week ago, with a solid deposit base and a book value close to $29. Through no fault of its own, PacWest Bancorp's shares are now trading at $11.37, implying a 60% discount to book value. I believe PACW and FRC have strong rebound potential once investors start to rationally evaluate community bank stocks again and are no longer fearful.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of PACW, FRC either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.