Spirit Airlines: Most Likely No Deal But Potentially 87.65% Upside

Summary

- The market believes the Spirit Airlines, Inc. - JetBlue Airways Corporation deal is as good as dead.

- If it fails, I'm not sure the sustained downside is all that intimidating.

- Meanwhile, there are interesting advance payments and the tiny probability of a miracle close.

- Looking for a portfolio of ideas like this one? Members of Special Situation Report get exclusive access to our subscriber-only portfolios. Learn More »

Justin Sullivan

Spirit Airlines, Inc. (NYSE:SAVE) is likely being acquired by JetBlue Airways Corporation (NASDAQ:JBLU) for $31 per share and change (more about that later). This heavily contested merger is receiving a lot of (anticipated) regulatory attention. Maybe it is receiving even more attention than anticipated. It was first announced on April 5, 2022.

From January 2023, SAVE shareholders get $0.10 per month from JetBlue as an advance payment. This is added to the $31 amount although JetBlue won't pay more than $32.15 in total.

Monday, SAVE dropped 8.76% as it appeared:

the Department of Transportation and Department of Justice are looking to halt the deal on the grounds that the merger would be anti-competitive, according to Bloomberg. The outlet said that a suit could be filed as soon as Tuesday by the DOJ.

I like that you can get $0.10 per month while fighting to get the merger through. If it gets through in some way, the upside is fantastic. The stock is trading at ~$16.52, while the offer is for $31. That's 87.65% upside. Even the monthly ticking fee is substantially similar to an 8% yield (beware of taxes, though).

The likely outcome (as per the market) seems to be for the deal to fail.

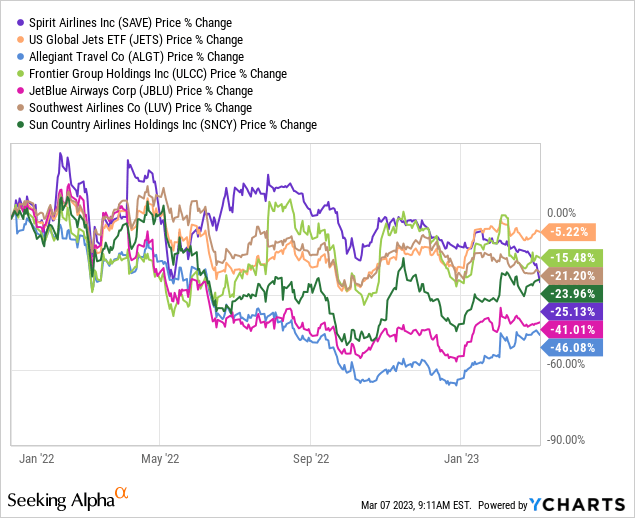

However, it appears as if that's at least partially priced in. The U.S. Global Jets ETF (JETS) as well as a number of competitors (used by Barclays as a peer valuation group in the merger agreement) have traded down since early 22'. I have deliberately referenced January 1, 2022, below instead of the merger announcement date because something of a bidding war had been going on.

JetBlue and Allegiant Travel Company (ALGT) are the only peers that have done worse.

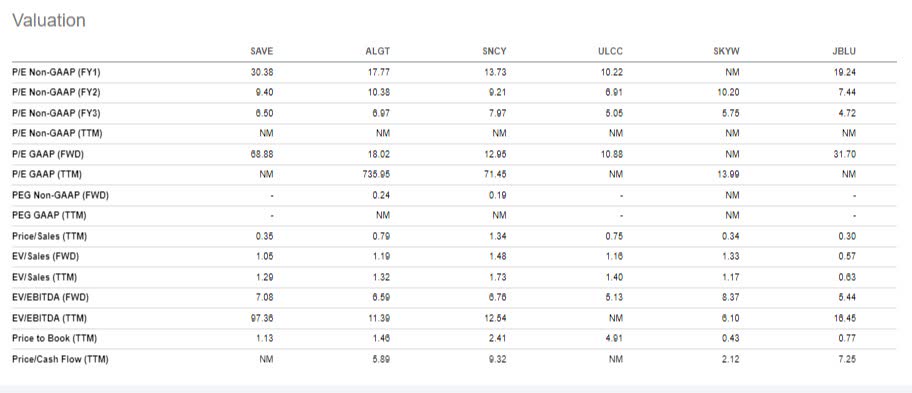

When I pull up valuations from a group of airline competitors (the above group + 1), the valuations of SAVE already appear to be in-line. There is not much sign of a merger premium except in the P/E line. Current elevated investments pretty easily skew a P/E line. I think EV/EBITDA, EV/sales, and even P/B are a bit more likely to be representative.

Spirit Airlines Peer Valuations (Seeking Alpha)

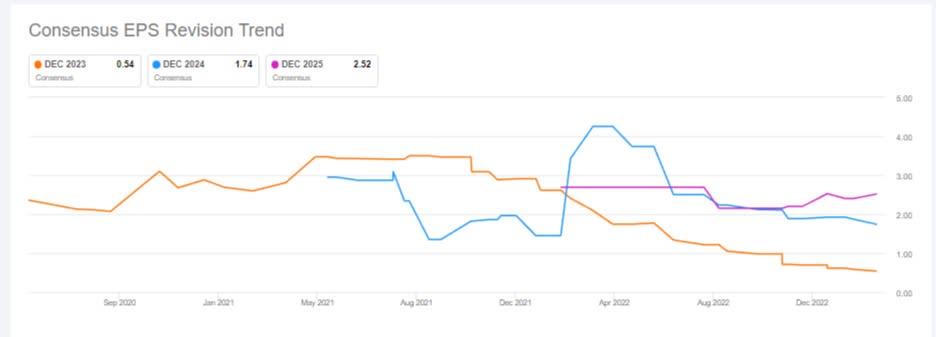

It has to be said that the earnings profile, especially 2023, has disappointed analysts since the deal announcement. That's roughly consistent with the price action we've already seen.

Spirit Airlines EPS (Seeking Alpha)

If this deal breaks, I'm not sure SAVE will need to trade down another 15%-20% on a sustained basis. There is also a break free, but it is admittedly small and won't help much.

Meanwhile, Spirit Airlines, Inc. shareholders receive $0.10 per month from JetBlue which helps quite a bit with downside protection especially if the legal fights are protracted. One of the problems with this merger is that the deal break risk is apparently so great that it vastly outweighs the probability the deal will go through. That means there is a lot of general market risk associated with holding the shares. Some of that risk could theoretically be offset by shorting a basket of airlines (like referenced above) against the long position. Alternatively, shorting an ETF like the U.S. Global Jets ETF could do that job.

Having said that, the JETS ETF seems much less volatile than some of the companies in the peer group. Theoretically, I see a long position in SAVE with a short position in JETS or peers as a market-neutral trade. There will be a downside on a deal break, but I expect the monthly ticking payments substantially offset it (the later the deal fails, the better). Meanwhile, there is the possibility of a massive ~87% upside for Spirit Airlines, Inc. if the deal surprisingly closes after all.

This article was written by

I gravitate towards special-situations. That means situations around companies or the market where the price can move in a certain direction based on a specific event or ongoing event. This eclectic and creative style of investing seems to suit my personality and interests most closely.

Since 2020 I host a podcast/videocast where I discuss (special-situation/event-driven) market events and investment ideas with top analysts, portfolio managers, hedge fund managers, experts, and other investment professionals. I highly recommend it (pick episodes around topics that interest you) for the amazing guests that come on with regularity.

I've been writing for Seeking Alpha since 2013 after playing p0ker professionally. In 2018 I founded Starshot Capital B.V. A Dutch AIF manager. Follow me on Twitter @Bramdehaas or email me Dehaas.Bram at Gmail

Disclosure: I/we have a beneficial long position in the shares of SAVE either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.