KIO: Rights Offering Results

Summary

- KIO's offering was oversubscribed.

- NAV/share took a significant hit due to dilution.

- Sell and rebuy would have worked again.

- Looking for more investing ideas like this one? Get them exclusively at CEF/ETF Income Laboratory. Learn More »

Author's note: This article was released to CEF/ETF Income Laboratory members as part of the CEF Weekly Roundup on February 21, 2023, with certain numbers updated. Please check the latest data before investing.

KIO rights offering results

KKR Income Opportunities Fund (KIO) has announced the results of their rights offering. We discussed this when it was first announced in a previous CEF Weekly Roundup (public link). From the press release:

KKR Income Opportunities Fund Announces the Results of Its Rights Offering

February 17, 2023 11:06 AM Eastern Standard Time

NEW YORK--(BUSINESS WIRE)--KKR Income Opportunities Fund (NYSE: KIO) (the "Fund") today announced the preliminary results of its transferable rights offering (the "Offer"). The Offer commenced on January 23, 2023 and expired on February 16, 2023 (the "Expiration Date"). The Offer entitled the rights holders to subscribe for up to an aggregate of 6,780,105 common shares of beneficial interest of the Fund ("Common Shares"). The subscription price for the Common Shares to be issued was $10.75 per Common Share, which was determined based on a formula equal to 82% of the Fund's net asset value ("NAV") per Common Share at the close of trading on the New York Stock Exchange ("NYSE") on the Expiration Date which was greater than the formula of 92.5% of the average of the last reported sales price of a Common Share on the NYSE on the Expiration Date and each of the four (4) immediately preceding trading days. The Offer was over-subscribed. The Common Shares subscribed for will be issued promptly after completion and receipt of all shareholder payments and the pro-rata allocation of Common Shares in respect of the over-subscription privilege.

This was a transferable 1-for-3 offering with a subscription price that was the higher of 92.5% of market price or 82% of NAV, with the market price being defined as the average of the closing market price of the fund on the final five days of the offering. The ex-rights date for the offering was January 20, 2023, while the offer expired on February 16, 2023.

Significant NAV/share dilution

The final offering price was $10.75, which was 82% of the NAV ($13.11) of the fund at expiry and a discount of -5.78% to the closing market price ($11.41) on the expiry date. The offering was oversubscribed, allowing the fund to grow its share count by the maximum of +33.3%. Together with a 3.50% sales load charged by UBS, the dealer manager for this rights offering, the hit to the NAV is very large, estimated to be -5.22% by my calculations.

We can see the effect of this dilution on KIO's NAV, which dropped by -4.23% on February 23, 2023. The NAV drop was less than my estimate because the high-yield bonds rose for the day (e.g., SPDR Bloomberg High Yield Bond ETF (JNK) gained +1.0%).

CEFConnect

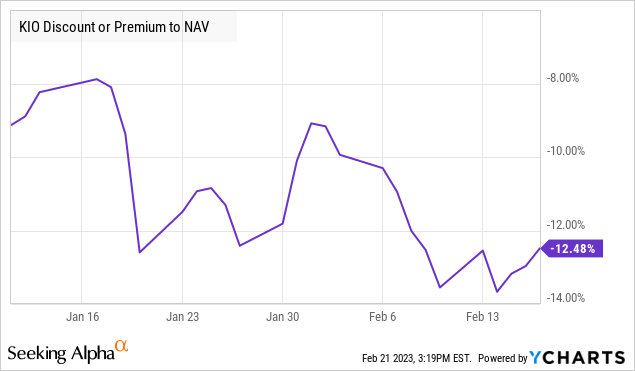

Sell and rebuy would have worked again

Surprisingly, KIO held relatively steady throughout this rights offering period. KIO's discount did widen to a low of -13.67% a few days before the offering expired, although still some ways from the subscription discount floor of -18%.

YCharts

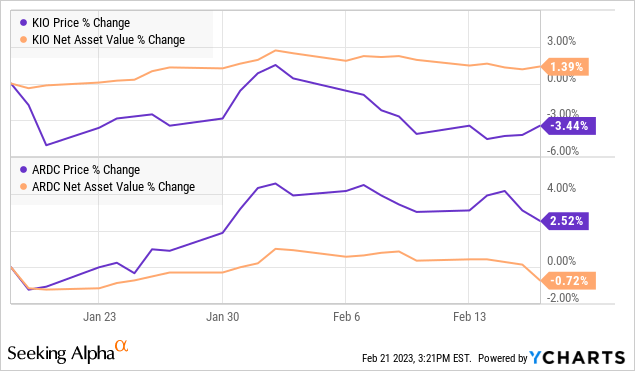

Nevertheless, the "sell and rebuy" strategy would still have been beneficial overall compared to buy-and-hold. As we previously wrote:

For investors who do not wish to expand their share count in KIO, I would recommend selling the fund before the ex-rights date of January 20th, 2023. History has shown that CEF prices tend to drift lower over the course of the offering period, so one can potentially rebuy the shares at a lower price once the offering concludes. To reduce market risk, one can switch to a similar fund like Ares Dynamic Capital Allocation Fund (ARDC) or Apollo Tactical Income Fund (AIF) over the course of the offering.

As it stands right now, an investor who sold KIO and bought ARDC could now rotate back from ARDC to KIO and gain around +6.2% "free shares" of KIO. As I always say, gaining free shares of a fund is better than subscribing (and paying) for slightly discounted shares, am I right?

YCharts

Going forward

cemagraphics

While KIO's senior loan exposure has increased the fund's income recently and allowed it to boost its distribution, the dilutive offering has negatively impacted distribution stability. Thus, the fund's 93.9% distribution coverage (per CEFData) should really be adjusted to around 89% once the NAV dilution is taken into account.

Don't know how to profit (or avoid losses) from CEF corporate actions?

We keep track of corporate actions such as rights offers, tender offers and mergers and how to profit from them in the members area of CEF/ETF Income Laboratory.

Check out what our members have to say about our service.

To see all that our exclusive membership has to offer, sign up for a free trial by clicking on the button below!

This article was written by

CEF/ETF Income Laboratory is a premium newsletter on Seeking Alpha that is focused on researching profitable income and arbitrage ideas with closed-end funds (CEFs) and exchange-traded funds (ETFs). We manage model safe and reliable 8%-yielding fund portfolios that have beaten the market in order to make income investing easy for you. Check us out to see why one subscriber calls us a "one-stop shop for CEF research.”

Click here to learn more about how we can help your income investing!

The CEF/ETF Income Laboratory is a top-ranked newsletter service that boasts a community of over 1000 serious income investors dedicated to sharing the best CEF and ETF ideas and strategies.

Our team includes:

1) Stanford Chemist: I am a scientific researcher by training who has taken up a passionate interest in investing. I provide fresh, agenda-free insight and analysis that you won't find on Wall Street! My ultimate goal is to provide analysis, research and evidence-based ways of generating profitable investing outcomes with CEFs and ETFs. My guiding philosophy is to help teach members not "what to think", but "how to think".

2) Nick Ackerman: Nick is a former Financial Advisor and has previously qualified for holding Series 7 and Series 66 licenses. These licenses also specifically qualified him for the role of Registered Investment Adviser (RIA), i.e., he was registered as a fiduciary and could manage assets for a fee and give advice. Since then he has continued with his passion for investing through writing for Seeking Alpha, providing his knowledge, opinions, and insights of the investing world. His specific focus is on closed-end funds as an attractive way to achieve income as well as general financial planning strategies towards achieving one’s long term financial goals.

3) Juan de la Hoz: Juan has previously worked as a fixed income trader, financial analyst, operations analyst, and economics professor in Canada and Colombia. He has hands-on experience analyzing, trading, and negotiating fixed-income securities, including bonds, money markets, and interbank trade financing, across markets and currencies. He is the "ETF Expert" of the CEF/ETF Income Laboratory, and enjoys researching strategies for income investors to increase their returns while lowering risk.

4) Dividend Seeker: Dividend Seeker began investing, as well as his career in Financial Services, in 2008, at the height of the market crash. This experience gave him a lot of perspective in a short period of time, and has helped shape his investment strategy today. He follows the markets passionately, investing mostly in sector ETFs, fixed-income CEFs, gold, and municipal bonds. He has worked in the Insurance industry in Funds Management, helping to direct conservative investments for claims reserves. After a few years, he moved in to the Banking industry, where he worked as a junior equity and currency analyst. Most recently, he took on an Audit role, supervising BSA/AML Compliance teams for one of the largest banks in the world. He has both a Bachelors and MBA in Finance. He is the "Macro Expert" of the CEF/ETF Income Laboratory.

Disclosure: I/we have a beneficial long position in the shares of ARDC either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.