Bengal Capital - XS Financial: Earning Good Risk-Adjusted Returns

Summary

- XS Financial is a cannabis specialty finance company.

- We believe that XS has a few underappreciated advantages.

- The Fund holds a position in XS equity, which is incredibly illiquid even by the standards of the Fund.

- In 2023, we will be looking for XS to continue to grow its leasing business.

Jikaboom/iStock via Getty Images

The following segment was excerpted from this fund letter.

XS Financial, Inc. (OTCQB:XSHLF)

XS Financial ("XS") is a cannabis specialty finance company focused on equipment leasing. The basic XS transaction looks like this: MSO Z is building a new cannabis growing/processing facility. It needs to outfit this facility with some equipment to make the facility work like extraction machines, growing lights, packaging automation, etc. While oftentimes the capex budget comes from REITs like IIPR, oftentimes that does not cover this type of equipment, so XS steps in to provide financing.

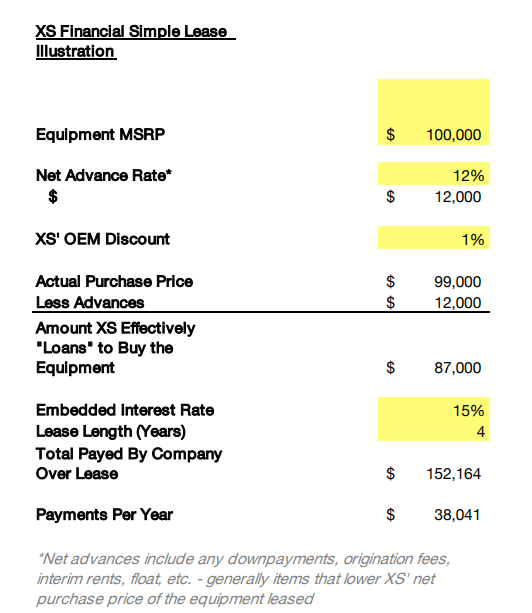

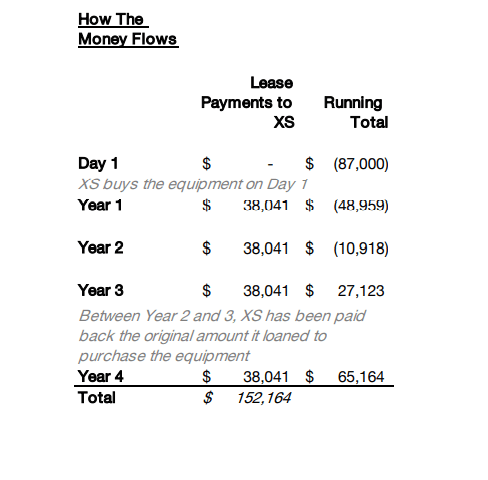

For example, let's say a packaging machine Z needs has an MSRP of $100,000. XS would generally get a small discount from the manufacturer off MSRP (say 1%), and also because of how its leases are structured it would receive certain advances (e.g., origination fee, interim rent, payment terms, etc.) that also reduce its initial exposure (say by around 12%, although the amount is anywhere from 10-15% as a general rule). It then leases the machine to Z in a lease that is fully amortizing over about four years with an embedded interest rate of 15% (which is XS' current portfolio yield, but this number will fluctuate with the market). Illustrations of the economics and how the money flows is below:

We believe that XS has a few underappreciated advantages, both generally and with respect to other cannabis lenders:

- Strong Management Team: XS' management team is confidence inspiring and has invested their own cash into the business. We believe they understand their function as debt providers well, and are deeply focused on long-term returns.

- More Effective Security Than a Cannabis REIT: Cannabis REITs' appear to have stronger security at first glance, and their legal documents certainly suggest as much, but we think that practically speaking XS enjoys as good or better security for a few reasons: (1) XS gets a return of its initial investment in around 2 and a half years vs. cannabis REITs that need to wait years (with their attendant disruption and price compression) to see similar results so the risk of losing invested capital is lower; (2) similarly to (1), XS is able to reprice its loans much more quickly than cannabis REITs, which have loaned for significantly longer terms; and (3) XS holds a primary security interest in the leased equipment and could, if necessary, foreclose on it. More so than the salvage value, which may be negligible and serves as a last ditch effort to recover owed monies, this is important because the type of equipment XS loans on is critical for a company's revenue generation - even a cannabis REIT has an interest in making sure that XS is paid because a built out cannabis facility with no equipment is just a pretty box that generates no revenue. Given all this, we feel that the safety of XS' loans is underappreciated. Although most of their borrowers are large MSOs which we criticized in our commentary, we think XS' unique position gives it a very high chance of being one of the first to be paid in a distressed situation.

- Potential to Build Strong Franchise Value: Many of the current cannabis REITs and other lenders can be boiled down to arbitrage - that is, they are raising money in one place and then loaning it in another to generate higher returns. Money is even more of a commodity than cannabis, so it is difficult to see the long run "franchise" value of the business these lenders are building. Not so with XS, where we see a significant benefit to scale in equipment leasing because of the ability to negotiate discounts with equipment manufacturers, centrally order equipment, and also centrally administer and track maintenance of the equipment. Indeed, our channel checks were unanimous that the XS team were a pleasure to work with, which indicated to us that XS is providing some kind of value to its customers beyond just loaning them money.

The Fund holds a position in XS equity, which is incredibly illiquid even by the standards of the Fund, and also has a side pocket investment of ~US$1 mm (original principal value) in XS' 8% convertible debt, which matures later this year in October 2023, although the company has an option to extend that for a year upon payment of a fee - an option we feel it more likely than not that they will take given that the cost of capital has since increased and the conversion price of CAD$0.35 is far from the current stock price of CAD$0.065, which implies a market capitalization of CAD$7mm.

Valuing a finance company depends strongly on assumptions regarding future returns and market capacity for financing. We feel any exercise in estimating these numbers beyond rough rules of thumb is just precision with the illusion of accuracy so we do not attempt to. That said, we are confident that XS is earning good risk-adjusted returns, that there is more capacity for this type of lending in the market - i.e., that XS has more loans to make beyond the ones that it has to this point - and that, eventually, this will lead to meaningful returns to equity.

In 2023, we will be looking for XS to continue to grow its leasing business to more clients, especially towards smaller cannabis operators with strong underlying cash flows to diversify away from larger MSOs, and monitoring any losses they experience.

DisclaimerThe information contained in this letter is provided for informational purposes only, is not complete, and does not contain certain material information about our Fund, including important disclosures relating to the risks, fees, expenses, liquidity restrictions and other terms of investing, and is subject to change without notice. This letter is not a recommendation to buy or sell any securities. The information contained herein does not take into account the particular investment objective or financial or other circumstances of any individual investor. An investment in our fund is suitable only for qualified investors that fully understand the risks of such an investment after reviewing the relevant private placement memorandum ("PPM"). Bengal Impact Partners, LLC ("Bengal Capital" or "we") is not acting as an investment adviser or otherwise making any recommendation as to an investor's decision to invest in our funds. Perhaps most importantly, Bengal Capital has no obligation to update any information provided here in the future, including if any positions discussed are sold or purchased, or if different positions are purchased. This document does not constitute an offer of investment advisory services by Bengal Capital, nor an offering of limited partnership interests of our Fund; any such offering will be made solely pursuant to the Fund's PPM. An investment in our Fund will be subject to a variety of risks (which are described in the Fund's definitive PPM), and there can be no assurance that the Fund's investment objective will be met or that the fund will achieve results comparable to those described in this letter, or that the fund will make any profit or will be able to avoid incurring losses. As with any investment vehicle, past performance cannot assure any level of future results. We make no representations or guarantees with respect to the accuracy or completeness of third party data used or mentioned in this letter. We provide services, such as strategic consulting services, to certain entities mentioned in this letter and may in the future provide such services to more in the future, or to companies not mentioned in this letter. While we may sometimes advise on issues regarding corporate communications, we do not believe any of the services which we provide are "stock promotion" - we have not been and will not be compensated for the mention or discussion of any of the companies discussed herein. We disclose such arrangements to investors in the Fund and will continue to do so. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

This article was written by