Gentex Corporation: Attractive Performance Justifies Further Upside From Here

Summary

- Gentex Corporation continues to grow nicely, with sales climbing even as 2022 proved to be a rocky year for profits and cash flows.

- At the end of the year, the company demonstrated some nice bottom line improvement, and the forecast for 2023 is encouraging.

- Shares are just cheap enough to warrant some additional upside from here.

- Looking for a helping hand in the market? Members of Crude Value Insights get exclusive ideas and guidance to navigate any climate. Learn More »

Sundry Photography/iStock via Getty Images

At this point in time, pretty much anything related to the automotive space is being looked at in a questionable manner. High inflation, combined with the rising interest rates aimed at combating it, can be perceived as a double whammy of an attack on the automotive space. Add on top of this the prospect that current economic conditions could eventually lead to a recession that would result in lower vehicle demand, and it would come as no surprise why people might stay away from this space. But one player that has done incredibly well in recent months is Gentex Corporation (NASDAQ:GNTX), a producer of digital vision, connected car, and dimmable glass products. It also sells fire protection products as well. Despite broader economic concerns, management has done well to push revenue, profits, and cash flows higher. Shares have responded in kind, with performance exceeding what the broader market has experienced. Truth be told, the stock of the company is not quite as cheap as it was when I last spoke favorably about it, but it is still at a low enough price and the health of the business is still robust enough, as to warrant a soft ‘buy’ rating at this time.

Attractive results across the board

In the middle of October of last year, I decided to revisit my prior bullish thesis on Gentex. In that article, I talked about how the company was continuing to post consistent revenue growth. Unfortunately, however, the profit and cash flow picture had been somewhat mixed. Despite that pain, I felt as though shares of the business were trading at cheap enough levels to warrant a ‘buy’ rating. Since then, the company has performed along the lines of what I would have anticipated. While the S&P 500 is up 6.1%, shares of Gentex have seen upside of 11.8%.

Author - SEC EDGAR Data

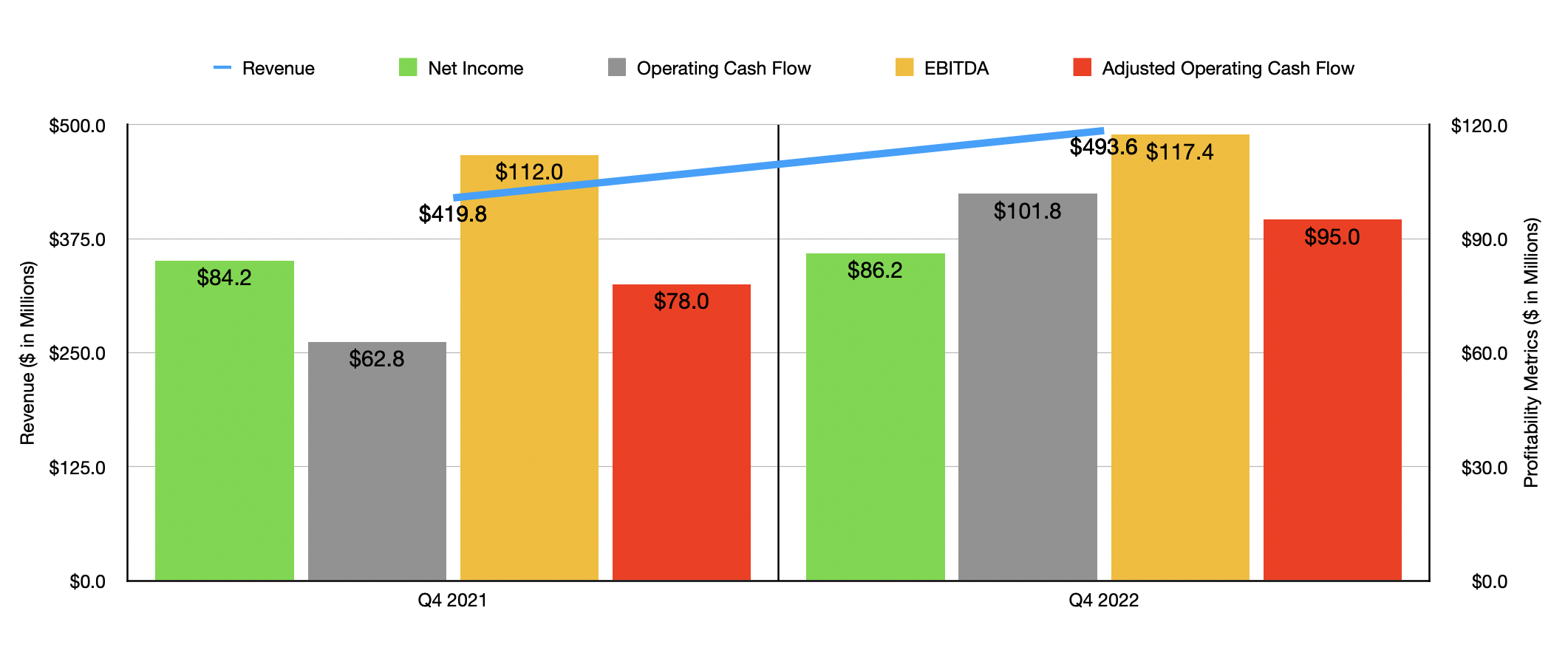

To understand why share price performance has been so much greater than what the S&P 500 has enjoyed, we need only look at data covering the final quarter of the company's 2022 fiscal year. During that time, revenue came in at $493.6 million. That's 17.6% higher than the $419.8 million reported one year earlier. This rise in revenue did include $15 million of cost recoveries from its customers. So without that, growth would have been a bit weaker. Having said that, the company benefited from a 7% quarter-over-quarter rise in light vehicle production spread across North America, Europe, Japan, and Korea.

On the bottom line, the picture also improved. Net income grew from $84.2 million in the final quarter of 2021 to $86.2 million in the final quarter of 2022. Even though sales increased nicely, it's worth mentioning that this translates to a margin decline for the company. In fact, its gross profit margin shrank from 34.3% down to 31.2%. This was driven largely by raw material cost increases, an unfavorable product mix, higher manufacturing costs that came from labor cost increases, and other factors. Even so, other profitability metrics continue to rise because of the growth in sales. Operating cash flow, for instance, shot up from $62.8 million to $101.8 million. If we adjust for changes in working capital, it would have risen more modestly, but still at an impressive rate, from $78 million to $95 million. And finally, EBITDA for the company grew from $112 million to $117.4 million. Even though margins contracted, management felt comfortable enough to buy back some additional stock. During the final quarter of the year, the firm repurchased 0.8 million shares for roughly $21.7 million. That brings total purchases for the 2022 fiscal year up to 4.04 million for a combined $113.9 million.

Author - SEC EDGAR Data

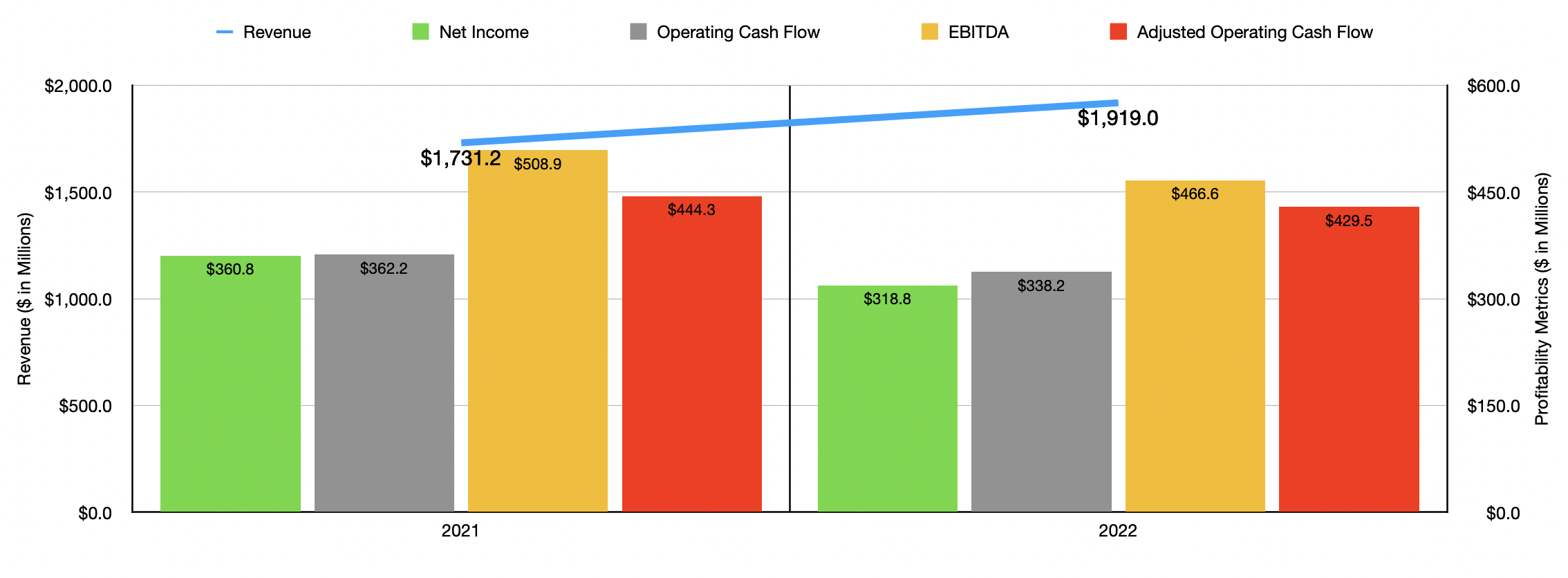

The revenue growth achieved in the final quarter was not a one-time thing. In fact, revenue was strong for the 2022 fiscal year as a whole. Sales of $1.92 billion beat out the $1.73 billion reported for 2021. This increase, totaling 10.8%, was thanks in large part to a 6% year-over-year increase in automatic dimming mirror shipments. These grew from 41.8 million units in 2021 to 44.2 million units last year. Despite the surge in revenue, profits for the company pulled back. High costs, particularly on the gross margin side of things, pushed net income down from $360.8 million to $318.8 million. Other profitability metrics followed a similar trajectory. Operating cash flow declined from $362.2 million to $338.2 million, while the adjusted figure for this declined from $444.3 million to $429.5 million. Meanwhile, EBITDA for the business dropped from $508.9 million to $466.6 million.

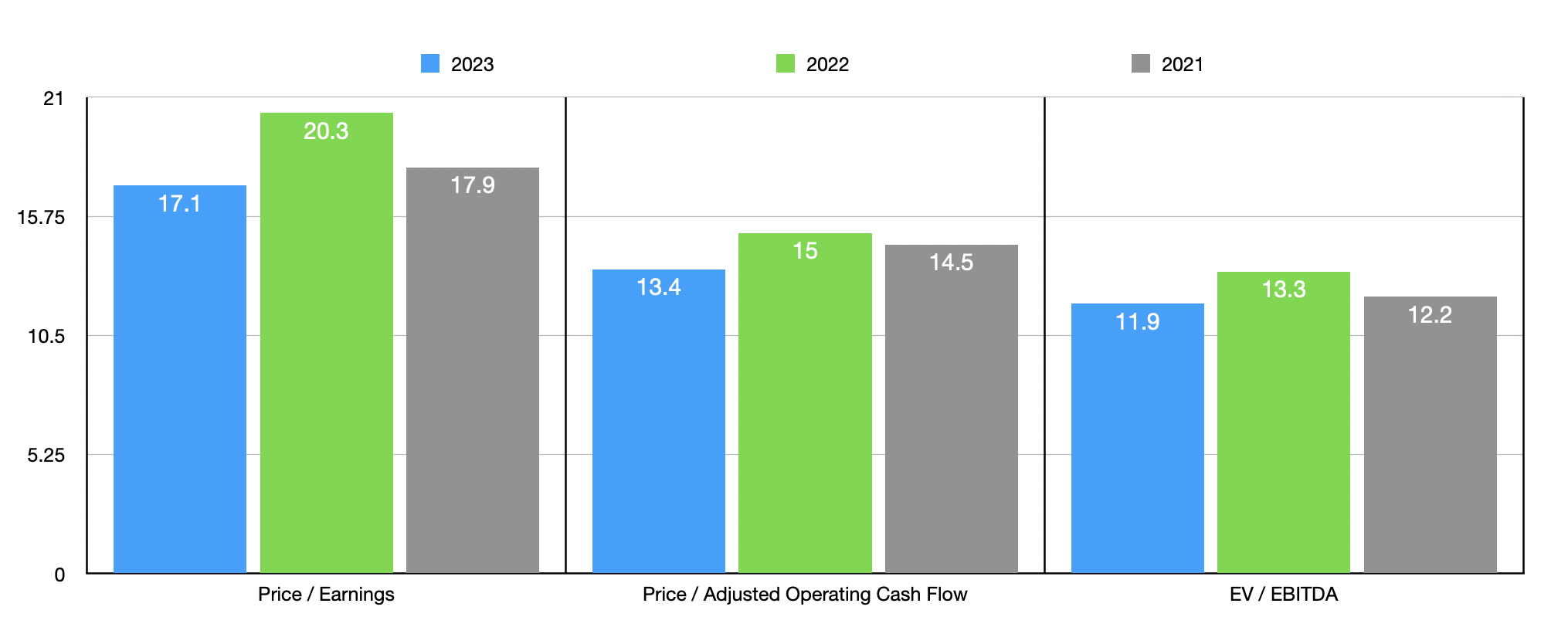

When it comes to the 2023 fiscal year, management has provided some guidance. Revenue, for instance, is forecasted to come in at around $2.2 billion, with a rise in shipments aiding the company. This rise, management said, should be driven by a roughly 3.7% increase in light vehicle production. Management did not exactly give a specific number on profitability. But they did give guidance on specific cost items that lets us get a good approximation. Based on my estimates, the company should generate around $378 million in net income in 2023. Playing with the numbers they provided, I also calculated operating cash flow of about $483 million. If EBITDA grows at the same year-over-year rate their operating cash flow is forecasted to, we would expect a reading for it of $524.7 million.

Author - SEC EDGAR Data

Using these estimates, I calculated that the company is trading at a forward price-to-earnings multiple of 17.1. The forward price to adjusted operating cash flow multiple should be 13.4, while the EV to EBITDA multiple should come in at 11.9. As you can see in the chart above, this pricing is lower than what we would get using data from 2022. It's closer, however, to what we would get using data from 2021. As part of my analysis, I also compared the company to five similar businesses. On a price-to-earnings basis, these companies ranged from a low of 14.9 to a high of 24.5. Using the price to operating cash flow approach, the range was between 7.9 and 25.8. In both of these cases, three of the five firms were cheaper than our target. Meanwhile, using the EV to EBITDA approach, we get a range of between 7.7 and 17.3. Four of the five companies ended up being cheaper than Gentex in this case.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Gentex Corporation | 20.3 | 15.0 | 13.3 |

| Autoliv (ALV) | 18.7 | 11.1 | 9.0 |

| Lear Corp. (LEA) | 24.5 | 7.9 | 8.3 |

| Fox Factory Holding Corp. (FOXF) | 23.6 | 25.8 | 17.3 |

| Standard Motor Products (SMP) | 14.9 | 11.6 | 7.7 |

| Modine Manufacturing (MOD) | 17.5 | 17.3 | 9.3 |

Takeaway

Right now, I wouldn't exactly call the fundamental condition of Gentex ideal. Sales continue to rise nicely, but the company had a rough 2022 fiscal year. The good news is that current guidance suggests continued revenue growth, as well as a meaningful uptick in profitability. Management continues to buy back stock, plus the company has no debt on its books and enjoys $237.8 million in cash and cash equivalents on hand. This cash figure, it's worth mentioning, excludes $153.9 million in long-term investments, as well as another $48.4 million in equity method investments. This provides the business a great deal of wiggle room should of the time come that it needs it. Shares are not exactly the cheapest on the market, either on an absolute basis or relative to similar firms. But when looking at the overall health of the firm, it is just cheap enough in my view to warrant additional upside from here.

Crude Value Insights offers you an investing service and community focused on oil and natural gas. We focus on cash flow and the companies that generate it, leading to value and growth prospects with real potential.

Subscribers get to use a 50+ stock model account, in-depth cash flow analyses of E&P firms, and live chat discussion of the sector.

Sign up today for your two-week free trial and get a new lease on oil & gas!

This article was written by

Daniel is an avid and active professional investor. He runs Crude Value Insights, a value-oriented newsletter aimed at analyzing the cash flows and assessing the value of companies in the oil and gas space. His primary focus is on finding businesses that are trading at a significant discount to their intrinsic value by employing a combination of Benjamin Graham's investment philosophy and a contrarian approach to the market and the securities therein.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.