Snowflake is all set to report quarterly earnings on Wednesday.

Going into the Q4 ER, Snowflake's stock is finely poised, and a significant move to either side (up or down) is possible.

Based on management's history of sandbagging guidance and lowered analyst estimates, I think Snowflake can deliver yet another beat on earnings this quarter.

With that said, Snowflake is still a richly valued stock that demands perfect execution. Given the macroeconomic challenges, SNOW stock could be headed lower after its earnings report.

Overall, I like the idea of accumulating shares in Snowflake for a 5+ years investment at ~$145 per share using a DCA plan to perform staggered buying over 6-12 months.

We're currently running a sale at my private investing ideas service, The Quantamental Investor, where members get access to portfolios, market alerts, real-time chat, and more. Learn More »

FG Trade Latin/E+ via Getty Images

Introduction

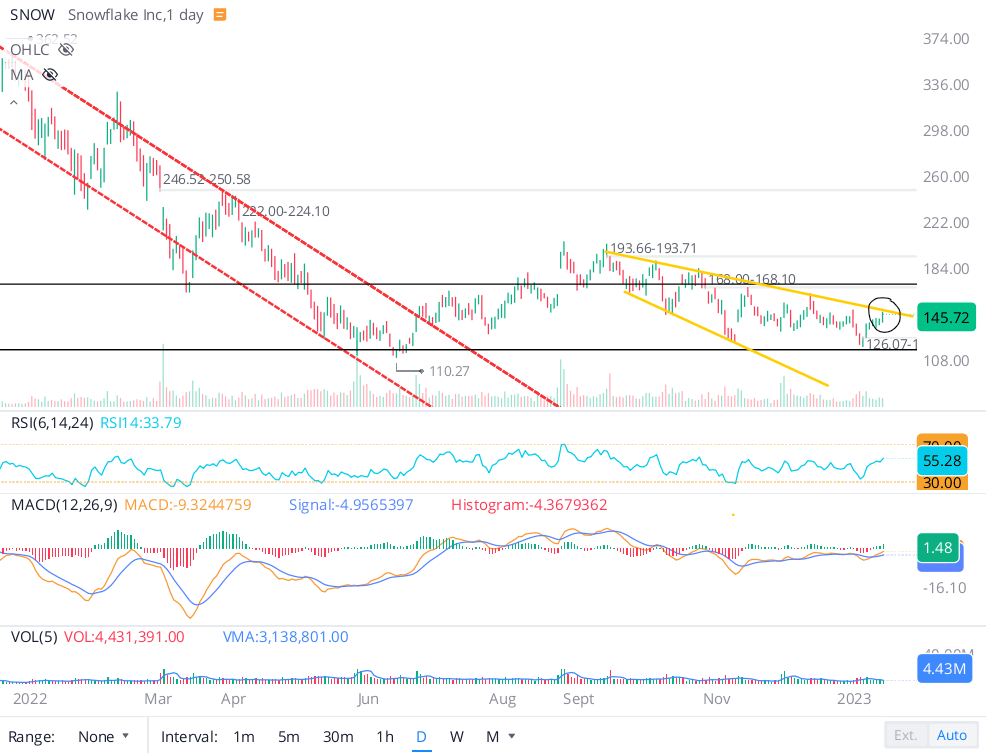

Snowflake's (NYSE:SNOW) stock has blown hot and cold to go nowhere since I last covered it in January. Back then SNOW was trading at ~$145, and here's what I wrote at the time:

In the last week or so, SNOW's stock bounced up from the ~$124 level, and I now view the $120-$170 range as the Stage-1 base for the stock. Currently, we are sitting right in the middle of this base, and if the recent rally extends, SNOW could test the upper end of the base at $170.

As you can see on the chart above, I have drawn a megaphone pattern on the right side. Snowflake's stock has turned back down from the upper trendline (drawn in yellow) for several months now, and this could happen again. Hence, a re-test of $120 (lower end of the base) is the more likely outcome for SNOW.

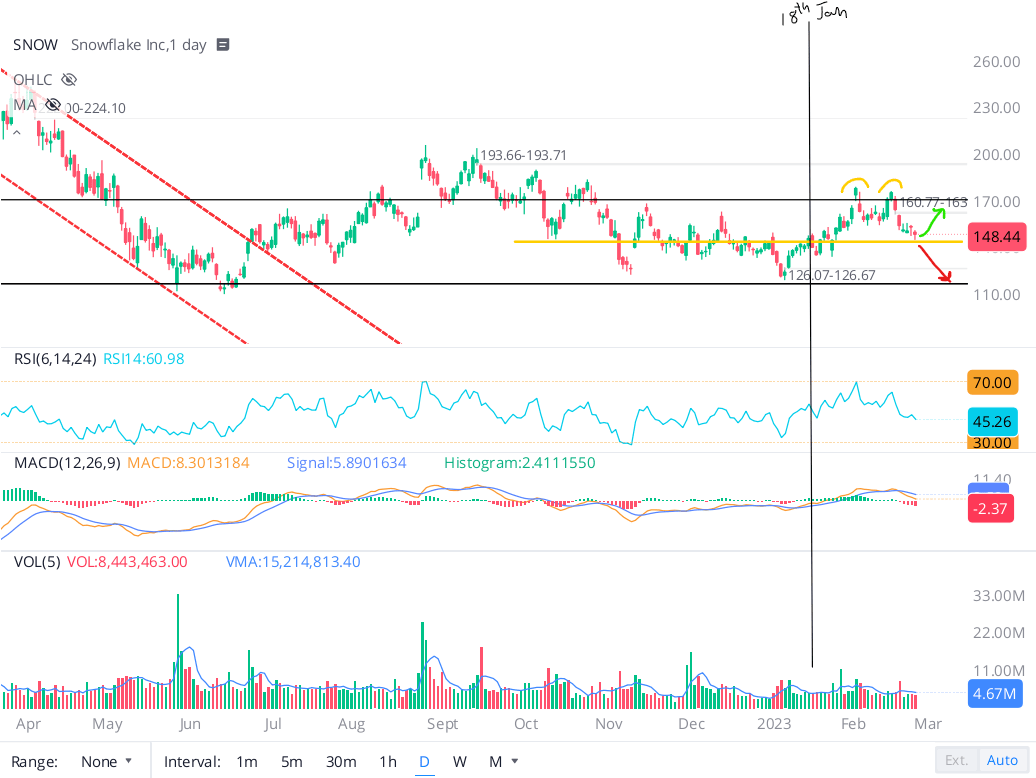

The year started with a tremendous rally in equities, with long-duration assets like Snowflake bouncing higher as interest rates retreated and financial conditions loosened up to early-2022 levels. As you can see on the chart below, Snowflake rallied up to the higher end of its Stage-I base and even breached it temporarily in late January. However, interest rates have climbed back to YTD highs in February, and Snowflake's stock has been in retreat over the last few weeks.

Heading into its Q4 FY2023 earnings report on Wednesday, 1st March 2023, SNOW is once again sitting smack in the middle of the Stage-I base we have been talking about recently. Now, as I see it, the recent rejection from the top of the base is looking like a local double top. If Q4 results fail to live up to expectations, I think we could finally see that move down to the lower end of the base at $120. On the flip side, a strong report could propel SNOW's stock back up to the upper end of the base ($170), and then maybe, we could get a real breakout to the upside at the third time of asking!

In this note, I will provide a preview of Snowflake's Q4 FY2023 report and share my rationale for investing in SNOW at the current levels.

What Is The Earnings Forecast For Snowflake?

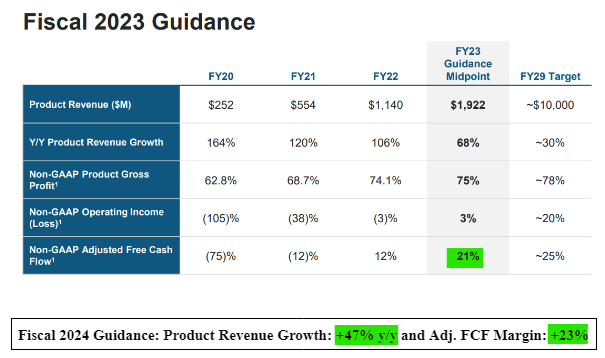

For Q4 FY2023, Snowflake's management has guided for Product revenues of $535-$540M (growth of ~49% y/y, ~3% q/q), which if true, would mark a sharp deceleration in revenue growth rates for the data cloud pioneer.

Snowflake Q3 ER Presentation

During the Q3 FY2023 earnings call, Snowflake's management clarified that Q4 tends to have a higher number of holidays, and since 70% of Snowflake's revenues are generated by humans interacting with its platform, revenues tend to be weaker in this quarter. Hence, the potential revenue growth deceleration we might see for Q4 is not a massive concern. And I say so with the utmost confidence because Snowflake's management has a history of sandbagging their guidance (& outperforming estimates).

SeekingAlpha

As of the publication of Snowflake's Q3 FY2023 earnings report, its management's business outlook for FY2024 (2023) looked robust, with SNOW projected to deliver ~47% y/y revenue growth in 2023 based on their current consumption patterns despite a poor macroeconomic environment.

How Was SNOW’s Previous Earning Report?

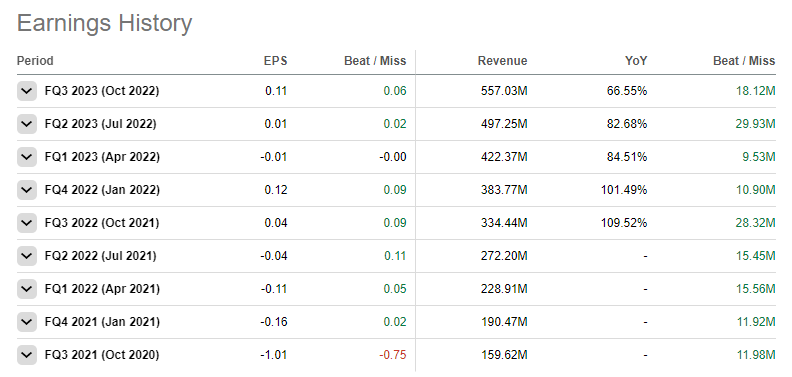

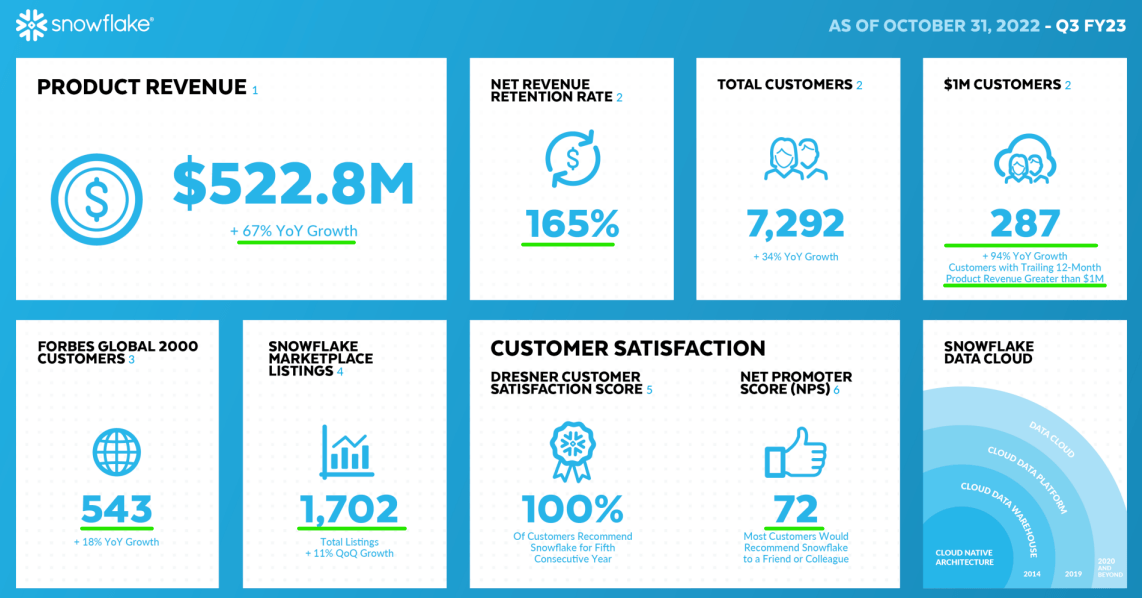

Unlike most other cloud software companies, Snowflake's business showed little impact due to the current macro environment in Q3, with SNOW beating on both the top and bottom lines. For Q3, Snowflake reported quarterly revenues and non-GAAP EPS of $557M (~66.5% y/y growth) and $0.11, respectively.

Snowflake Q3 ER Presentation

Of total revenues, Product revenue made up $522.8M, with professional services making up the rest. In Q3, Snowflake continued winning large enterprise customers at a healthy clip whilst generating massive growth from within its existing customer base [NRR of +165%].

Now, Snowflake's management highlighted weakness among its SMB customer base during the Q3 earnings call. However, SMBs make up less than 10% of total revenues, and having little exposure to them is playing in Snowflake's favor in this challenging business environment. Furthermore, nearly 95% of Snowflake's revenue is invoiced in US dollars (80% of revenue is generated in the US), which has shielded Snowflake's business from currency fluctuations.

While Snowflake remains unprofitable on a GAAP basis, it is turning into a free cash flow generating machine, with adj. FCF margin reaching +12% in Q3. For 2023, Snowflake expects adj. FCF margin to expand to +23%, and I like how Snowflake is delivering operating leverage whilst growing rapidly at scale.

Is SNOW Expected To Beat Earnings?

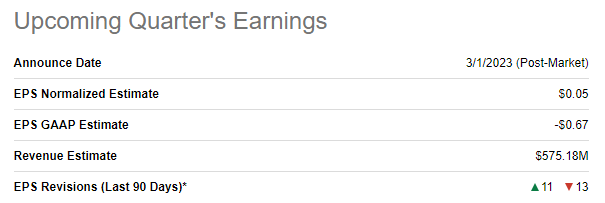

As we noted earlier, Snowflake's earnings date is 1st March 2023, with numbers expected to be released in post-market hours. According to consensus analyst estimates, Snowflake is set to deliver total revenue of $575.2M for Q4, and the range of these estimates is from $550M to $600M.

SeekingAlpha

Now, if we assume that Snowflake's Professional Services revenue will grow in line with its recent trend of $2-3M per quarter, then this revenue should come in at ~$36-37M. In this scenario, SNOW's Product revenue for Q4 would land at $538-539M, which is within management's guided range of $535-540M for Product revenues. Hence, the consensus analyst estimates are not baking in an earnings beat for Snowflake in Q4!

Over the last three months, Snowflake has seen 32 down revisions on revenue from analysts with zero up revisions. Clearly, analysts are not feeling very confident about Snowflake's top-line numbers going into Wednesday's report. And I think this pessimism is down to the growth deceleration we have seen in recent quarterly reports from cloud hyperscalers such as AWS (AMZN) and Azure (MSFT).

SeekingAlpha

SeekingAlpha

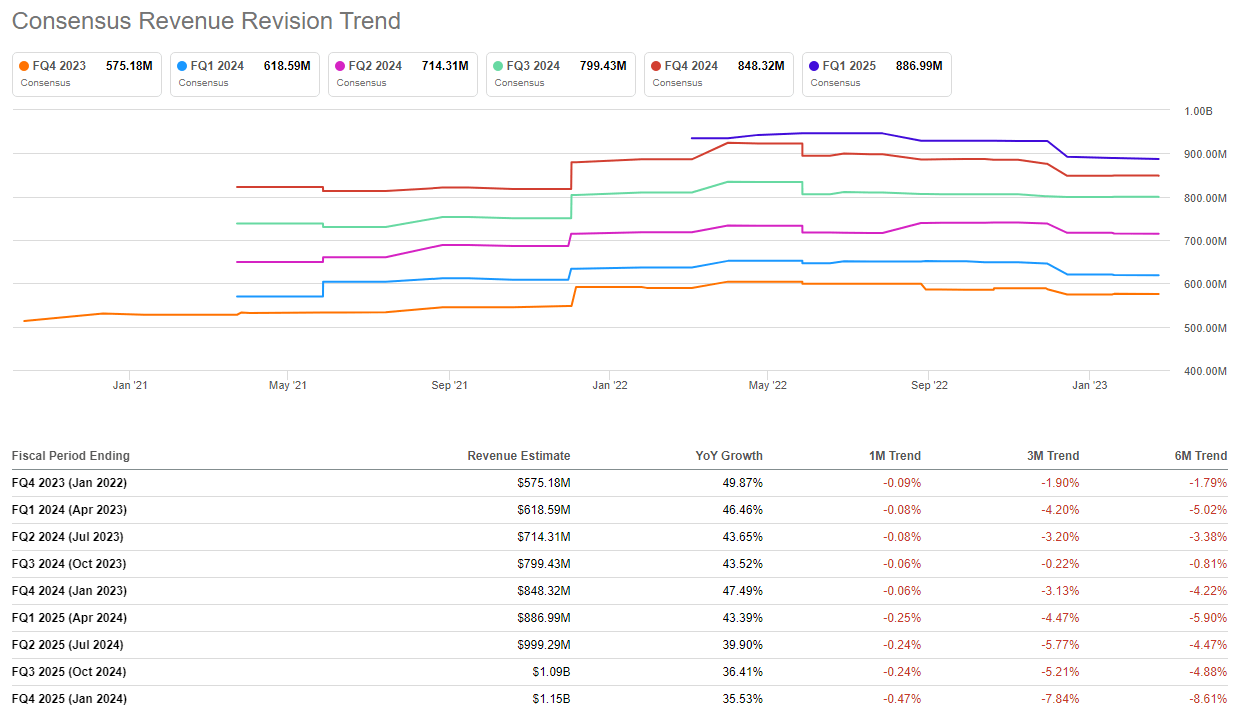

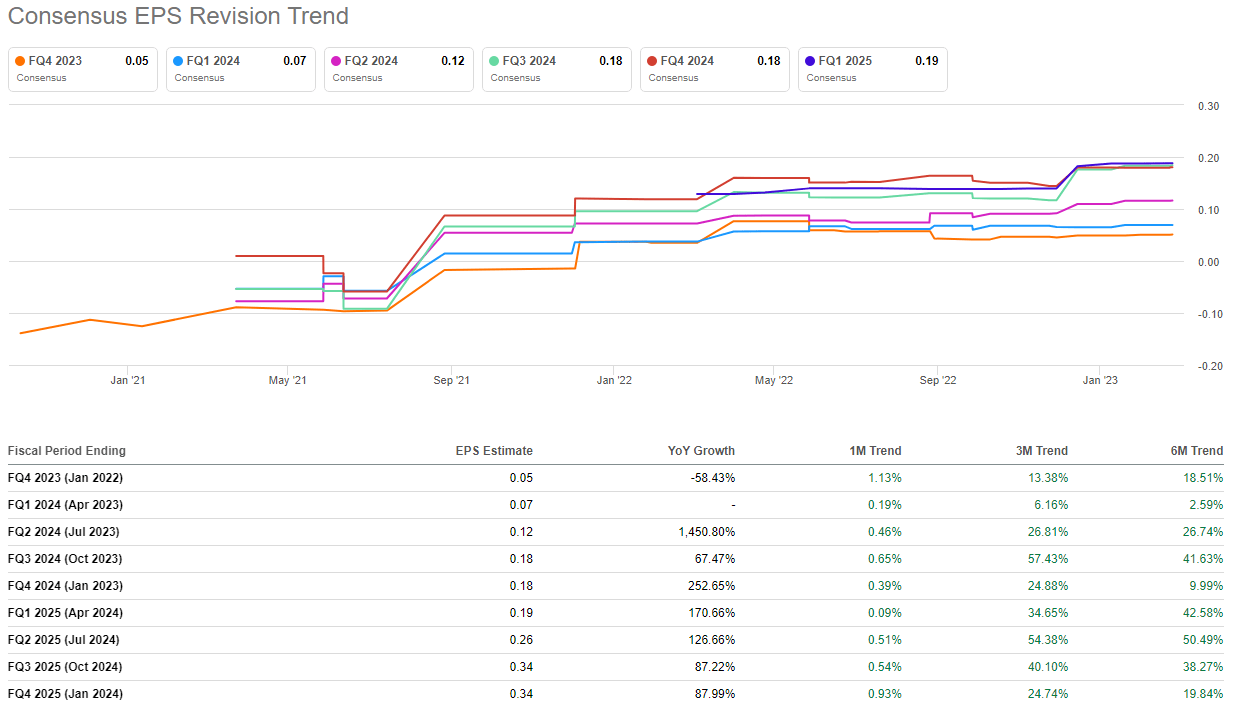

While the consensus outlook for Snowflake's revenue is trending in the wrong direction, we have a completely different story in development for earnings. With Snowflake's management focused on optimizing for free cash flows while driving rapid growth, the earnings outlook for SNOW is getting brighter:

SeekingAlpha

Based on recent business trends and management's guidance, I think Snowflake can beat the odds, and record a solid quarter in Q4, with Product revenues reaching $550-565M (vs. guidance of $535-540M, i.e., a beat of $15-30M). And this is what I have baked into my valuation model for SNOW.

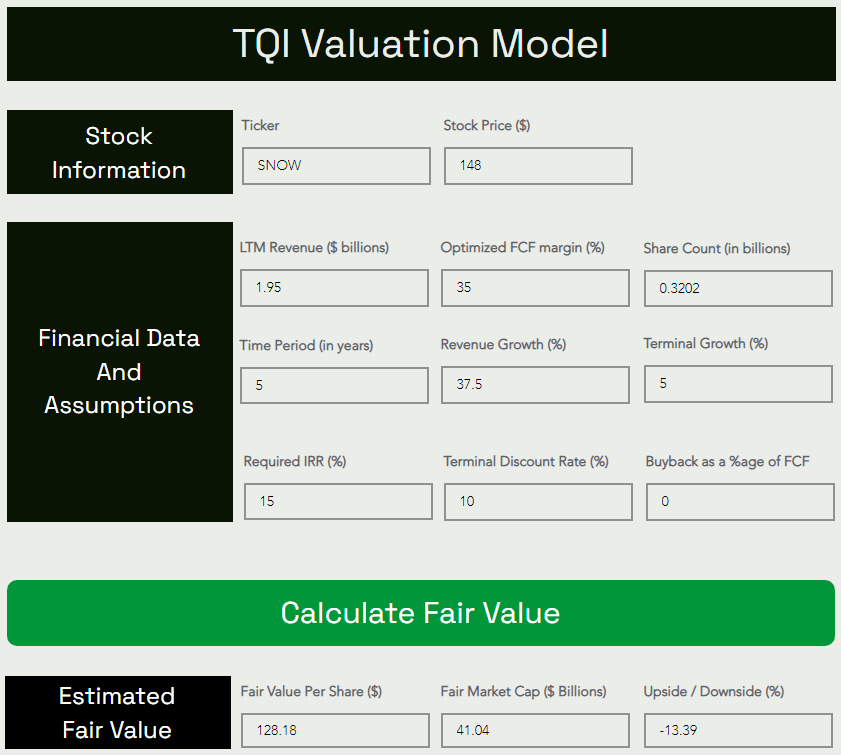

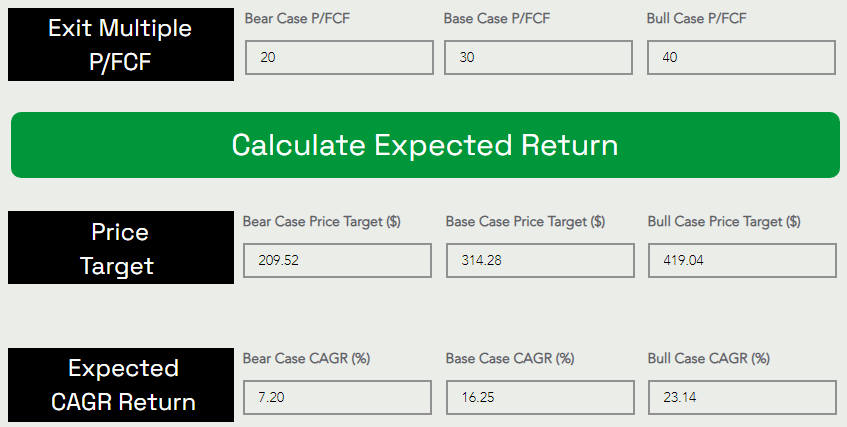

Snowflake's Fair Value And Expected Returns

TQI Valuation Model (TQIG.org)

TQI Valuation Model (TQIG.org)

Despite using somewhat aggressive (but achievable) assumptions for Snowflake (optimized FCF margin: 35% and 5-yr CAGR revenue growth: 37.5%), the stock looks slightly overvalued at current levels. While the expected CAGR returns of 16.25% are healthy, I strongly prefer staggered accumulation in SNOW due to its rich valuation and lukewarm technical setup.

Bottom Line

Here's what I wrote in conclusion to my post-earnings evaluation of Snowflake's Q3 report:

Given a poor macroeconomic backdrop, equities [especially the long-duration, richly valued ones like Snowflake (~85x P/FCF)] could remain under pressure in 2023. More than 90% of Snowflake's revenues come from large enterprises, and most of its revenues are committed and billed before consumption. Hence, I am not too concerned about Snowflake's usage-based business model failing in a recession. That said, SNOW's stock is unlikely to be immune to the broad market conditions, and hence, we could very well see weakness persisting in this counter for the foreseeable future.

From a technical perspective, Snowflake's stock is not inspiring at all despite its recent +20% jump. If we do see a decisive breakdown of the $100-$120 range, I would expect Snowflake to correct much further. This is why I suggest slow accumulation at these prices. However, a long-term investment does make sense here due to strong fundamentals and a reasonable valuation [SNOW is not a cheap stock]. As Warren Buffett said, "I would rather buy a great company at a fair price than a fair company at a great price". Overall, I like the idea of accumulating shares in Snowflake for a 5+ years investment at ~$145 per share using a DCA plan to perform staggered buying over 6-12 months.

Going into SNOW's quarterly report, I continue to like it as a long-term investment; however, investors should look to stagger their purchases over 6-12 months. Using a DCA plan would eliminate all the pre-earnings guesswork as to how the stock would perform after the report. That said, I am excited to see how Snowflake fares in this challenging market environment as such periods tend to separate the wheat from the chaff.

Key Takeaway: I rate Snowflake a "Buy" at $145, with a strong preference for staggered accumulation.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

Are you looking to upgrade your investing operations?

Your investing journey is unique, and so are your investment goals and risk tolerance levels. This is precisely why we designed our marketplace service - "The Quantamental Investor" - to help you build a robust investing operation that can fulfill (and exceed) your long-term financial goals.

We have recently reduced our subscription prices to make our community more accessible. TQI's annual membership now costs only $480 (or $50 per month). New users can also avail of special introductory pricing!

We make investing in equity markets simple, fun, and profitable

I am the Author and Chief Financial Engineer at "The Quantamental Investor" - a community pursuing bold, active investing with proactive risk management. At TQI, our mission is to help retail investors build generational wealth in equity markets. To do so, we share robust model portfolios that cater to investor needs across different stages of the investor lifecycle. All of our investment ideas are thoroughly vetted through TQI's Quantamental Analysis process, which uses a mix of fundamental, quantitative, technical, and valuation analysis. If you're interested in learning more about our marketplace service, visit: The Quantamental Investor

Prior to joining The Quantamental Investment Group LLC, I served as the Head of Equity Research at LASI's SA Marketplace service - Beating The Market, for two years. In the past, I have worked as an Associate Fellow with Jacmel Growth Partners, a middle-market private equity firm in New York. My resume also includes a stint at Capgemini as a software engineer. With regards to academia, I hold a Master of Quantitative Finance degree from Rutgers Business School and a Bachelor of Technology degree in Electronics and Communication Engineering, whilst I am also pursuing the CFA certification (Level 2 candidate).

If you would like to connect with me, please feel free to send me a direct message on SA or leave a comment on one of my articles!

Disclosure:I/we have a beneficial long position in the shares of SNOW, AMZN either through stock ownership, options, or other derivatives.I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Recommended For You

Comments

To ensure this doesn’t happen in the future, please enable Javascript and cookies in your browser.