Magnachip Semiconductor: Given 2023 Recovery Story, Management Could Buy Back More Stock

Summary

- Magnachip Semiconductor Corporation went from a signed deal at $29 per share to everything falling apart.

- The business is struggling due to wafer shortages and inventory builds.

- Sales are expected to increase markedly in the second half and near the end of 2023.

- Management has a great opportunity given the low share price and an expected recovery in sales.

- The company has the cash firepower to take out a lot of shares and create shareholder value highly efficiently.

- Looking for more investing ideas like this one? Get them exclusively at Special Situation Report. Learn More »

PonyWang

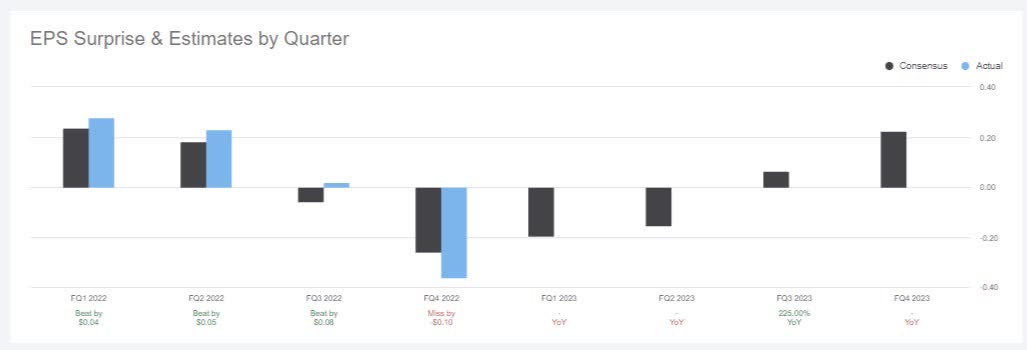

Magnachip Semiconductor (NYSE:MX) recently reported earnings, and they were a bit worse than expected. The market expected a negative print but the consensus was slightly higher. In addition, MX tends to beat expectations, and this time it went under. In the next two quarters, the company is expected to report negative earnings again with before recovering later in the year. I have no problems with the market's response to the earnings, especially with management failing to deliver on buybacks (in size).

Magnachip EPS estimates (Seeking Alpha)

MX basically has two lines of business: power and display. Management's story is that the display revenue is nonexistent because of wafer shortages for the OLED business. This caused the company to miss key product launch windows in the second half of 2022 and, with that a lot of volume. This business is also suffering from weak demand in China.

In the power business, management is claiming weakness because of consumer demand deteriorating, which leads to inventories building up at its customers.

On the last call (which I discussed here), management claimed that a display customer would likely complete qualification by the end of 2022. They guided towards production for new products to start end of Q1 2023. On this earnings call, the story remained consistent:

In our Display business, we successfully won a new Tier 1 panel customer outside of Korea, which marked the expansion of our OLED business into international markets. We are currently working with this customer on two OLED DDIC design projects and I am happy to report today that our first chip was successfully qualified by this customer in December and we will begin shipping towards the end of Q1 2023.

On the power solutions front, things aren't nearly as bad but guidance isn't exactly upbeat. Among other things, management said (emphasis mine):

For our Power Solutions business, we expect to maintain the momentum of design wins and premium tier product mix. However, it's important to note that our Power business is not immune to the broader economic downturn, which impacts consumer-related applications, and we expect the first half of 2023 to also be challenging. We believe that this will largely be due to macro factors rather than anything specific to fundamentals as the data points, I just highlighted are a testament to the competitiveness of our power products. Q1 is also typically our seasonally slowest quarter following holiday shipments and is impacted by slow activity around Chinese New Year. Looking forward, as channel inventories are consumed and the broader economy recovers, we expect to see a rebound in Power revenue.

On the previous to last call, management leaned more on China's shutdown (emphasis mine):

In addition, China COVID lockdowns and the dramatic slowdown in consumer spending as a result of global inflationary pressures reduced demand for smartphones, particularly in China, and resulted in an oversupply of channel inventories. This caused our large customer in Korea to significantly reduce orders to normalize inventory levels. Unfortunately, we believe these poor dynamics will continue in the near future, but we expect inventory levels will normalize by the middle of next year.

With China reopening, that's a bit more difficult to sell, and they're pivoting to talking more vaguely about macro challenges. This worries me slightly, although their previous guidance was for inventory levels to normalize by the middle of 2023. The company also started a voluntary resignation program which it expects to result in a 4%-5% reduction in the workforce. I have to give credit where it is due because CEO Young-Joon Kim took a voluntary salary reduction of 10% for 2023. I think this is good leadership, a great example for other employees, and a clear demonstration he understands shareholders are not satisfied with current performance.

The CEO has previously said that they're focused on what's in their control and to make improvements there while waiting for the macro to improve. One thing that's in management's control but where I think their actions are lacking is in buybacks. The company bought back $9 million in Q4. That's with a highly inefficient capital structure with no debt and $225 million in cash at year-end. True, this should get them through an extended downturn, but could there be other options to navigate a downturn should an even deeper one materialize? A credit facility or a set of bonds. Perhaps the company could do a creative green bond issuance tied to their power business, that's very important to renewable energy generation. I'm not a CFO, so I don't know the right answer, but I do know that the company has around $5 in net cash per share. Not long ago, private equity wanted to take this company private at ~$30 per share. If management and the board believe in their recovery story for end of 2023, the logical path to shareholder value creation is to hit the bid hard, execute on the $37 million outstanding buyback program and announce a 1-2 year $100 million program. With MX stock trading below $10 per share, $5 in cash and consensus earnings for 2024 of $0.65, I still think it is a strong buy. I expect the long-term trend for earnings and sales to increase while the company is valued as if it is on a permanent downward trajectory.

This article was written by

I gravitate towards special-situations. That means situations around companies or the market where the price can move in a certain direction based on a specific event or ongoing event. This eclectic and creative style of investing seems to suit my personality and interests most closely.

Since 2020 I host a podcast/videocast where I discuss (special-situation/event-driven) market events and investment ideas with top analysts, portfolio managers, hedge fund managers, experts, and other investment professionals. I highly recommend it (pick episodes around topics that interest you) for the amazing guests that come on with regularity.

I've been writing for Seeking Alpha since 2013 after playing p0ker professionally. In 2018 I founded Starshot Capital B.V. A Dutch AIF manager. Follow me on Twitter @Bramdehaas or email me Dehaas.Bram at Gmail

Disclosure: I/we have a beneficial long position in the shares of MX either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.