Silicom: Edge Solutions Serve A Growing Customer Base

Summary

- Silicom has posted 18 years of profitable results and has not missed quarterly guidance for the last 19 consecutive quarters.

- Silicom enters the new financial year with a record-high backlog, a strong sales pipeline and a growing demand from a broader range of potential customers.

- Cautious of management concerns about the economic slowdown and supply chain disruption leading to potential cancellations and order delays in 2023.

jamesteohart

As the world increasingly generates and consumes data 'on edge, ' companies with edge networking expertise and offerings, such as Silicom Ltd. (NASDAQ:SILC), are growing in importance. SILC has been securing back-to-back design wins across a broader customer base, recently chosen by a voice solution leader and an SD-WAN leader, entering the financial year with a record-high backlog and a strong pipeline of future design wins. Although the company is profitable with solid fundamentals, the stock price dropped after the Q4 earnings call, in which management raised concerns about growth being impacted by the global economic slowdown and supply chain disruptions in the form of high-order cancellations and delays.

One month stock trend (SeekingAlpha.com)

Whilst we should remain cautious of a performance slowdown, SILC has delivered record revenues and earnings and has a strong balance sheet and solutions that are increasingly crucial to a larger-than-expected consumer base. It is a small-cap stock with a market cap of $260.45 million that has grown through 200+ tailor-made design wins for over 400 customers across the globe, benefiting hugely from a long-term partnership with Intel (INTC). Therefore investors may want to take a long-term bullish stance on this stock.

Overview

SILC is a connectivity solution provider founded in 1987 and is headquartered in Israel. It produces many tailor-made and off-the-shelf network and data infrastructure solutions for cloud, 5G, telecom, mobile operator, service provider and on-premise environments. Customers ranging from telcos, services providers and OEMs are reaching out for solutions, from SDWAN and SASE to Enhanced-Internet and telco-dedicated routing. It has built a solid global reputation with over 200 customers and over 400 active design wins and is well-positioned to benefit from the fast-growing connectivity markets. It has a strategic partnership with Intel that continues to help SILC's growing customer base due to its product collaboration efforts.

Market leading customers (Investor Presentation 2023)

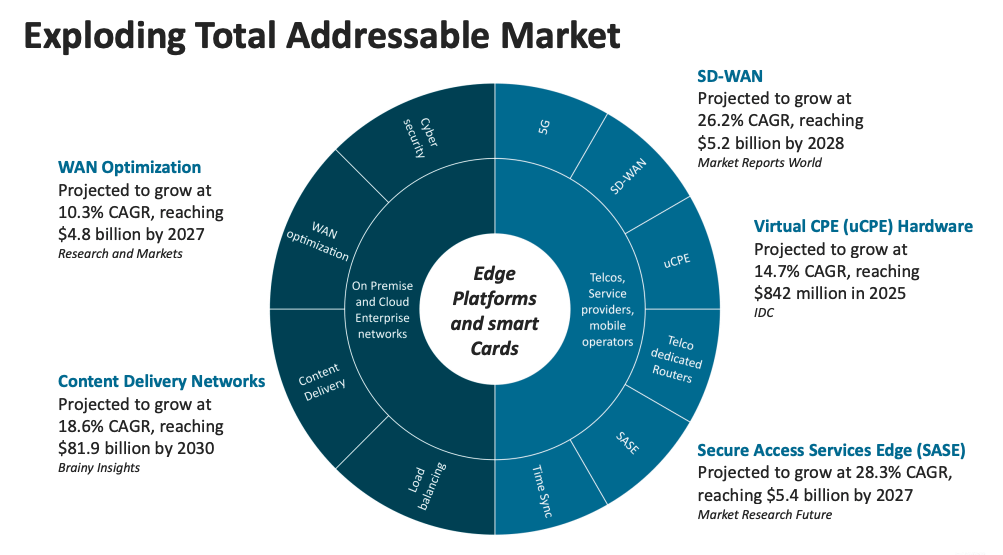

Growing total addressable market

Over the years, the company has diversified its offerings, lowering the cyclical nature associated with its product offering, increasing the variety of tailwinds and growing its TAM. The company sees a significant tailwind for its Smart Edge Platforms and Acceleration Cards as businesses seek to have computing, networking, and storage activities near the end user as possible.

TAM (Investor Presentation 2023)

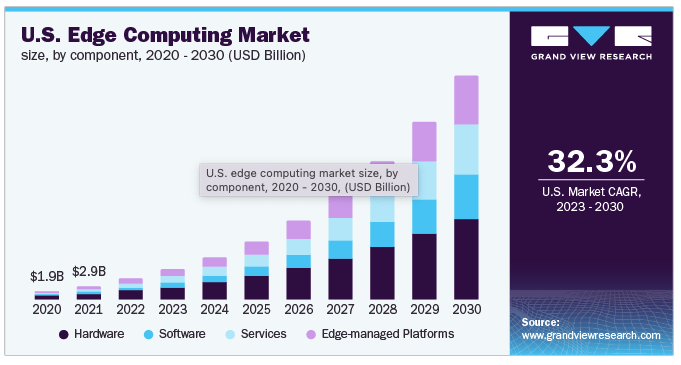

According to a recent study, the global edge computing market will reach $155.9 billion by 2030 at a CAGR of 37.9% from 2023.

Market growth (Grandviewresearch.com)

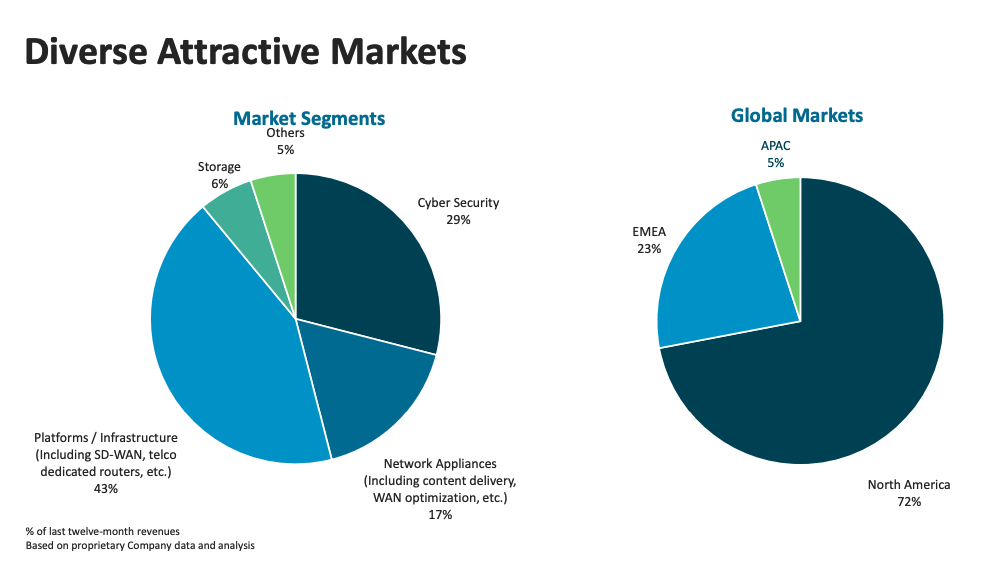

Below we can see an overview of its market segments and global market regions as represented in Q4 2022. The platforms /infrastructure segment accounted for 43% of total sales over the last 12 months. This includes SD-WAN, telco and dedicated routers. The edge products have been a significant growth driver, although initially targeting the SD-Wan market, the same products are relevant to a broader market.

Market segments (Investor Presentation 2023)

The company is diversifying its customer base through its ability to provide complete solutions compared to competitors who provide specific best-of-breed solutions. SILC recently announced a design win with a leading provider of enterprise voice solutions. The customer has placed a total order of $2.5 million. For the last 18 years, SILC has consistently reported profitable results, has not missed quarterly guidance for the last 19 consecutive quarters, has a strong balance sheet, and its SD-WAN/ Smart Edge platforms, 5G/O-RAN solutions, and server adapter products are in high demand.

Financial overview

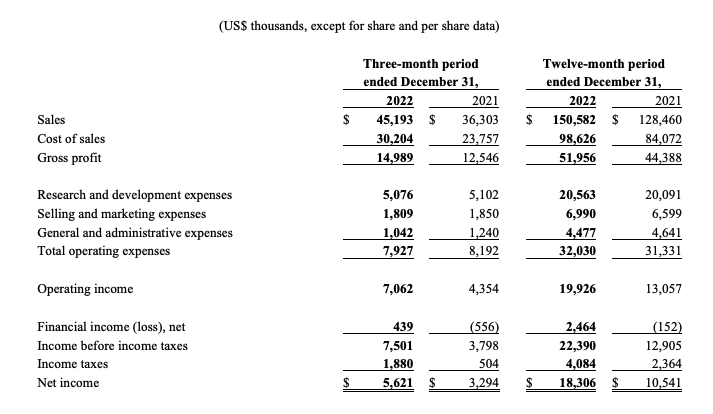

The company has just posted a robust set of Q4 and full-year results and enters the next financial year with a record-high backlog and a strong pipeline of future design wins. SILC has had a solid finish for its financial year 2022. Its full-year revenue for 2022 increased by 17% YoY to $150.6 million, and net income increased by 74% to $18.3 million (GAAP basis). For Q4 2022, quarterly revenue increased by 24% YoY to $45.2 million, and net income increased by 71% to $5.6 million. Backlog was at an all-time high time high, entering the first quarter.

Financial overview Q4 and FY22 (sec.gov)

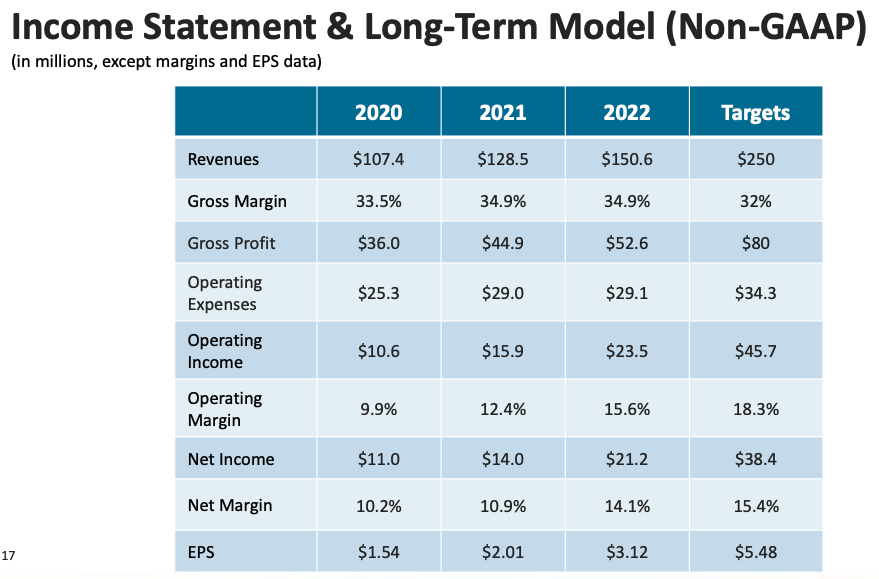

SILC has a strong balance sheet with zero debt, cash & cash equivalents of $49.9 million, working capital of $126.5 million, total assets of $216.2 million and stockholders’ equity of $179.3 million. If we look at liquidity, it has a current ratio of 5.67 and a quick ratio of 2.42. We can see in the chart below that revenues have been upward trending over the last three years, and it has impressive operating and net margins and 55% growth in its EPS.

Annual growth overview (Investor presentation 2023)

The company has initiated a Q1 2023 guidance which could fall under the consensus of $37.84 million. However, it would still be an increase of 17% YoY.

Final thoughts

While the company is delivering back-to-back design wins through its Edge Networking technologies and offering unique and in-demand solutions for an increasingly larger TAM, its stock price has dropped in value by 39% over the last five years. However, the drop in price does not take away that SILC has an increasingly important solution as more and more data is generated and consumed ‘locally’, driving demand for data processing capabilities at the edge. However, we should remain cautious of the impact of an economic slowdown, component shortages and continued supply chain challenges in the short term. The company has an upward-trending historical financial performance, is growing its customer base and is delivering ongoing wins due to its complete solution offering and the benefit of partnering with INTC. Therefore investors may want to take a bullish stance on this stock.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.