Trex: Key Takeaways From 2022 Full Year Results

Summary

- Rising interest rates and inflation are squeezing the consumer and weighing on discretionary spending.

- Trex outlined how it's combating these pressures in its Q4 2022 and Full Year earnings release and conference call.

- There are a few key takeaways from the results, some I like and some I don't.

- Even with an uncertain economic outlook, I think Trex stock is GARP and a long-term winner.

karelnoppe

Trex Company (NYSE:TREX), the market-leader in composite decking, announced Q4 2022 and Full Year results on February 27. The market wasn't impressed, sending shares down 6% for the day.

During the earnings conference call, talks of inventory recalibration, throttling build-out of the Arkansas manufacturing facility, and tempered restocking levels amongst Distributors, didn't help matters.

It's no secret the US economy is fragile, with rising interest rates and annoyingly high inflation squeezing the consumer. New home sales are down, and discretionary spending is expected to take a hit. My 7 year old son knows this, yet it seems to be the sole focus of all Analysts covering Trex (and most other stocks).

During the Q&A session of the call, nearly every question was short-term in nature:

- How should we think about the Q1 guide for gross margin in comparison to Q1 2022?

- Your guide implies sales may be down 8-10% YOY. Can you break that down for us?

- Can you provide a little color on your operating margin being down 10 basis points YOY?

I exaggerate, but you get the point. I don't mean to make light of the current macroeconomic environment, but investing is a long-term game. I encourage you to read Trex's 10K and listen to the Full Year 2022 conference call for yourself.

I did, and here are a few of the key takeaways.

Proactive management team

One thing that stood out to me was Trex's ability to improve profitability in a tough economic environment. Q4 2022 gross margin came in at 34.1%, which was a 9.6% improvement over Q3 2022.

To me, this indicates management understands the business and can successfully navigate uncertain times. They recognized a shift in demand in early 2022, and pulled levers to maintain/improve operating results and profitability.

Bryan Fairbanks, President and CEO, provided these comments in the Q4 2022 earnings release:

Driving the sequential margin improvement was the full quarter benefit from the measures we took early in the third quarter to better align our cost structure with demand by decreasing production levels, right sizing our employee base, and focusing on cost efficiency programs. Further improvements are expected as we move through 2023 with the ongoing implementation of continuous improvement programs that will provide margin expansion opportunities.

Planning for $1 billion sell-through

Historically, Trex doesn't provide full-year revenue guidance; 2023 is no different. However, the company does provide quarterly guidance, which is revenue of $230 to $240 million for Q1 2023.

During the call, management made numerous comments about Trex's plan to produce $1 billion in product in 2023. They made it clear it wasn't a revenue guide per se, but one might infer Trex is expecting around $1 billion in revenue in 2023.

For context, Trex generated $1.1 billion in revenue in 2022, $1.2 billion in 2021, and $881 million in 2020. If Trex can generate somewhere near these numbers in the tough economic environment that is 2023, I'd say it's a win.

Share buybacks partially financed

I'm a big fan of share buybacks when the company has a lot of cash on the balance sheet, generates free cash flow (FCF), and has no good place to deploy capital for above average returns.

In 2022, Trex returned $395 million to shareholders through share buybacks. I like the sentiment. But I don't like how they appear to have financed a good portion of it.

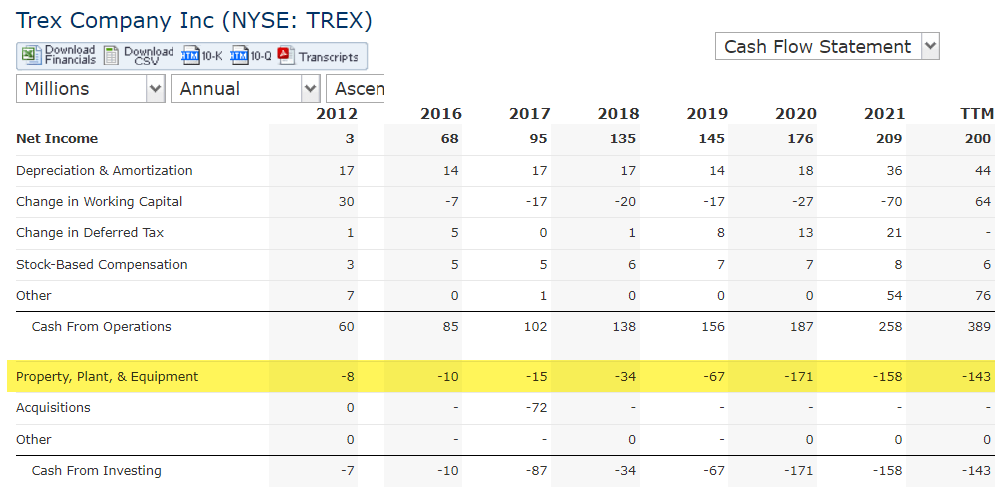

Here's a look at Trex's 2022 cash flow statement. It shows operating cash flow of $216 million and capital expenditures of $176M, which equates to $40 million in FCF.

TREX 2022 Cash Flow Statement (TREX 10K 2022)

I also noticed a substantial decrease in cash on the Balance Sheet, which makes sense given the buybacks, and a new $220 million line of credit coming due this year.

TREX Balance Sheet (10K 2022)

Is it cause for concern? I don't know, but it's worth keeping an eye on. Especially when considering Trex's guide of $130 to $140 million in capital expenditures this year.

It wouldn't surprise me to see another year of double digit FCF in 2023. Which begs the question, how will Trex pay off the $220 million coming due (Current Liabilities)? I assume they'll draw on additional credit, but it's not the ideal situation in my opinion.

Free cash flow should improve after Arkansas

Trex is in the early stages of a $400 million investment in its Arkansas manufacturing facility. The facility is being built to create capacity for future growth and to expand Trex's geographic footprint.

But the investment is capital intensive. Trex's capital expenditures have been >$150 million per year since 2020. Prior to that, the max Trex had spent in capex in any year was $67 million (2019).

Trex Cash Flow Statement (Quickfs.net)

Once Arkansas is complete, I anticipate Trex's capital expenditures will decrease considerably, which bodes well for free cash flow and shareholders.

Valuation

I'm currently a shareholder of Trex with an average cost basis of $59. So at $53 per share, I'm down around 10% as of this writing.

Trex is difficult to value because its P/E has varied widely over the past 5 years, and FCF is masked by the Arkansas investment. It may seem odd to value a GAAP profitable company using P/S, but it's been somewhat more consistent than most market multiples.

If you exclude the Covid years of 2020 and 2021, Trex's P/S averaged 6x across 2017, 2018, 2019, and 2022. The low was 5.0x in 2018, and the high was 7.1x in 2019.

With revenue expected to be around $1 billion in 2023, and 110 million in diluted shares outstanding, that puts a fair value of $54.50 ($1 billion x 6 / 110 million) on Trex shares.

Even if revenue came in nearer $900 million, the P/S puts shares at $49.

Conclusion

Given the long-term track record of Trex, I think shares represent growth at a reasonable price (GARP). While the company is bound to experience headwinds with reduced revenue and profitability in 2023/2024, I like the long-term prospects. And believe shares are priced low enough to take a nibble, perhaps even a bite.

Trex is a proven compounder and market-leader in composite decking. There's still a lot of market share up for grabs with the conversation away from wood. And I like Trex's chances for continued growth in the coming years.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of TREX either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.