DaVita: Earnings Top Lowered Expectations, Labor Costs A Concern, Cautious Chart

Summary

- The Healthcare sector has endured a very nasty stretch after posting impressive 2022 relative returns.

- DaVita reported better-than-expected earnings but that came after the bar was lowered.

- With a reasonable valuation, there are growth challenges this year while the chart remains lackluster.

Brett_Hondow

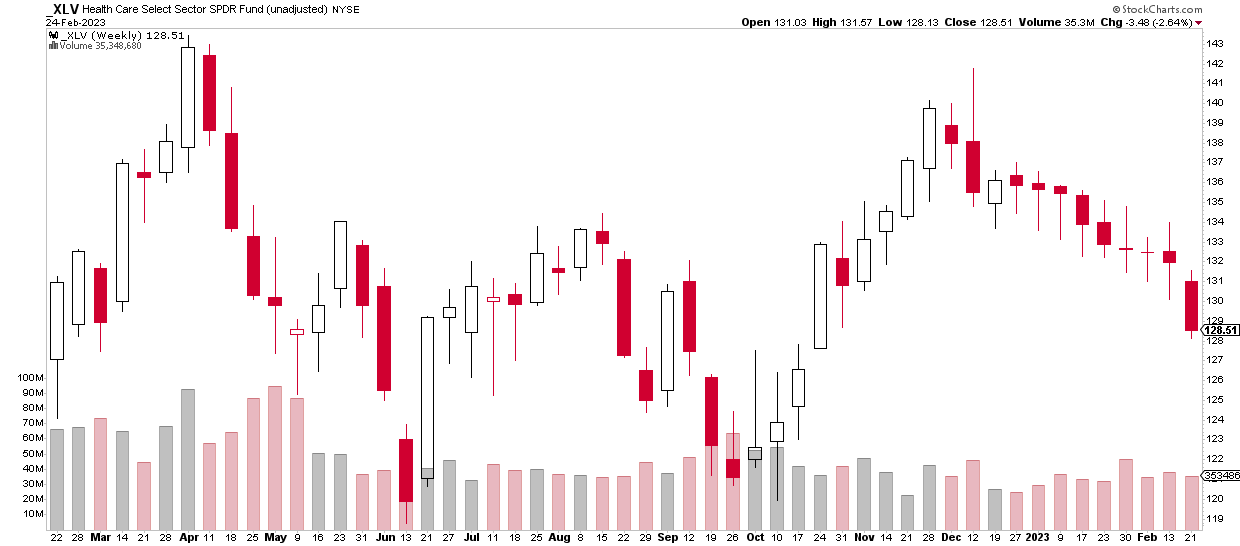

The Healthcare sector has been a major spot of recent relative weakness. The generally defensive niche of the S&P 500 is down a whopping 9 weeks in a row as the long-duration tech trade has held firm while other more strictly value sectors, like Financials and Industrials, have actually managed to hang on to some relative strength built in 2022.

DaVita (NYSE:DVA) is a healthcare services provider that features a weak growth outlook this year despite boasting ample free cash flow. I see the stock as a value play, but the technicals need to improve.

Healthcare: Down 9 Straight Weeks

BofA Global Research

According to Bank of America Global Research, DaVita Inc. is a leading dialysis provider in the United States. The company operates over 2,700 outpatient clinics in the US and serves over 200,000 patients. DaVita also operates in countries outside of the US.

The Denver-based $7.4 billion market cap Healthcare Providers & Services industry company within the Healthcare sector trades at a near-market 14.6 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend, according to The Wall Street Journal.

DaVita beat updated earnings estimate figures in its Q4 report and raised its 2023 operating income guidance. The lower hurdle was not enough to sustain a rally in the stock though. What might have been troubling to investors was a free cash flow guidance figure that was below consensus. Encouraging, though, was a beat on fourth-quarter margins due to better labor costs. At the same time, 2023 labor costs could be a significant headwind for the firm.

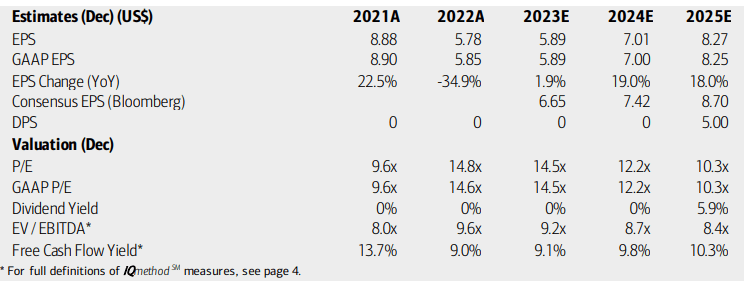

On valuation, analysts at BofA see earnings rising just modestly this year after a steep 2022 fall. Next year’s per-share profits as well as those in 2025 are seen as growing at a more robust pace. Still, the longer-term earnings growth trajectory is seen in the mid to high single digits. The Bloomberg consensus forecast is a bit more upbeat compared to what BofA sees.

Both DaVita’s operating and GAAP earnings multiples are seen as improving, so there’s a value case here. The EV/EBITDA multiple and free cash flow yield are both respectable. Overall, I continue to like the valuation.

DaVita: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

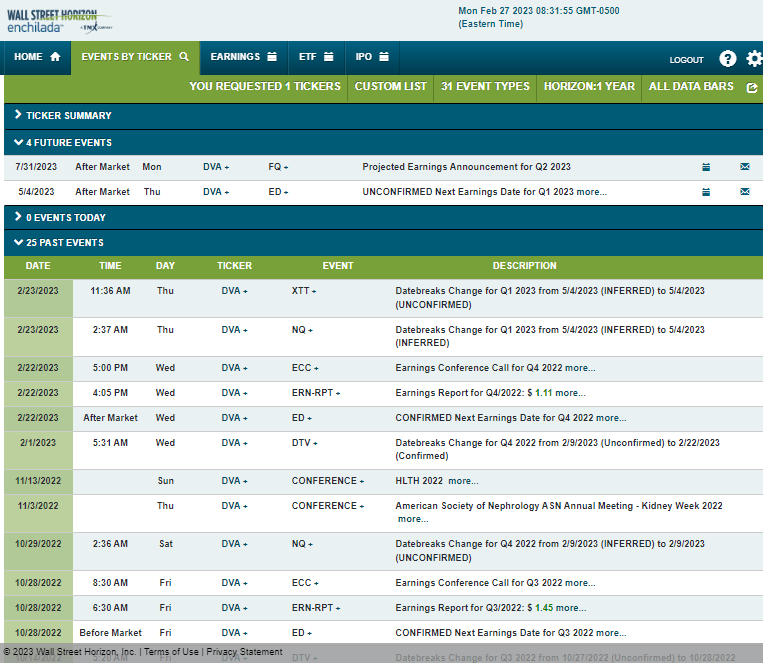

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q1 2023 earnings date of Thursday, May 4 AMC. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

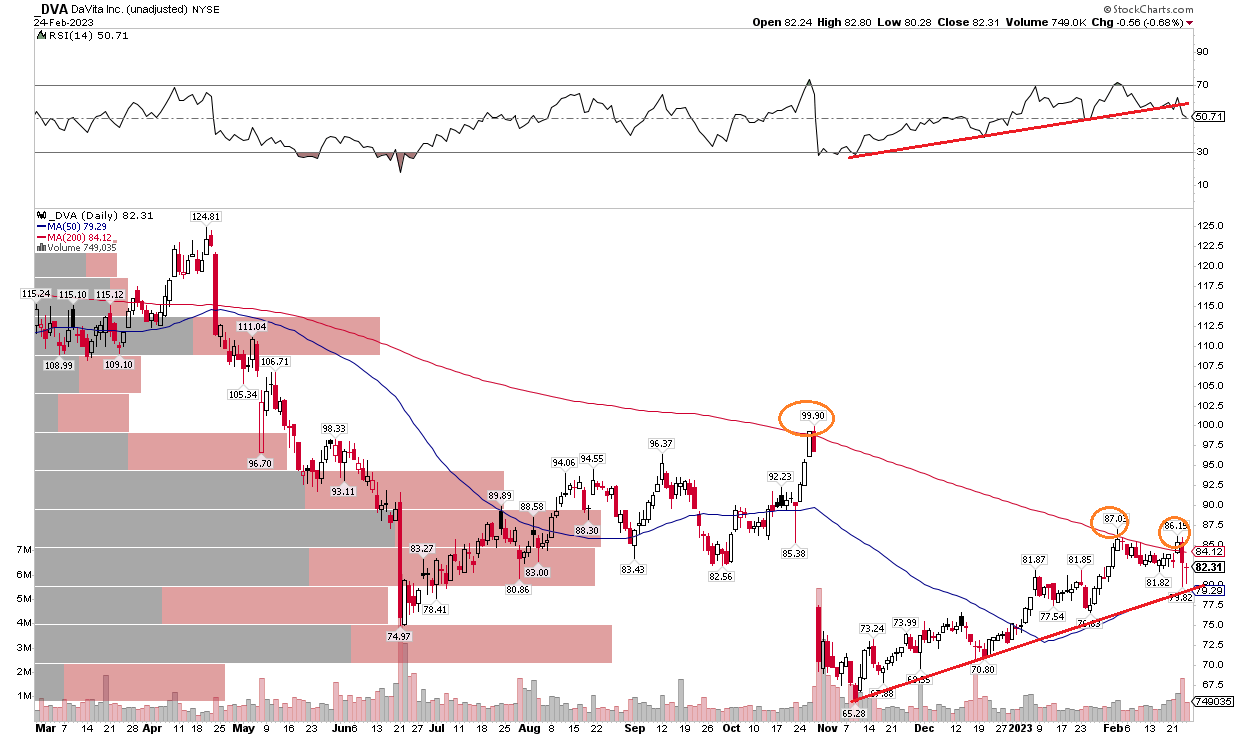

DVA has recovered nicely off its November low, but shares have still not managed to rally above the falling 200-day moving average. What I also notice in the chart below that is a concern for the bulls - the stock’s RSI momentum has modestly broken its uptrend since late last year. It's thought that momentum often turns before price, so this could be a bearish signal. Also, there was a slight uptick in volume late last week on the rejection of a rally try above the 200-day.

I would like to see the stock climb above the 200-day to help confirm a trend change – notice that DVA failed at that spot in October and now twice in February. There is some support in the $75 to $77 range and at the November low near $65. Overall, the burden of proof is on the bulls to break the long-term trend despite the rise in the last handful of months.

DVA: Concerning RSI Trends

Stockcharts.com

The Bottom Line

I remain a hold on DaVita. The valuation is fine, but there is a persistent downtrend that has yet to show definitive signs of breaking.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.