Jazz Pharmaceuticals: Challenges To Repricing

Summary

- Jazz Pharma has been unable to catch a bid into the new-year rally.

- Despite recent advancements, it faces additional patent challenges to its core cash producing assets.

- Valuations are compressed, but we've seen no valuation upside over 5-year averages.

- Net-net, rate hold.

naphtalina/iStock via Getty Images

Investment Summary

Shares of Jazz Pharmaceuticals plc (NASDAQ:JAZZ) have traded within a range over the past 2-years to date. Looking to the current 12-month period, the story is much the same. The company has been forced to overcome a number of hurdles within this timespan, most significantly with patent disputes on a couple of its core drug segments, and recently. Still, JAZZ continues advancing its pipeline assets and recent developments in its zanidatamab collaboration with Zymeworks (NASDAQ:ZYME) are an encouraging feature within the investment debate.

There's no denying JAZZ is a long-term cash compounder that presents with robust fundamentals. A thorough analysis of this exhibits that the company is a defensive position within any equity investor's portfolio. However, for those seeking growth opportunities within this space, there may be more selective opportunities elsewhere. In this deep dive, I'll run through the moving parts in the JAZZ investment debate, paying close attention to the patent challenges that investors have discounted into its stock price. Net-net, rate hold.

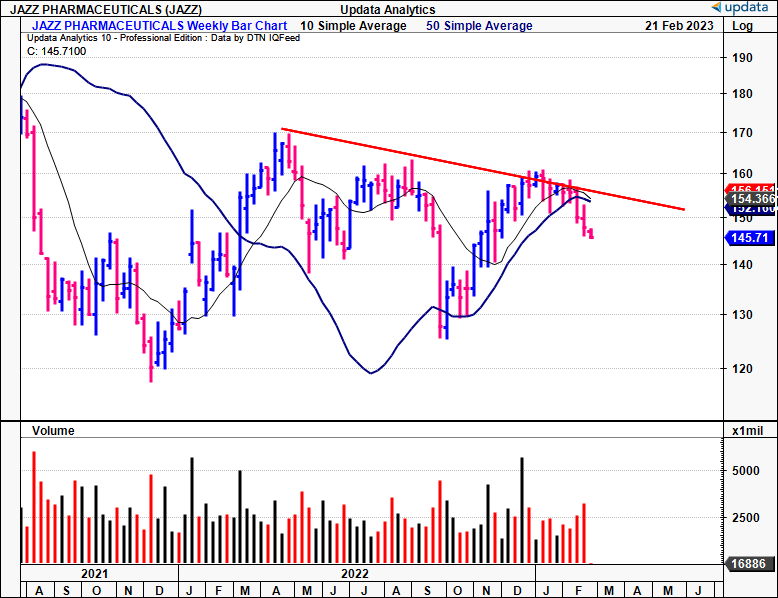

Fig. (1)

Note: Log scale (Data: Updata)

Challenges to the buy thesis

Investors take note of headwinds to drug development and sales within the biotech and pharmaceuticals sphere. We saw evidence of this back in September FY22’ when a Delaware court ordered JAZZ to delist its patent on its Xyrem label, from the FDA’s Approved Drug products With Therapeutic Equivalence Evaluations [colloquially known as the ‘Orange Book’ in the world of drug patents]. For reference, Xyrem is indicated in the treatment of narcolepsy, a rare disorder that impacts the sleep-wake cycle. The decision came after JAZZZ had filed motions back in May of FY21’ against Avadel Pharmaceuticals (AVDL) claiming it had infringed upon 5 patents pertaining to Xyrem, via its Lumryz label. The quandary started when JAZZ alleged AVDL had utilized the same active ingredient in its formulation, known as sodium oxybate. Except, Lumryz is a once-daily oral administration, whereas Xyrem, contributing $1.7Bn in sales for JAZZ in FY20’, is a bi-daily solution. Alas, the Court’s upheld decision is a remarkable factor that must be factored into the JAZZ investment debate. We’ve covered this extensively in our last coverage on AVDL [see: here]. For a deep dive on the comparison between the two competing names, see Seeking Alpha author Out of Ignorance’s coverage on the same – this in-depth take on the situation, appropriately labels it the “Oxybate Wars”. I encourage you to read both analyses for the best investment reasoning possible.

Extending from this, JAZZ has pushed forward ahead of the debacle by rolling patients from Xyrem onto its Xywav label. Xywav is potentially more of a mid to long-term growth lever for JAZZ in our opinion, seeing as is has a dual indication in both narcolepsy and idiopathic hypersomnia (“IH”). As a key differentiator, it is the only oxybate approved for both narcolepsy and IH. In that vein, the strategy looks to be rolling patients off Xyrem, onto Xywav, in order to drive sales across both conditions. For example, in its Q3 FY22’ earnings, it reported 9,500 patients on Xywav, with ~85% of these attributed to narcolepsy, the remainder for IH. Per JAZZ President Dan Swisher’s comments on the last earnings call: “We expect that Xywav will be the oxybate of choice in 2023, even as authorized generics enter the market and as branded competition potentially becomes available…We have confidence that Xywav is a durable product that will continue to contribute meaningfully to Jazz's commercial portfolio”. Consequently, the move away from Xyrem could prove to be a smart move to drive top-line sales for JAZZ by estimation, especially now that it is competing on-top of AVDL’s Lumyrz label with the dual indication, and thus not directly against it.

Extending from the above, JAZZ also filed patent infringement suits against 13 competing biotech and pharmaceuticals companies to develop a generic version of the company’s cannabidiol oral solution, Epidolex. For reader reference, Epidiolex is a phytocannabinoid-based pharmaceutical drug indicated for the treatment of 2 rare and severe forms of epilepsy: 1) Lennox-Gastaut syndrome, and 2) Dravet syndrome. It is administered as an oral solution bidaily and is known to act by modulating the endocannabinoid system, resulting in increased levels of certain neurotransmitters in the brain, thus leading to a reduction in seizure frequency. Specifically, the mechanism of action of Epidiolex involves the inhibition of an enzyme known as fatty acid amide hydrolase (“FAAH”). This enzyme is responsible for the degradation of the endocannabinoid anandamide, itself known to play a role in the regulation of neuronal excitability. Hence, by inhibiting FAAH, Epidiolex is thought to increase the levels of anandamide in the brain, thus reducing the frequency of seizures. It’s worth noting that JAZZ’s patents are related to the composition and method of use for Epidiolex. The company’s in question are challenging JAZZ’s patent claim under a paragraph IV certification, meaning they allege this protection on Epidolex is “invalid, unenforceable, and/or will not be infringed by the manufacture, use or sale of the generic product”. As a favourable outcome for JAZZ, resultant from the lawsuit, the FDA will impose a 30-month stay of approval against the company’s filing for the generic applicant. We’d also point out that Epidiolex has orphan drug exclusivity for treating the conditions listed above until FY25’.

JAZZ recent catalysts

The most recent positive catalyst that could potentially see JAZZ catch a bid is the positive readouts from its zanidatamab study, in collaboration with ZYME. The pair's open-label phase 2 study (NCT03929666) is ongoing, and is examining the combination of zanidatamab with chemotherapy as a first-line treatment for patients with advanced HER2-expressing metastatic gastroesophageal adenocarcinoma ("mGEA"). The study includes efficacy and tolerability data from 46 mGEA patients, who were not previously treated with HER2-targeted agents, or received previous systemic treatment. The methodology involved administration of zanidatamab, along with physician's choice of chemotherapy treatment, to patients across 15 sites in Canada, South Korea, and the U.S. Findings illustrated this combination is an effective treatment protocol as a first-line therapy of HER2-positive mGEA.

Looking at the results in greater detail, among 42 patients evaluated for overall survival ("OS") who the combination therapy [at the 95% confidence interval]:

- The 18-month OS rate was 84%

- The 12-month OS rate was 88%

- The median overall survival had not yet been reached (with 26.5 months median duration of study follow-up).

- Zanidatamab treatment resulted in a confirmed objective response rate ("ORR") of 79%. The disease control rate was 92%.

- Moreover, of the 38 response-evaluable patients, 3 achieved complete response.

- The median duration of response in this cohort was 20.4 months.

Subsequently, the pair continue to enroll patients in their phase 3 Herizon-GEA-01 study to push zanidatamab along the regulatory pathway, hopefully for an FDA approval.

JAZZ fair view of fundamentals

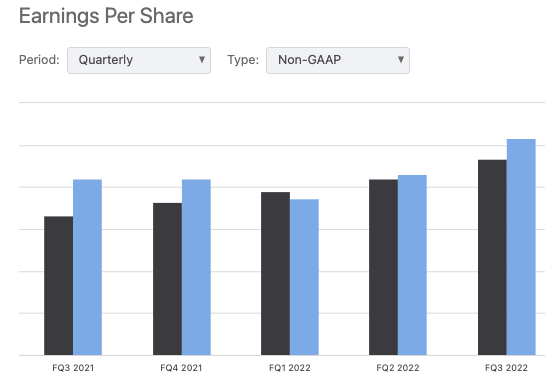

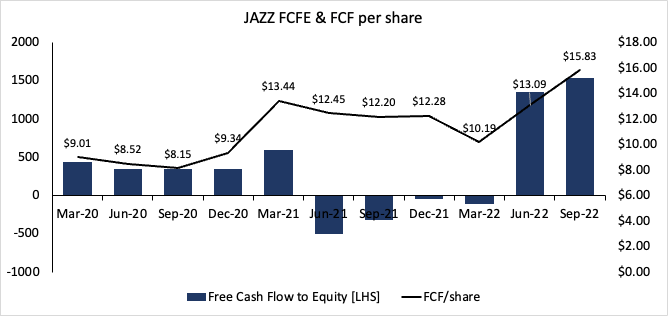

Balancing the investment debate, it's important to note that JAZZ has robust fundamentals that are well appreciated by the market. Moreover, with companies investing heavily into R&D its essential to examine the movement of cash flows over GAAP earnings, given that GAAP accounting requires companies to expense R&D on the income statement, versus recognizing it as in investment into future growth. On a rolling TTM basis, JAZZ has continued ratcheting up CFFO, booking $1.1Bn in Q3 FY22', up from $847mm in Q1 FY20'. More importantly to this analysis, it has continued driving free cash flows higher, realizing $1.5Bn in trailing FCFE in its last report, a growth of 250% over this same time period. Note, that its FCF per share has lifted to multi-year highs to $15.83 in the last print. This is more than $6 accretion in FCF/share since FY20', exhibiting the value it has created for shareholders. Adjusting for the R&D expense and other line-items to JAZZ's non-GAAP earnings, you'll see it has beaten estimates in 4/5 of the last quarters, winding up the earnings leverage as it goes. The company is also well capitalized to continue its growth route looking ahead as well. Looking at its credit summary, its short-term obligations are covered by liquid assets by 3.16x, whereas its TTM interest expense is covered more than 5x by trailing EBITDA.

Fig. (2)

Data: Seeking Alpha, JAZZ, see: "Earnings"

Profitability is also a standout, and the company is positioned well above the industry in trailing returns in capital at 6.4%, with an asset turnover of 0.3x. On its top-line sales growth, it has held a relatively constant gross margin in the 93–94% range, meaning it is a potential standout in the current high inflation environment. We'd note the majority of its expenditures are OpEx related, and related to the production of its various products. Henceforth, we believe JAZZ has potential to remain resilient in a market downturn with its high gross margin.

Fig. (3)

Data: Author, using data from JAZZ SEC Filings

Valuation

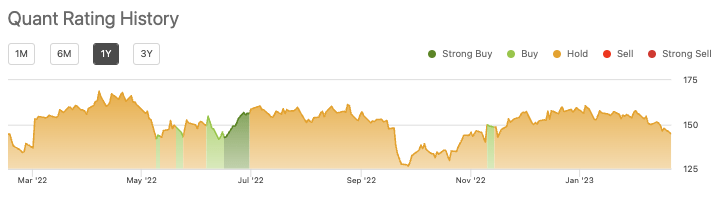

On face value, JAZZ is attractively priced at ~8.5x trailing earnings [non-GAAP] but this is balanced by the fact it trades at ~3x book value of equity. Nevertheless, valuations are an attractive feature in the JAZZ investment debate. It trades at a respective discount to industry peers across all multiples except the price to book value mentioned above. It also trades at a meaningful discount to its 5-year averages. However, this opens up an interesting channel of argument. JAZZ is certainly not the same company it was 5-years ago. In that vein, we'd expect some valuation upside from the company over this time, and this isn't the case. By the best estimation, this suggests that investors haven't rewarded its growth percentages listed above, especially the high growth in FCF's over the past 3-years. This is supported by the quant rating system, the rates JAZZ a hold based on a composite of factors, including valuation and profitability.

Fig. (4)

Data: Seeking Alpha, JAZZ, see: "Ratings"

Final remarks

JAZZ is a long-term cash compounder that has displayed exceptional free cash conversion over the last 3 years. A deeper look at its fundamentals illustrates that it has above-industry returns on capital, and robust gross margins to withstand any market downturn. Unfortunately, the market hasn't rewarded its stock on the back of this. Most notably, the company has faced challenges from patent protection over its key drug assets, something the market has priced into the JAZZ stock price quite distinctively. Consequently, the investment debate comes mostly down to investor preference. The stock is well justified as a defensive position in the equity risk budget. However, those searching for growth opportunities may find more selective names elsewhere within the pharmaceutical continuum. We are more aligned with the latter, and rate JAZZ a hold.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.