Expensify: Watch The Stock-Based Comp

Summary

- Expensify posted a solid quarter for Q4 2022, albeit missing consensus on revenues.

- The firm was able to generate positive cash from operations as well as $6M in free cash flow.

- However, this didn't filter into net income due to the company's ongoing & significant stock-based compensation program.

- This stock will become much more interesting once that program concludes. At the same time, however, revenue growth has stalled.

- This results in an inflection point with two countervailing forces and an unclear immediate future for the valuation of the stock.

Prostock-Studio/iStock via Getty Images

Overview

Expensify (NASDAQ:EXFY) is an expense management technology company. The centerpiece of their offering is a combination of expense card (Expensify Card) along with an application that lets users take pictures of receipts, which are then automatically processed using the firm’s technology. The company has since diversified their offering to cover a broad gamut of expense accounting needs for businesses.

Expensify.com 2.24.23

The company has a two-sided value proposition in that it offers services to both businesses as well as consumers. However, it only monetizes the business side of the equation through their SaaS platform. This generates revenue on a per-user basis and is primarily targeted at small and middle-market businesses. Their technology allows for ready integration into company accounting and payroll systems while also providing an easy-to-use reporting interface.

Expensify.com 2.24.23

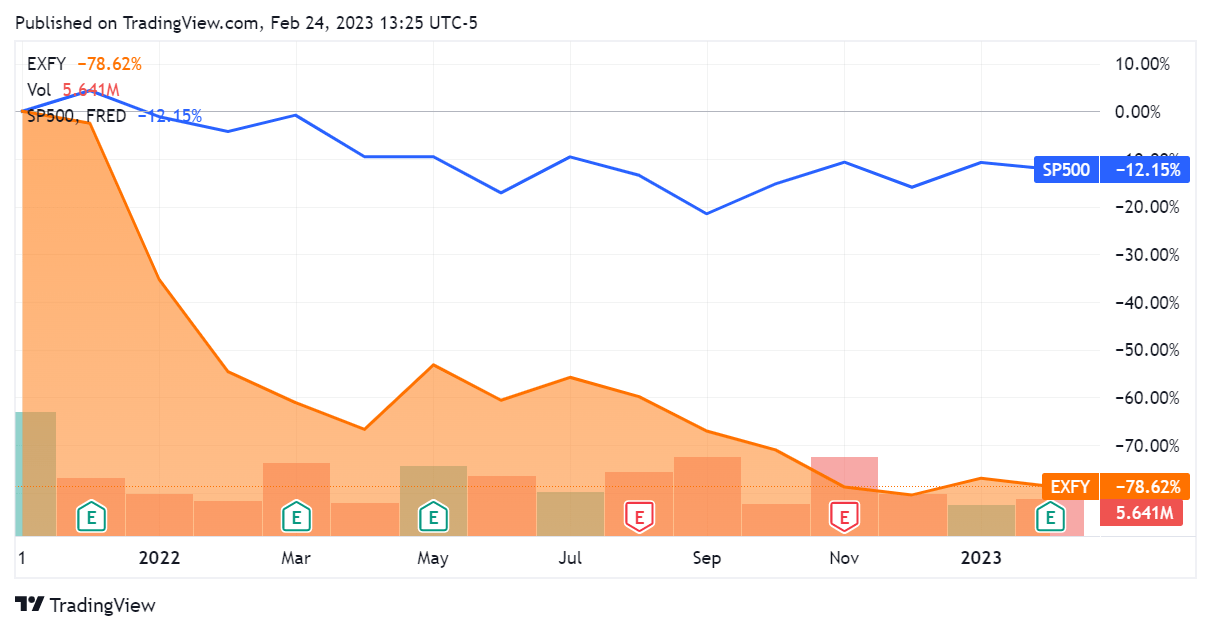

Founded in 2008, Expensify has grown significantly since then and first listed itself publicly in Q4 2021 at $27 per share. The stock has depreciated significantly since then while also trailing the S&P500 Index by a factor of 6.47x.

SeekingAlpha.com EXFY 2.24.23

This article will review Expensify’s financial statements as well as its present valuation in order to determine if it may be a quality investment at this time.

Financials

Revenues have grown significantly over the last 10 quarters, and the firm has put up a healthy double-digit growth rate throughout most of this period. Nonetheless, the results for the last two quarters saw the weakest levels of growth yet, and Q4 2022 saw the firm’s YoY sales growth slip into the single digits for the first time. This is of course a bad sign for a growing technology entity, although it isn’t enough of a trendline for us to conclude whether it may be a new normal as of just yet. The previous quarter constituted a revenue miss against consensus of $881.5K, something that wasn’t specifically addressed by management during the earnings call for that period.

SeekingAlpha.com EXFY 2.24.23 SeekingAlpha.com EXFY 2.24.23

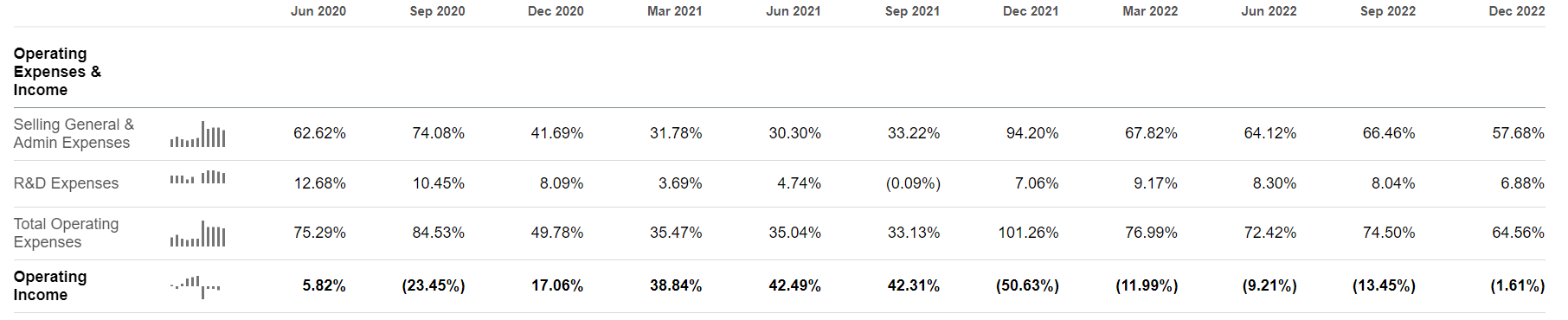

Looking over at its operating performance, we see that Expensify appeared to swing into an operating loss during the quarter of its IPO. This has unfortunately persisted since then.

SeekingAlpha.com EXFY 2.24.23 SeekingAlpha.com EXFY 2.24.23

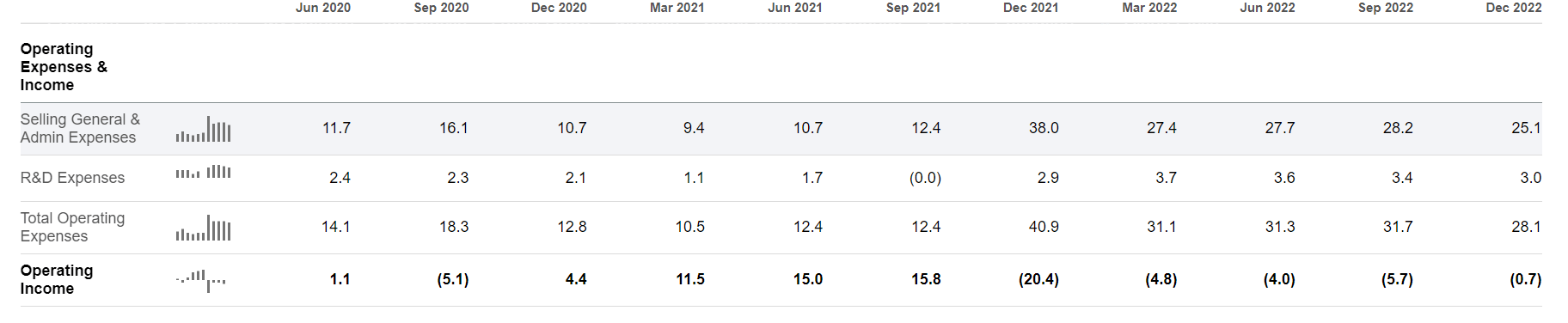

Operating expenses have been fairly significant throughout, with the firm’s expense structure peaking during its IPO quarter and dwindling down somewhat since then; some cost cutting in the previous quarter brought it to a more reasonable figure and reduced the size of the operating loss.

Due to the intricacies of the company’s operating cycle, it is actually able to generate cash from its operations ahead of operating income. This is due to the company acting as a custodian for cash that flows through its Expensify card, and certainly acts as a boon for the business as well as its capacity to operate in a capital-efficient fashion.

SeekingAlpha.com EXFY 2.24.23

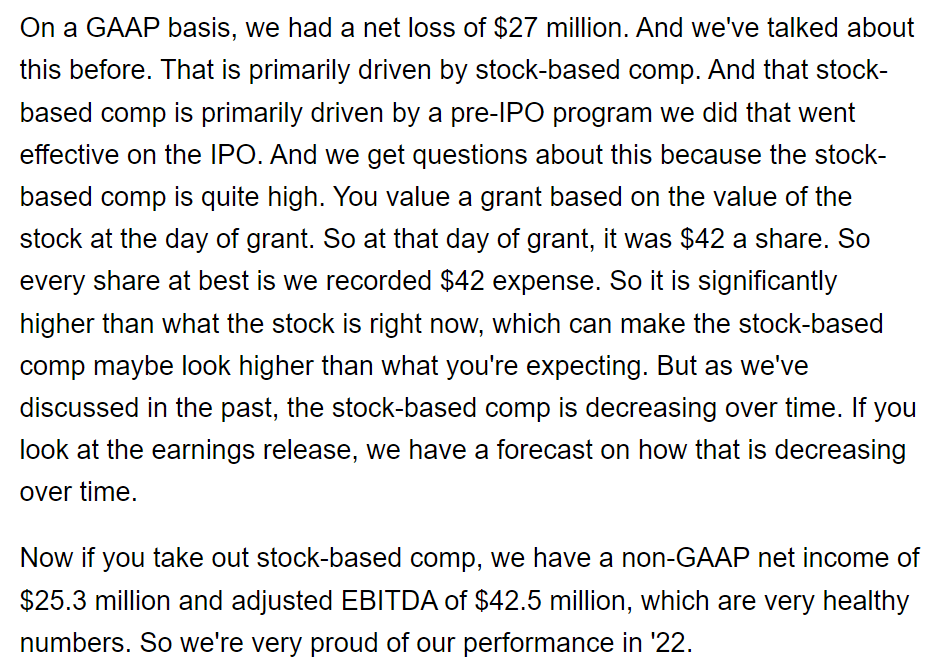

According to the earnings call transcript, this operating performance actually filtered into a free cash flow figure of $6M. The 2022 free cash flow figure came in at $26M – a decent showing in light of the other metrics.

SeekingAlpha.com EXFY Q4 2022 Earnings Transcript 2.24.23

Nonetheless, net income has been negative for some time. The nuance here is that this company is technically profitable prior to its share-based compensation program, which requires that the expense be deducted against net income in the quarter that it is issued. As such, the cash and operating figures are much more telling of the business performance overall: this business is more successful than it looks.

SeekingAlpha.com EXFY 2.24.23

Stock-based compensation is particularly significant for this company, generally hovering around 25-30% of its overall revenues.

SeekingAlpha.com EXFY 2.24.23 SeekingAlpha.com EXFY Q4 2022 Earnings Transcript 2.24.23

The company’s stock-based compensation program is, as mentioned, one that they have been running since the IPO and is based on the price that the shares hit that day. This masks what is actually a relatively well-performing business, although we must look at non-GAAP metrics in order to see this clearly. The cash flows and non-GAAP net income look solid in light of these adjustments.

Valuation

Looking at this company through its non-GAAP earnings multiple, we see that it is still trading at a premium relative to the information technology sector as a whole. This isn’t an overly significant premium, and I’m not certain that the market is pricing this company for what it’s adjusted performance as of just yet. Ultimately, it is generating both profits and cash flows when we look at it properly. However, the material slowdown in revenue growth over the last two quarters serve to give me pause.

SeekingAlpha.com EXFY 2.24.23

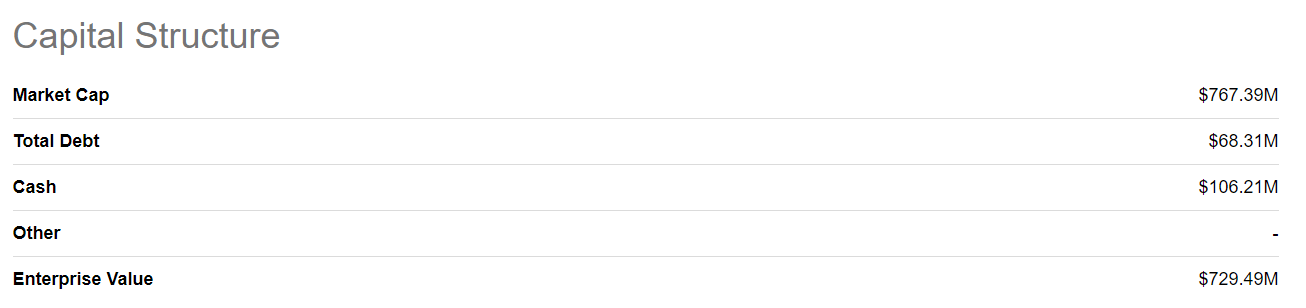

One notable highlight in its capital structure is that the company is holding 13.8% of its overall market capitalization in cash – certainly this places it above average. If it means anything it is that the firm is relatively well-capitalized for its size. Looking at this valuation in the context of the market, I would say it is mildly optimistic yet cautious - which is correct, in my view.

SeekingAlpha.com EXFY 2.24.23

Conclusion

Expensify is at an interesting inflection point. The company’s stock-based compensation program is masking what are solid and improving fundamentals, although it is also a significant dilutive consideration for investors. The firm is taking steps to counteract this through share buybacks. However, if revenue growth stalls, the conclusion of the share-based compensation program would make it such that the stock is still trading at a relative premium – or just about right at its current price. It isn’t clear which effect will be more quantitatively significant going forward, and as such I would rate this company a hold until we get a clearer view into the progression of these counteracting metrics.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.