Pioneer Natural Resources Vs. Devon Energy: Which Is The Best Of The Permian?

Summary

- In this head to head, I am going to see which of these independent oil producers - Pioneer Natural Resources Company or Devon Energy Corporation - is competing the hardest for our investment dollars.

- Each company will be evaluated on Dividends, Debt & Dollars, and Dirt (yes, DIRT!).

- The winner will be considered the best of the Permian.

bjdlzx

Thesis

In this article I will compare, head-to-head, two big names of the Permian Basin. The winner will be based on the following metrics for both Devon Energy Corporation (NYSE:DVN) and Pioneer Natural Resources Company (NYSE:PXD).

- Dividends - which company has the best shareholder return model.

- Debt & Dollars - a measure of overall management performance and forward flexibility.

- Dirt - a measure of the physical asset we are investing in. Whoever has the best acreage should (over the long haul) provide the best returns.

A Quick Look

Before we get started, let's take a look at each company. Both DVN and PXD have similar business models as independent oil and gas producers. Pioneer operates strictly in the Midland Basin, while Devon is slightly more diverse. Devon produces roughly 67% of its output from the Delaware Basin (the next-door neighbor to the Midland Basin, but we'll touch on that later). The rest of its production is sprinkled amongst the Eagle Ford, Anadarko, Powder River, and Williston Basins.

Both companies cash flows are derived from commodity prices. Due to the volatility this can create, both companies have created, a variable shareholder return model. Pioneer is the larger company of the two, coming in at a $48 billion market cap, compared to $35 billion at Devon.

DIRT

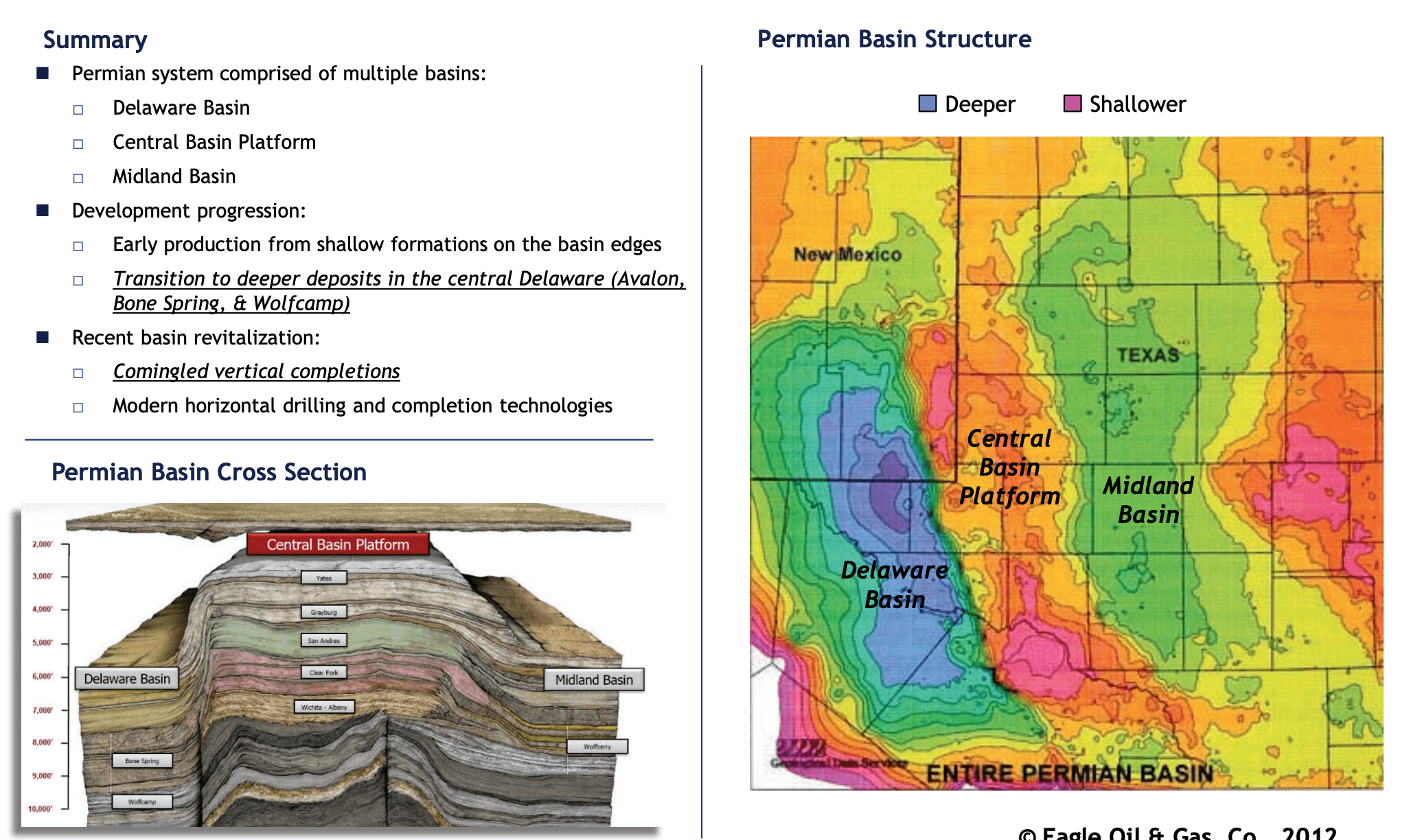

Ultimately when investing in an oil/gas producing entity, we must remember that the quality of property they own will be the limitation to their success. Poor quality wells will produce poor financial returns. The main focus of this discussion will compare and contrast the Midland Basin and the Delaware Basin, both of which are located in West Texas and Southern New Mexico.

Going back over the last 10 years or so, Devon and Pioneer owned property in both basins. Interestingly, each company progressively sold their acreage in the opposing basin to become focused and have developed into their current form. In 2016, Devon sold its Midland Basin property to Pioneer for $435 million. In 2021, Pioneer also swapped its basin profile away from the Delaware Basin as part of a $3 billion deal.

Midland Basin

The Midland Basin is Pioneer's heart and soul. It is fully committed to that territory and has been able to produce excellent results. The Midland Basin is located just east of the Delaware Basin. One of different physical aspects of the Midland versus the Delaware is that the Midland Basin is in the ballpark of 2,000 ft higher in elevation to the oil producing layers of the basin such as the Wolfberry or the Wolfcamp. This gives Pioneer a distinct cost advantage, having to drill through 2,000 less feet of rock to reach their product. Pioneer uses this advantage to yield one of the lowest production costs per BOE in the industry.

Depth Profile of the Midland and Delaware Basins (Search and Discovery Article #10412)

Delaware Basin

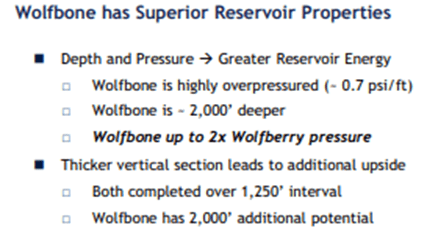

If it's easier to get to the oil products in the Midland Basin, why on earth would someone bother drilling in the Delaware Basin? Being 2,000 feet deeper isn't necessarily ALL bad. The additional rock overhead creates more pressure and thus more oil can be extracted per well. This does create the potential for higher ROIs if the wells are drilled and executed correctly.

Delaware Vs. Midland Basin Properties (Search and Discovery Article #10412)

Diversity

Devon has roughly 1/3 of its production in other basins. These basins include the Eagle Ford, Power River, Williston, and Anadarko. In the aggregate, these basins carry roughly the same margin as the Delaware. The benefit to having some diversity is some sheltering from weather risk. A winter storm or hurricane in Texas can take entire systems offline and reduce output (as was seen in Q4). By having some assets in other regions, this risk is somewhat mitigated. I categorize this as a small, rainy day, advantage for Devon.

Acreage Continuity

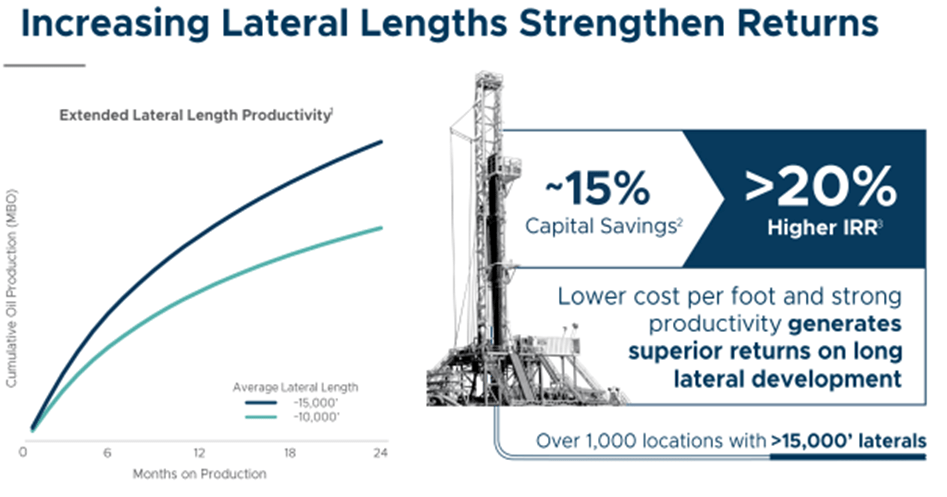

Another important variable when evaluating a company's acreage is the continuity of the entire property portfolio. Having large blocks of continuous property allows for longer lateral drilling and a higher ROI per well due to capital efficiency.

The industry has been pushing the envelope to reach 3-mile lateral lengths to boost the overall returns of their wells. Since hundreds of wells are drilled every year by both companies, large swaths of territory are needed to facilitate this capital efficiency push. Therefore, a company who has pockets of acreage would be disadvantaged to one who owns large blocks.

ROI Growth for 3 Mile Laterals (PXD Earnings Presentation)

The following two figures will compare the bulk of both Devon's and Pioneer's acreage. Devon certainly has solid operating pockets but cannot be truly compared to Pioneer's almost entirely continuous acreage. The pros and cons of the Delaware and Midland Basins can be called a push in my opinion. The point goes to PXD on this one for having the best opportunity to maximize its acreage.

Devon Acreage Map (DVN Earnings Presentation) Pioneer Acreage Map (PXD Earnings Presentation)

Dividends

Devon has a stated goal of returning 50% excess free cash flow to shareholders after the base dividend is paid in the form of a variable dividend. Currently the base dividend is $0.20/quarter, or roughly 1.5% at $55/share. Beyond that, the company executes buybacks opportunistically and are not included in the 50% goal.

Conversely, Pioneer pays back 75% of free cash flow ("FCF") following the base dividend (roughly 2.2% at $200/share) and also buys back shares in addition to the dividend policy. Pioneer has been so generous to its shareholders that it has paid out over 100% of FCF in both Q3 and Q4 of 2022 (108% and 103% respectively when factoring in buybacks). This obviously cannot be sustainable for the long term without taking on debt. Because of this, I put a personal asterisk by the overall payout for Pioneer, but not to diminish that the company is truly delivering for its shareholders.

At this point, it's easy to see a clear difference in shareholder returns. Most would say Devon shouldn't even be in this discussion based on the previous two paragraphs. But we should be asking ourselves the following question.

What is Devon doing with the 25% that Pioneer is giving to their shareholders? Are they lining their pockets with cash?

The short answer is YES! Sort of, anyway.

Let us look at how Devon is spending its excess cash in 2022.

- DVN spent $1.8 billion to acquire Validus.

- DVN spent $865 million to acquire Rim Rock Oil and Gas.

- $2.665 billion total spent between the two purchases.

- Combined these acquisitions will net the company an additional output of approximately 60k BOE/day.

- Acquired acreage is adjacent to existing property to allow for longer lateral wells, thereby increasing capital efficiency.

This is where the return models diverge. Pioneer will give you cash today, while Devon is earmarking some shareholder cash for inorganic growth to generate cash tomorrow. To say which is strategy is superior may entirely depend on your age and financial goals. The younger you are, the more willing you may be to leave some cash on the table to benefit you later. To decide the victor here I will go with the old tried and true motto, "Cash is King." The score is now 2-0 PXD.

Debt & Dollars

To measure the work of the management team, we must evaluate the financial condition the company is operating under. We will compare the debt and cash profiles of both companies as well as the cost of said debt on a per share basis.

| Total Debt | Interest Rate | Interest Cost | Cash Reserves | |

| Devon | $6.4 Billion | 5.8% | $0.14/share/quarter | $1.5 Billion |

| Pioneer | $4.9 Billion | 1.6% | $0.33/share/quarter | $1 Billion |

Pioneer has the obvious advantage in both total amount of debt and terms of that debt. An average interest rate of 1.6% is hard to compete with and in all honesty is not something that can be replicated. Devon does have a slightly better cash position, especially when considering it has the smaller market cap of the two companies.

Near-Term Maturities

Since both of these investments are aimed at cash production for their shareholders via FCF, one thing that can get in the way is a debt maturity. Over the next 3 years Devon has $1.2 billion in debt coming due, barring any refinancing activity. Conversely, Pioneer has $1.7 billion due in that same timeframe. This comes out to be fairly equivalent debt loads (Devon's is slightly less) when compared to the difference in market cap of the two companies.

Somehow, Pioneer's fantastic debt profile works against them when we look at the maturity dates. The company can either pay off the debt and take the huge hit to FCF. This will jeopardize the payout of the variable dividend. The other option is to refinance into a loan that will be at a considerably higher interest rate. For example, paying off the 2023 notes will burn $750 million that can't be returned to shareholders (and doesn't even help by saving on interest costs). At the same time, refinancing a 0.55% interest loan, into something that can only assumed to be 5% interest or more, would be just embarrassing.

It is hard to refute an average debt profile of 1.6%, and for that reason alone, this section has to be awarded to Pioneer. The score is now 3-0 PXD.

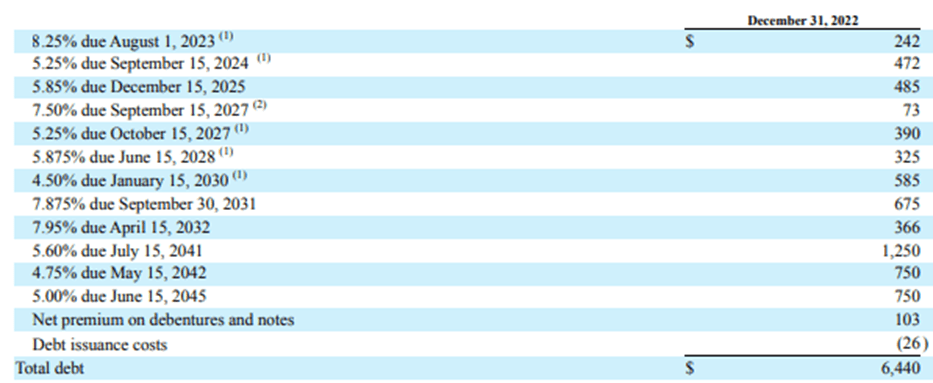

Devon Energy Debt Profile (DVN Form 10-K) Pioneer Natural Resources Debt Profile (PXD Form 10-K)

The Risks

Both companies operate in the commodities space and thus their earnings can fluctuate wildly. Unfortunately, this is largely out of their control. In one of my previous articles, I discussed the potential near term impacts that face Devon. Pioneer is in the same business and therefore the thesis is applicable.

Both companies have done an excellent job of maintaining a low breakeven operating structure despite inflationary pressures. Breakeven is roughly $40/barrel, WTI. This level is sufficient to fund operations and CAPEX for 2023, which we have been well above so far this year.

Per the EIA, over the last 10 years, oil prices have averaged about $65/barrel. The downside risk is real however, as prices have flirted with breakeven in 3 out of the 10 years. That is why I stress the need to be patient, waiting for an entry point that protects against capital losses. At this time I believe there is adequate support to oil prices to preclude any near term fall out.

Summary

The "official" score has Pioneer Natural Resources Company for the win with a final score of 3-0. I think the overall contest is closer than the score would indicate. Here are the highlights of each discussion.

- The Delaware and Midland basins have contrasting qualities between cost and oil production. Pioneer has a more continuous block of acreage allowing it to drill lateral runs that are longer and thus more capital efficient. Pioneer was awarded the point for that reason.

- Pioneer has a 75% cash return model plus buybacks. Devon only returns 50% cash plus buybacks. Pioneer was awarded the point because "Cash is King." Readers should not dismiss that Devon's model allows management more flexibility for acquisitions to fund external growth. If you are not solely focused on income as your financial goal this could be useful.

- Pioneer's debt levels and metrics are nothing short of phenomenal. An average interest rate of 1.6% was good for the last point in our head to head.

Both companies do an excellent job of rewarding shareholders but Pioneer takes the edge as a total package from a cash perspective. Devon Energy Corporation may be more suited for an investor looking for a combination of cash and growth as more of the profits stay internal to the company. Most importantly, investors should remember it is okay to own both companies for a blended position.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of DVN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.