Sprout Social Sees Headwinds As Operating Losses Remain

Summary

- Sprout Social reported its Q4 2022 financial results on February 21, 2023.

- The firm provides a SaaS platform for social media monitoring and management activities.

- SPT has produced growing revenue but worsening operating losses.

- Given its rather hefty valuation and uncertain macroeconomic outlook, I'm on Hold for SPT in the short term.

- Looking for more investing ideas like this one? Get them exclusively at IPO Edge. Learn More »

Photosbypatrik

A Quick Take On Sprout Social

Sprout Social (NASDAQ:SPT) reported its Q4 2022 financial results on February 21, 2023, missing revenue but beating EPS consensus estimates.

The firm provides a social media management and tracking system to businesses.

Sprout is generating substantial operating losses and its valuation appears quite full, so I’m on Hold for SPT in the near term.

Sprout Social Overview

Chicago, Illinois-based Sprout Social was founded in 2009 and its platform enables businesses to manage social media engagement publishing and analytics, including brand awareness, reputation management, customer service, business intelligence, and customer acquisition.

Management is headed by founder, CEO, President and Director Justyn Howard, who was previously responsible for Enterprise Account Sales in Learn.com.

The firm mainly attracts customers through a product-driven strategy, where potential buyers are led to the firm’s website and sign up for a free trial of its products.

Sprout has a dedicated marketing team that is tasked with increasing awareness of the company’s platform via inbound marketing, through its own industry-related blog and other social content, as well as its own social media following.

Sprout Social’s Market & Competition

According to a 2019 market research report by Technavio, the global social media management software market is projected to increase by $789.43 million between 2019 and 2023, growing at a CAGR of 14% during the same period.

The main factors driving forecast market growth are the increase in social media advertising, the adoption of analytics in social media management [SMM] platforms and their benefits, such as better visibility over customer engagement and satisfaction as well as marketing effectiveness.

The Asia-Pacific region is projected to grow at a steady rate during the period, accounting for 32% of the anticipated market growth during the period.

Major market participants include the following:

Adobe (ADBE)

Brandwatch

Digimind

Emplifi

Hootsuite (HOOT)

HubSpot (HUBS)

Meltwater (OTC:MWTRF)

Qualtrics (XM)

Salesforce (CRM)

Sprinklr (CXM)

Zoho

Sprout Social’s Recent Financial Performance

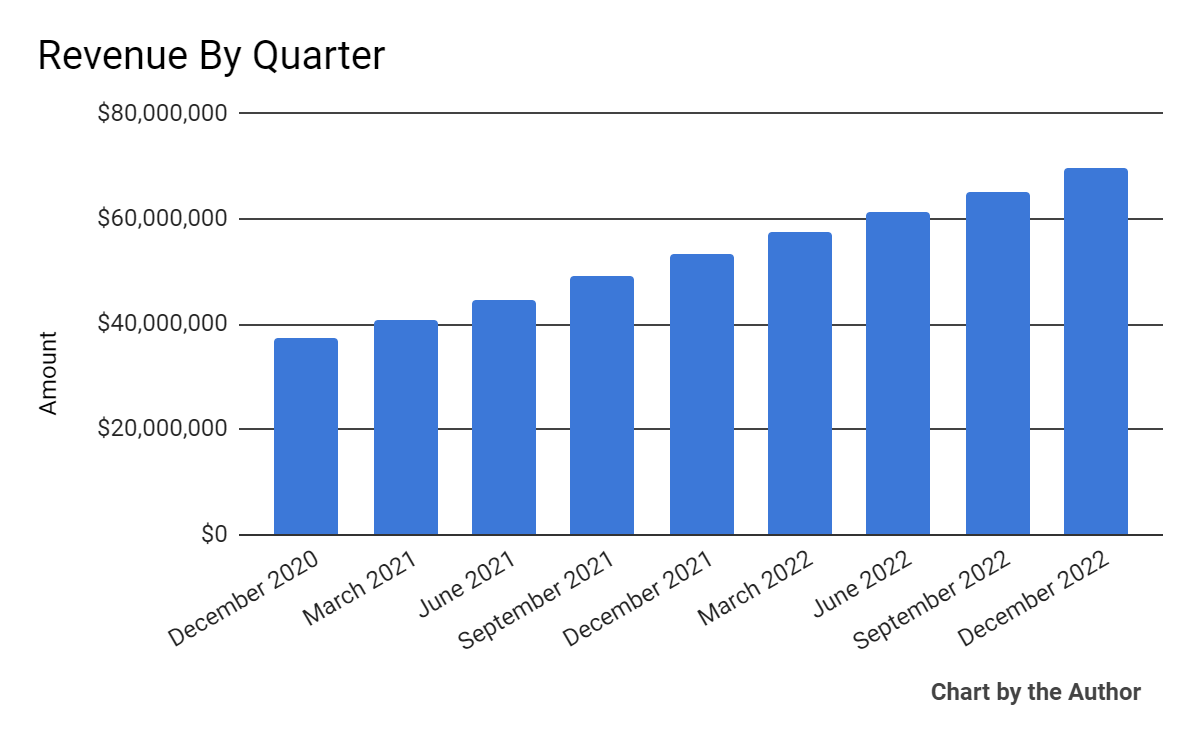

Total revenue by quarter has risen per the following chart:

Total Revenue (Seeking Alpha)

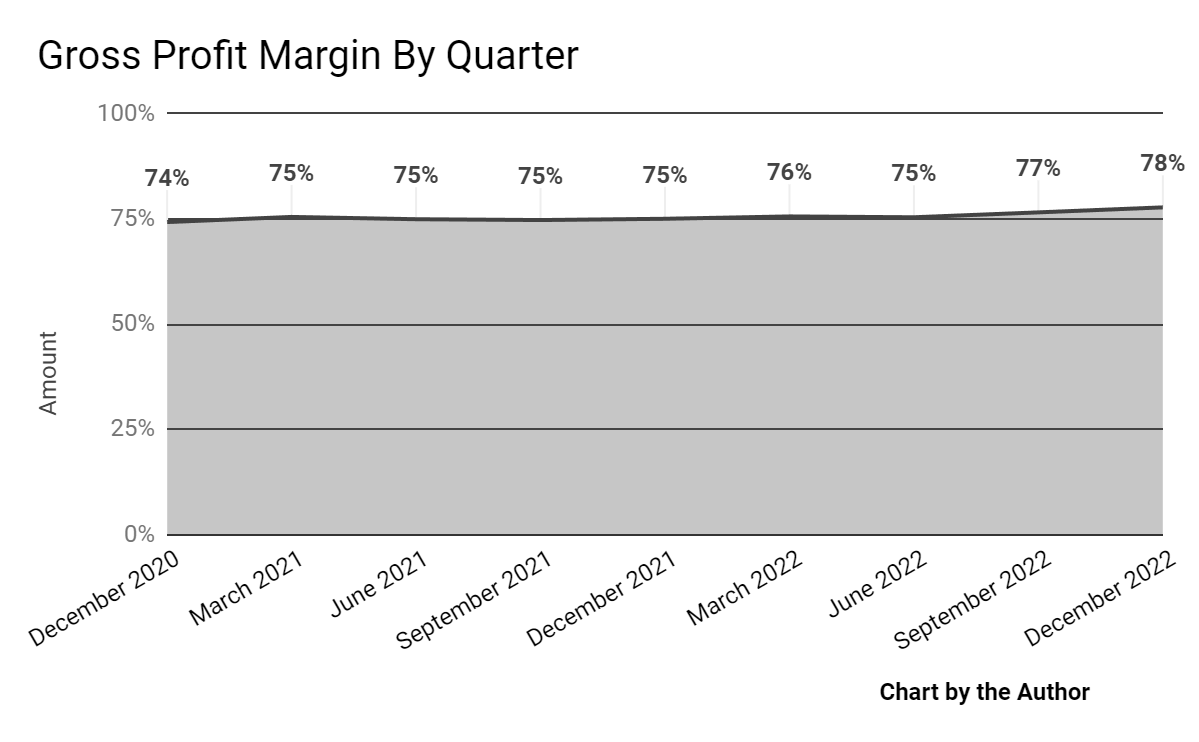

Gross profit margin by quarter has trended higher in recent quarters:

Gross Profit Margin (Seeking Alpha)

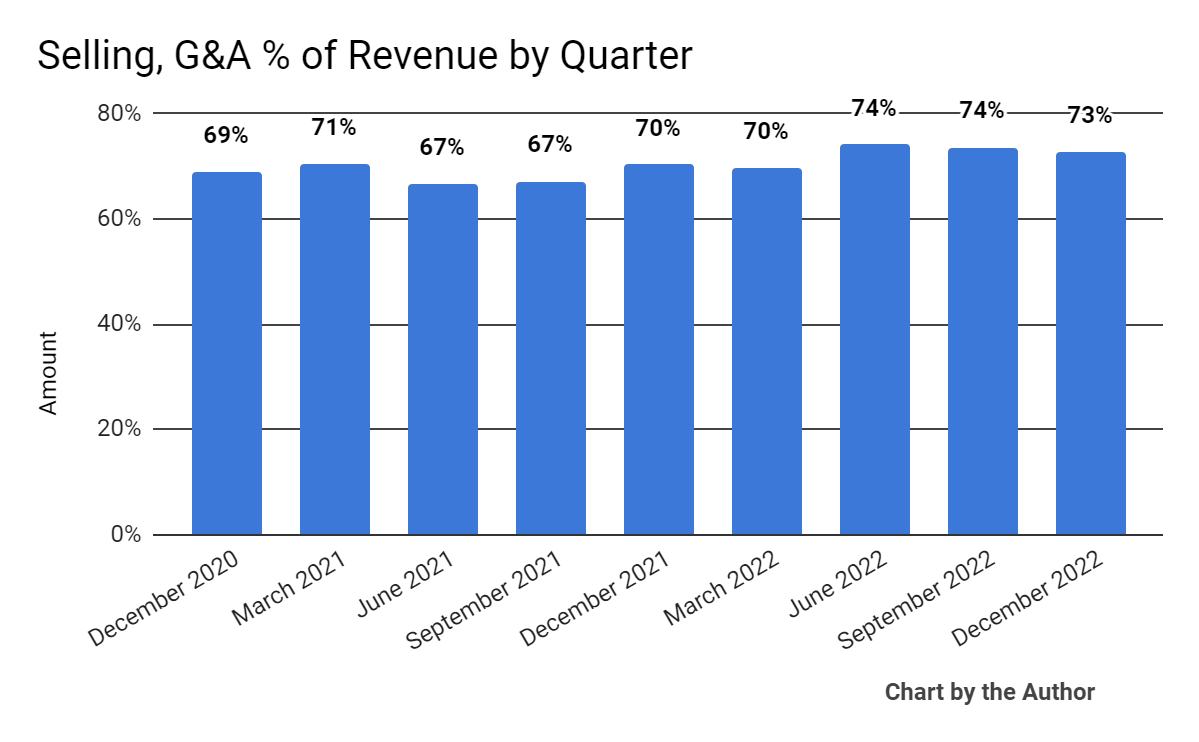

Selling, G&A expenses as a percentage of total revenue by quarter have also moved up more recently:

Selling, G&A % Of Revenue (Seeking Alpha)

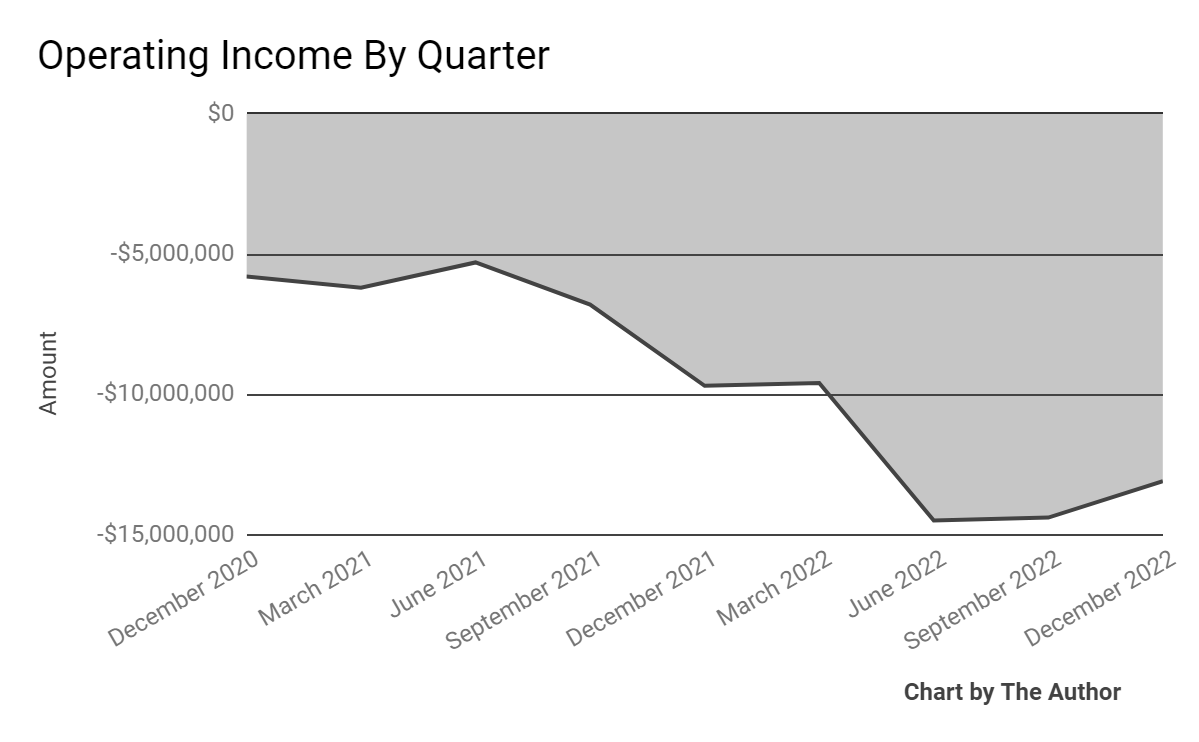

Operating losses by quarter have worsened in recent quarters:

Operating Income (Seeking Alpha)

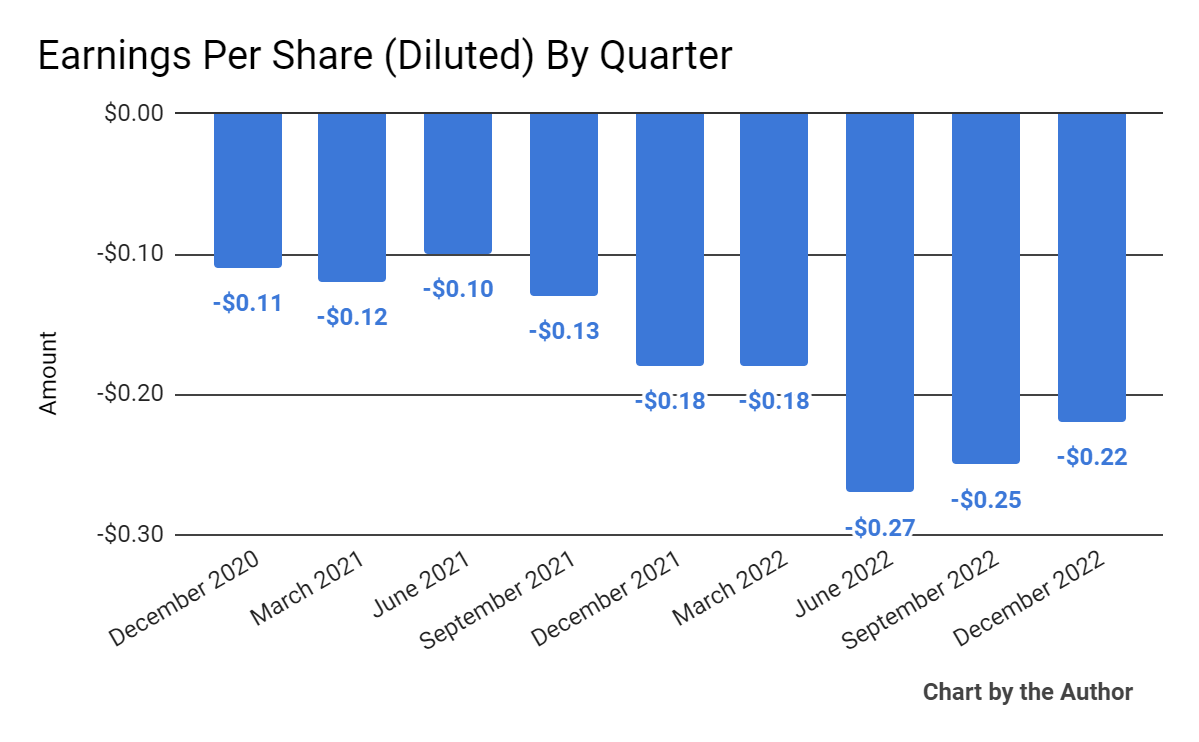

Earnings per share (Diluted) have also deteriorated further into negative territory in recent quarters:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

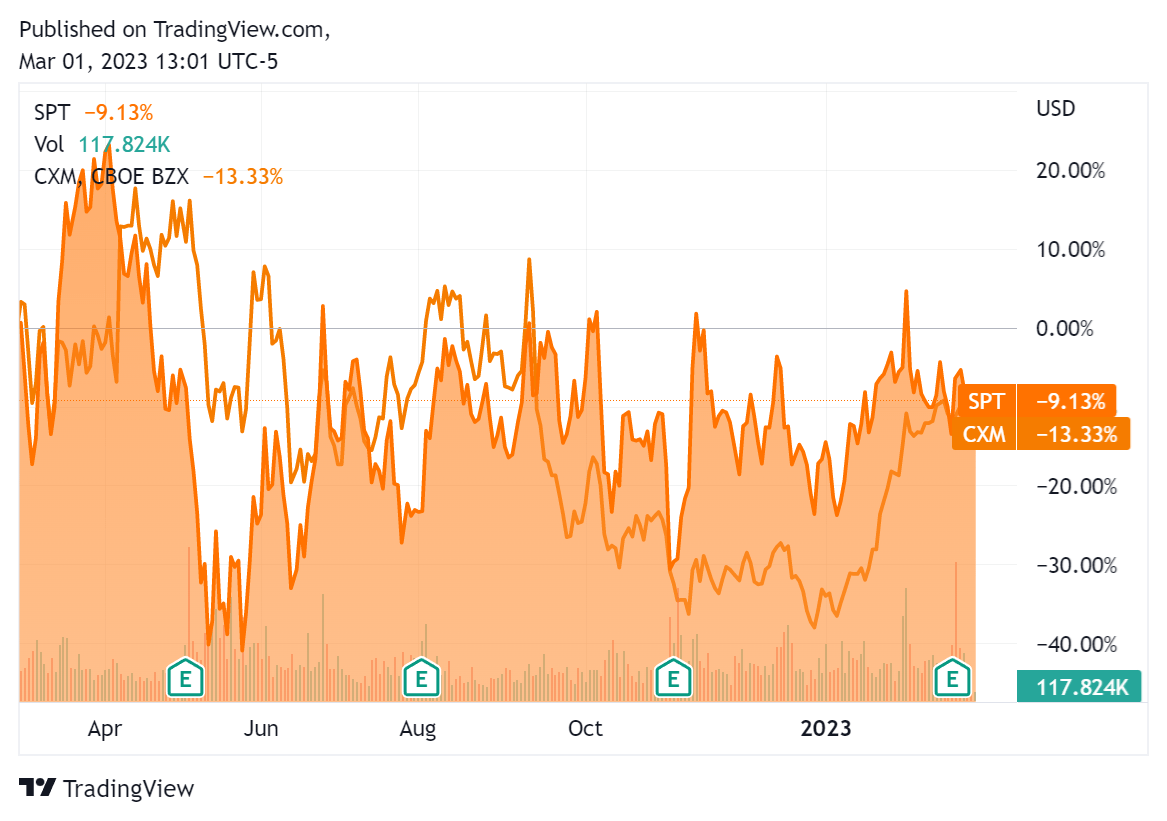

In the past 12 months, SPT’s stock price has fallen 9.1% vs. that of Sprinklr’s drop of 13.3%, as the chart indicates below:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Sprout Social

Below is a table of relevant capitalization and valuation figures for the company:

Measure [TTM] | Amount |

Enterprise Value / Sales | 12.6 |

Enterprise Value / EBITDA | NM |

Price / Sales | 13.1 |

Revenue Growth Rate | 35.1% |

Net Income Margin | -19.8% |

GAAP EBITDA % | -18.8% |

Market Capitalization | $3,360,000,000 |

Enterprise Value | $3,190,000,000 |

Operating Cash Flow | $10,670,000 |

Earnings Per Share (Fully Diluted) | -$0.92 |

(Source - Seeking Alpha)

As a reference, a relevant partial public comparable would be Sprinklr; shown below is a comparison of their primary valuation metrics:

Metric [TTM] | Sprinklr | Sprout Social | Variance |

Enterprise Value / Sales | 3.9 | 12.6 | 221.7% |

Revenue Growth Rate | 27.7% | 35.1% | 26.7% |

Net Income Margin | -15.6% | -19.8% | 26.6% |

Operating Cash Flow | -$10,400,000 | $10,670,000 | --% |

(Source - Seeking Alpha)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

SPT’s most recent GAAP Rule of 40 calculation was 16.3% as of Q4 2022, so the firm needs improvement in this regard, per the table below:

Rule of 40 - GAAP | Calculation |

Recent Rev. Growth % | 35.1% |

GAAP EBITDA % | -18.8% |

Total | 16.3% |

(Source - Seeking Alpha)

Commentary On Sprout Social

In its last earnings call (Source - Seeking Alpha), covering Q4 2022’s results, management highlighted growth in its net new ARR (Annual Recurring Revenue) due in part to expanding deal sizes with 59% year-over-year growth in customers paying the firm $50K per year or more.

This represents what management calls ‘upmarket momentum’, which when combined with success in its previous price increases, produced favorable growth results.

Its acquisition of Repustate will also improve SPT’s social listening and machine learning/AI capabilities across its platform.

As to its financial results, total revenue rose a strong 31% year-over-year and gained 132 net new customers to end the quarter with 34,390 customers in total.

The company's dollar-based net retention rate for all of 2022 was 109%, down from 112% in 2021, largely due to lower dollar growth among its SMB and agency segments.

The firm’s Rule of 40 result has been modest, with a positive revenue growth result offset by negative operating performance contributing to a mediocre figure for this metric.

SPT continued to hire employees, so its non-GAAP sales and marketing expenses rose, although this increase was offset partially by a drop in non-GAAP R&D expenses.

Non-GAAP figures usually exclude stock-based compensation, which in SPT's case has been significant.

GAAP operating losses and earnings per share have worsened in recent quarters, a disconcerting signal.

For the balance sheet, the firm finished the quarter with $172.8 million in cash, equivalents and short-term investments and no debt.

Over the trailing twelve months, free cash generated was $8.9 million, of which capital expenditures accounted for only $1.8 million. The company paid a hefty $47.7 million in stock-based compensation in the last four quarters.

Looking ahead, management expects revenue growth for full-year 2023 to be at 31% over 2022 and non-GAAP operating income to be $1.8 million at the midpoint.

Regarding valuation, the market is valuing SPT at an EV/Sales multiple of around 12.6x.

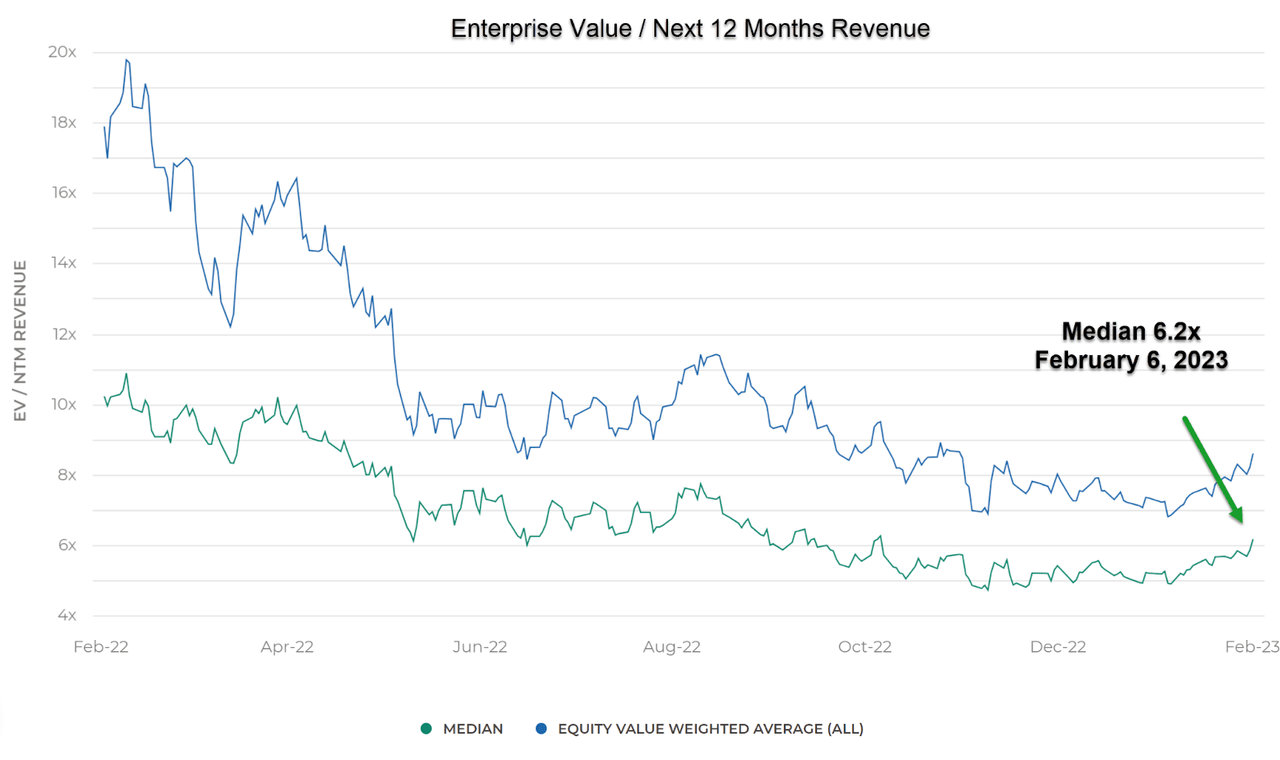

The Meritech Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 6.2x on February 6, 2023, as the chart shows here:

Enterprise Value / Next 12 Months Revenue Index (Meritech Capital)

So, by comparison, SPT is currently valued by the market at more than double the broader Meritech Capital Index, at least as of February 6, 2023.

The primary risk to the company’s outlook is a likely macroeconomic slowdown, which may produce slower sales cycles and reduce its revenue growth trajectory.

Given the firm’s worsening operating losses in a market that punishes money-losing technology companies and its substantial EV/Revenue multiple, I’m more cautious about SPT here.

My outlook for SPT in the near term is a Hold.

Gain Insight and actionable information on U.S. IPOs with IPO Edge research.

Members of IPO Edge get the latest IPO research, news, and industry analysis.

Get started with a free trial!

This article was written by

I'm the founder of IPO Edge on Seeking Alpha, a research service for investors interested in IPOs on US markets. Subscribers receive access to my proprietary research, valuation, data, commentary, opinions, and chat on U.S. IPOs. Join now to get an insider's 'edge' on new issues coming to market, both before and after the IPO. Start with a 14-day Free Trial.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This report is for educational purposes and is not financial, legal, or investment advice. The information referenced or contained herein may change, be in error, become outdated and irrelevant, or be removed at any time without notice. The author is not an investment advisor. You should perform your own research on your particular financial situation before making any decisions.