In all our work, we tend to deal in probabilities and possibilities. None of us are blessed with divine knowledge and hence certainties are outside our grasp. We estimate based on the data available. True North however did give a nod to our analysis and did a drastic cut.

The REIT also announced its capital strengthening and unitholder ("Unitholder") value strategy which includes: 1) the sale of two recently vacated Ontario properties to separate purchasers; and 2) effective with the March 2023 distribution payable on April 17, 2023, to Unitholders of record on March 31, 2023, a 50% distribution reduction. These strategic initiatives are expected to provide the REIT with greater financial strength and the flexibility to address future tenant turnover while preserving capital, improving its leverage profile and delivering long-term value to its Unitholders.

"The implementation of the strategic initiatives announced today will allow the REIT to strengthen its financial and liquidity position, while delivering long-term value to its Unitholders. The reduction of the REIT's distribution will provide an additional $25 million of cash annually that will be used primarily to improve its capital profile and deliver Unitholder value," explained Daniel Drimmer, the REIT's Chief Executive Officer. "The disposition of the recently vacated buildings located at 360 Laurier Avenue West and 400 Carlingview Drive provides us with the ability to extract their underlying value at this time and will provide approximately $5 million of excess sale proceeds to further strengthen the REIT's financial position. Disposing of non-core assets and reducing leverage while also focusing on opportunities to deliver Unitholder value, are expected to be our driving focus as we move forward in 2023."

What drove this cut? Is this level sustainable? What is the fair value for the REIT today? These are questions that we will delve into in our analysis.

What Created The Distribution Cut?

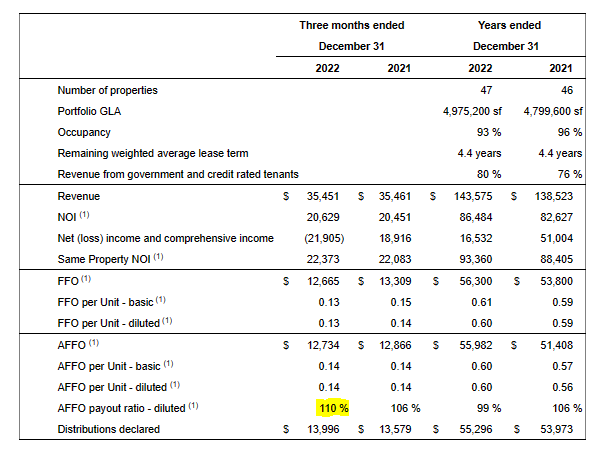

True North had a very poor distribution coverage and we saw that again in Q4-2022. The adjusted funds from operations (AFFO) payout ratio moved up to 110%.

True North Press Release

The fourth quarter is generally a weaker quarter for coverage as expenses tend to move a bit higher. Nonetheless, that lack of coverage at the AFFO level, which we have brought up before, shows how tough it was for True North to sustain the distribution. That was still only the first hurdle. One only needs to read the financial statements once to see what problems the company was facing beyond baseline coverage.

Q4-2022 FFO basic and diluted per Unit were lower by $0.02 and $0.01, respectively compared to Q4-2021. Q4-2022 AFFO basic and diluted per Unit remained stable at $0.14. YTD-2022 FFO basic and diluted per Unit increased $0.02 and $0.01, respectively, to $0.61 and $0.60. YTD-2022 AFFO basic and diluted per Unit increased $0.03 and $0.04, respectively to $0.60.

Excluding termination fees, Q4-2022 FFO and AFFO basic and diluted per Unit would have been $0.12 and YTD-2022 FFO and AFFO basic and diluted per Unit would have been $0.52. Q4-2022 AFFO diluted payout ratio would have been 127% and YTD-2022 AFFO diluted payout ratio would have been 115%.

Source: True North Press Release (emphasis ours)

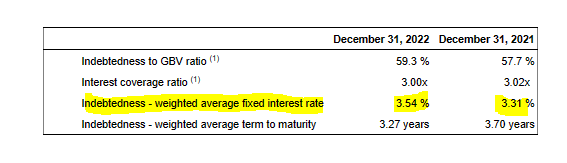

Finally, as we move into 2023, things were about to get a lot harder for the REIT from an interest rate perspective.

True North Press Release

The interest rate has been creeping up as the refinancing process continues. The latest quarter numbers were at 5.38%.

During the quarter, the REIT refinanced a total of $36,000 (YTD-2022 - $118,820) of mortgages with a weighted average fixed interest rate of 5.38% (YTD-2022 - 4.53%) for five year terms (YTD-2022 - one to seven year terms), providing the REIT with additional liquidity of approximately $8,800 (YTD-2022 - $29,400).

Source: True North Press Release

There will be a palpable drop in AFFO just from interest rate moves.

Is This Level Sustainable?

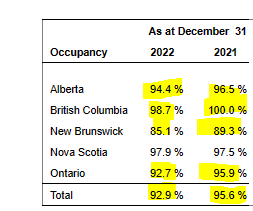

50% cut is of course rather deep and the first assumption would be that we are now comfortably in the clear. For 2023, itself, we think the REIT is definitely in a good place. But beyond that, one would not be too sure. The occupancy drops year over year took place in 4 out of the 5 provinces.

True North Q4 Financial Report

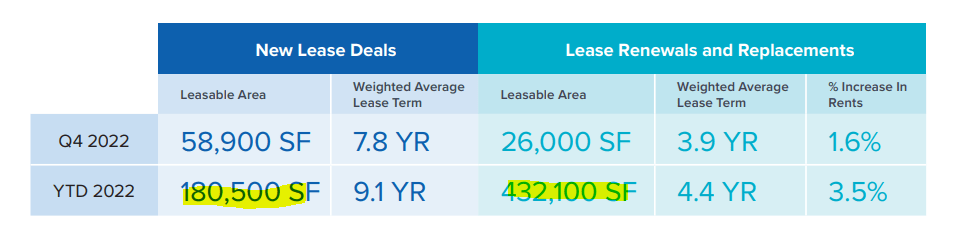

The 92.9% number is a good drop from the last quarter (94.6%). Based on its square footage and average lease term, True North needs to be renewing close to 1.0 million square feet of leases a year to keep occupancy and lease length static. We got only 612,600 square feet in 2022.

True North Q4 Financial Report

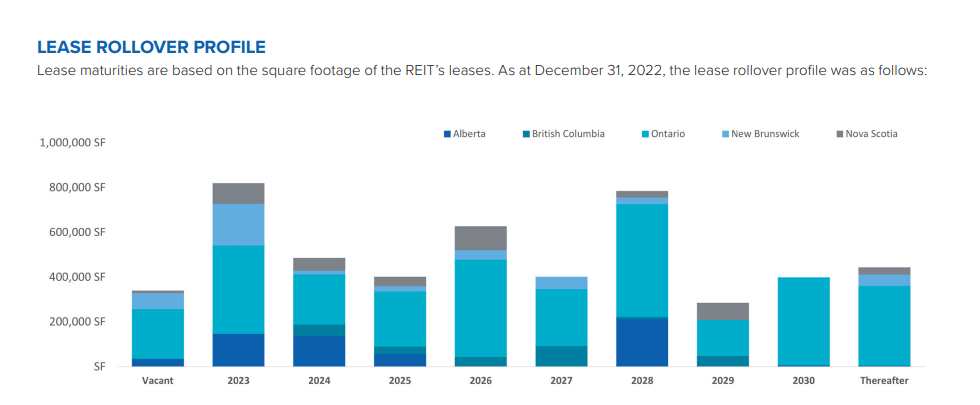

Upcoming lease maturities will be extremely challenging in 2023.

True North Q4 Financial Report

These are numbers as of December 31, 2022. Note that the two sales were done on properties where the building was almost completely empty as of the release of this report.

The Carlingview Property, a single-tenanted office building located in close proximity to Toronto Pearson International Airport, was purchased in February 2013 and became fully vacant as of March 2023. The Laurier Property is an eleven-story office building located in Ottawa and was purchased in February 2019. The Laurier Property is approximately 96% vacant as of February 2023 with the sale expected to close on or about June 15, 2023.

So AFFO pressure will remain strong throughout the year.

What Is The REIT Worth?

If you use the REIT's last metrics, the NAV is close to $6.00 a share. Of course, that was computed using the capitalization rates shown below.

True North Q4 Financial Report

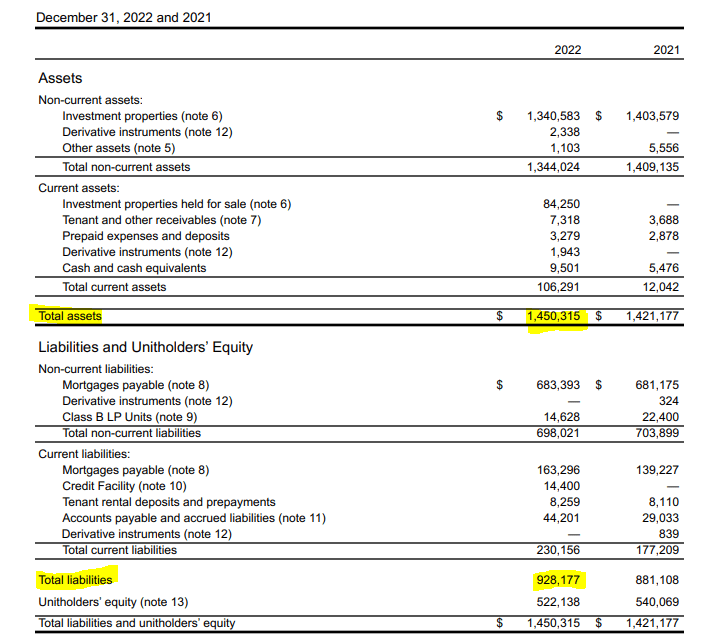

We have said this before and we will say this again. We don't think those numbers are realistic. True North is not the only one using cap rates we don't think will hold today. We saw the same thing with Dream Office REIT (D.UN:CA) and Brookfield Property Partners. True North's debt to asset ratio is also very high.

True North Q4 Financial Report

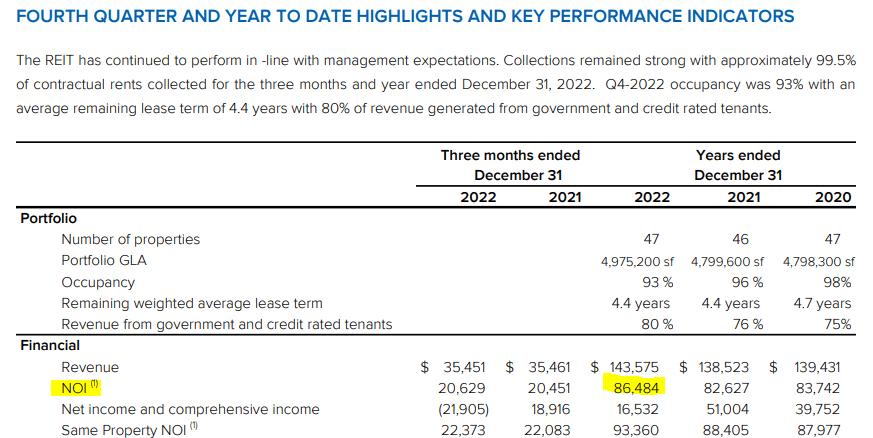

So small movements in the cap rate will cause a big distortion in the NAV. Let us show you. The NOI was close to $86.5 million.

True North Q4 Financial Report

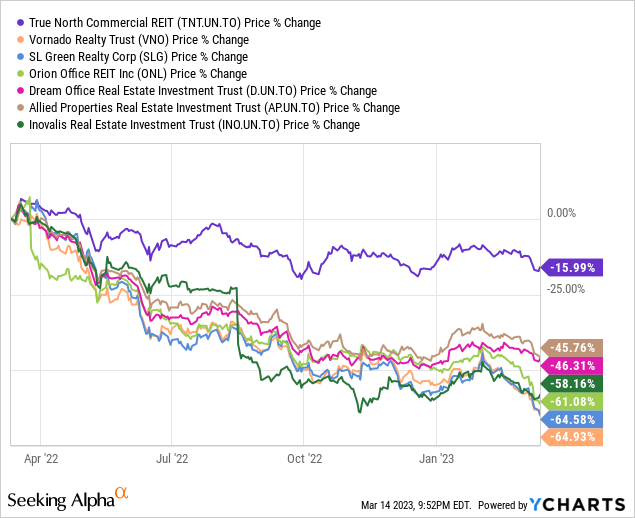

If you apply an 8% cap rate, the NAV drops to $3.25 per share. We think this is more realistic for office properties especially with such short leases in troubled markets like Alberta. Yes, the tenants are investment grade. That only means they have better negotiating power and can find a better place if they need to. We think that the stock will actually trade to that $3.25 level very soon. In case you think this would be an anomaly, have a look at some other office REITs in US and Canada. True North has held up partially because of its huge dividend.

Now that has been cut, what do you think happens next?

Verdict

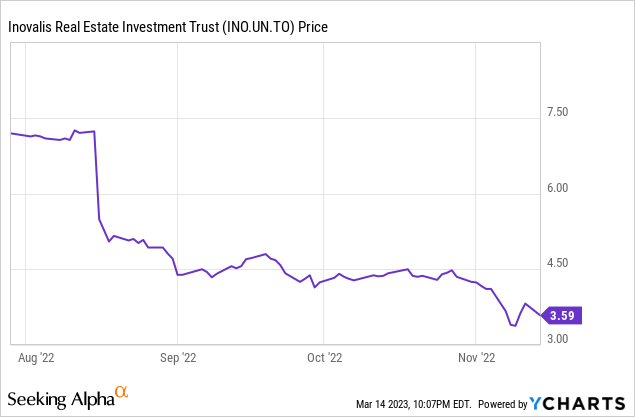

When the first round of selling is over, here is what will happen. You will feel regret if you already owned it. But you will think True North has certainly become cheap. Price anchoring will tell you that if the only thing that has changed is the distribution, surely you should be ready to back up the truck at $4.50? What you will miss here is that the distribution should have been cut way back to align to fundamentals. What you will miss is that this is the first salvo in the battle. Keep in mind that big distribution cuts never create a bottom on day 1. Here is Inovalis REIT (INO.UN:CA), which "surprised" investors with a distribution cut. About as surprised as one can get for a REIT running a 200% AFFO payout ratio. The stock still bottomed 3 months later.

We may be biased here (well we have a small short position), but we think that 8% cap rate NAV will be visited in 2023. If you disagree, tell us why.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Are you looking for Real Yields which reduce portfolio volatility?

Conservative Income Portfolio targets the best value stocks with the highest margins of safety. The volatility of these investments is further lowered using the best priced options. Our Cash Secured Put and Covered Call Portfolios are designed to reduce volatility while generating 7-9% yields. We focus on being the house and take the opposite side of the gambler.

High Valuations have distorted the investing landscape and investors are poised for exceptionally low forward returns. Using cash secured puts and covered calls to harvest income off value income stocks is the best way forward. We "lock-in" high yields when volatility is high and capture multiple years of dividends in advance to reach the goal of producing 7-9% yields with the lowest volatility.

Preferred Stock Trader is Comanager of Conservative Income Portfolio and shares research and resources with author. He manages our fixed income side looking for opportunistic investments with 12% plus potential returns.

Disclosure:I/we have a beneficial short position in the shares of TNT.UN:CA either through stock ownership, options, or other derivatives.I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Recommended For You

Comments (3)

To ensure this doesn’t happen in the future, please enable Javascript and cookies in your browser.