Upstart: Don't Fight The Sellers Here

Summary

- Upstart stressed the macro headwinds over the past year surpassed its "most wildly bearish expectations."

- Despite that, Upstart highlighted that its AI models had improved further.

- The Fed's record rate hikes have exposed a significant shortfall in third-party funding, a gap that has not gone unnoticed.

- Has Upstart finally turned the corner? Could the worst be behind the company?

- I do much more than just articles at Ultimate Growth Investing: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

Scott Heins

It's hard to find investors or analysts optimistic that Upstart Holdings, Inc. (NASDAQ:UPST) could recover from its malaise. Instead, a flawed funding model, a hawkish Fed, subprime borrowers, and reticent lenders have come together to inflict significant pain on the AI-powered consumer financial technology company.

It has been so bad that even management was taken aback, as CFO Sanjay Datta stressed recently:

Reflecting back over the past year and on our outlook of a year ago, it's safe to say that the macro has exceeded our most wildly bearish expectations. One year ago on our earnings call, we've begun to sound the alarm on encroaching consumer delinquencies and the potentially adverse impact of the disappearing government stimulus. At a time when the broader markets were still quite sanguine about the economy. (Upstart FQ4'22 earnings call)

Upstart bears have continued to point their fingers at its unsustainable funding model, which relies on "at-will" external funding. Moreover, the company's discussion with its funding partners on a more sustainable model predicated on "locked-in and secured volume" has yet to yield definitive results.

The company has also continued to take on risks onto its balance sheet (meant initially for R&D purposes), reaching $1.01B in FQ4, up nearly 45% QoQ, including R&D loans. As such, management highlighted that it's near/at the limit of its balance sheet capacity and, therefore, will not likely be able to drive loan origination volumes from its balance sheet further.

So, how should investors react to that commentary?

Management articulated that it will not move toward creating a deposit base by incorporating a bank charter "like some peers," most likely referring to SoFi (SOFI).

Despite that, SoFi's recent performance demonstrated that it has managed to capitalize on its bank charter to drive robust loan originations in its personal loans segment, even as home loan and student loan originations were weak.

As such, Upstart's strategy remains focused on third-party funding to scale its capacity.

However, with the Fed's record rate hikes exposing a critical flaw in its model, how does the company intend to rectify its inherent disadvantage moving ahead?

Management argued that it has "upgraded" its model's capability, allowing Upstart to "understand and react to macroeconomic conditions and plans to launch the Upstart Macro Index or UMI" in Q1.

The UMI is designed to provide its lenders with "near real-time insight into the financial health of the American consumer." As a result, management is optimistic that the introduction of the UMI should provide its lenders with more visibility over the performance of its credit models relative to the macro headwinds.

In other words, Upstart is likely trying to assure its lenders that its AI models still work and has continued to improve, despite the macro impact. As a result, it aims to drive volume back from the lenders as the macro headwinds subside subsequently, accelerating its recovery.

Hence, the critical question is whether macroeconomic headwinds are expected to moderate moving ahead?

We discussed in our previous article that UPST's recovery could be driven by a surge in risk-on sentiments in the broad market, lifting speculative stocks.

Wall Street has also slashed its forward estimates significantly, as the company proffered cautious Q1 guidance. As such, UPST last traded at an FY24 EBITDA multiple of 15x EBITDA, which is no longer that attractive.

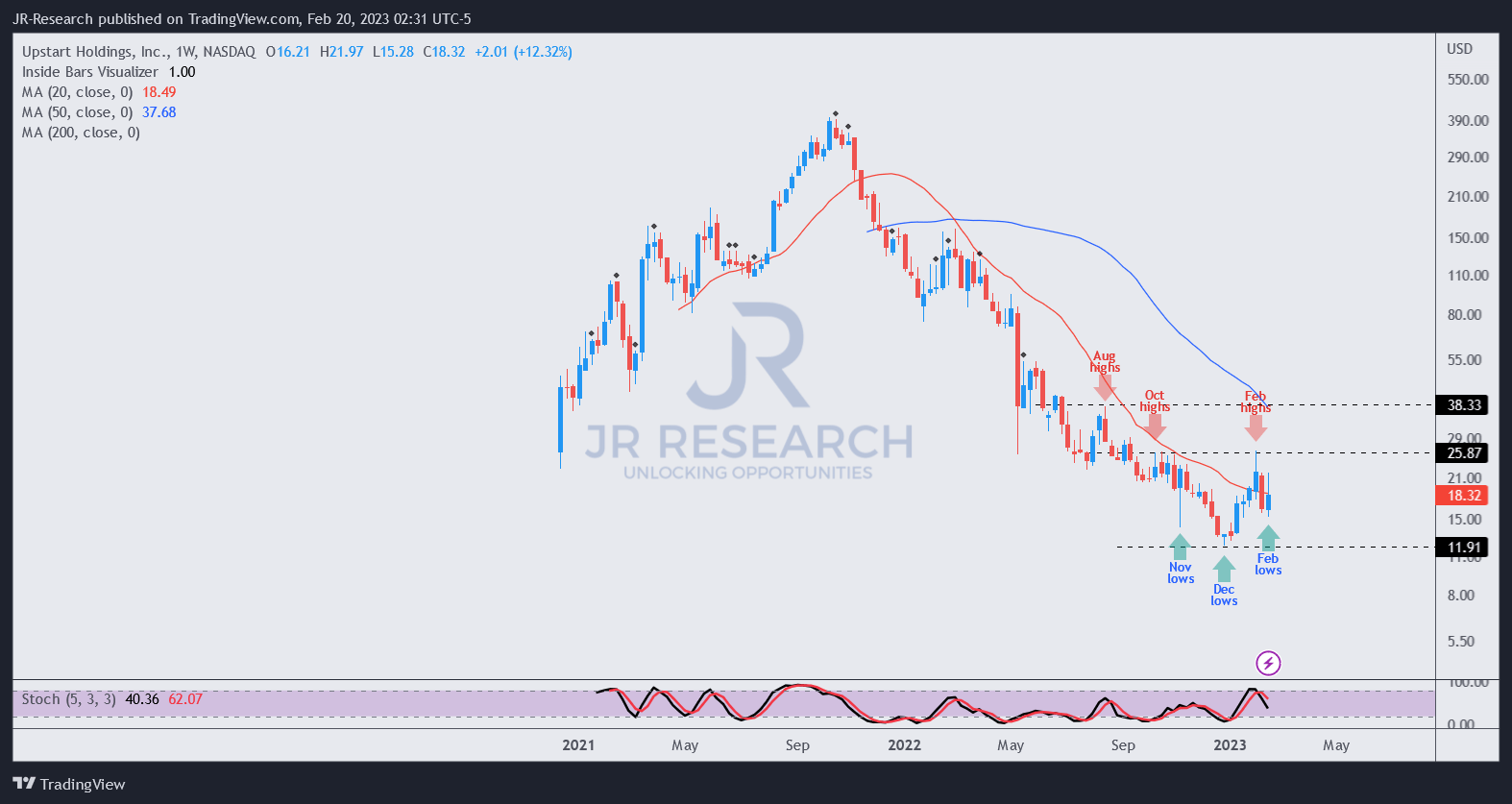

UPST price chart (weekly) (TradingView)

The recent surge toward its February highs (pre-earnings) was firmly rejected, in line with the highs in October.

Hence, that seems a firm resistance zone that likely attracted dip-buying investors at its December lows to unload and cut exposure.

With the recent pullback, UPST should continue to consolidate, but no longer as appealing.

While we think the worst should be over for Upstart, it still needs to chart a sustainable path with its third-party funding and its way back to profitability.

Moreover, we believe market operators will turn their attention back toward execution after the recent mean-reversion opportunity found significant resistance.

Rating: Hold (Revised from Speculative Buy).

Are you looking to strategically enter the market and optimize gains?

Unlock the key to successful growth stock investments with our expert guidance on identifying lower-risk entry points and capitalizing on them for long-term profits. As a member, you'll also gain access to exclusive resources including:

24/7 access to our model portfolios

Daily Tactical Market Analysis to sharpen your market awareness and avoid the emotional rollercoaster

Access to all our top stocks and earnings ideas

Access to all our charts with specific entry points

Real-time chatroom support

Real-time buy/sell/hedge alerts

Sign up now for a Risk-Free 14-Day free trial!

This article was written by

Unlock the secrets of successful investing with JR Research - led by founder and lead writer JR. Our dedicated team is laser-focused on providing you with the clarity you need to make confident investment decisions.

Transform your investment strategy with our popular marketplace service - specializing in a price-action-based approach to uncovering the hottest growth and technology stocks, backed by in-depth fundamental analysis. Plus, stay ahead of the game with our general stock analysis across a wide range of sectors and industries.

Improve your returns and stay ahead of the curve with our short- to medium-term stock analysis. We not only identify long-term potential but also seize opportunities to profit from short-term market swings, using a combination of long and short set-ups. Join us and start seeing experiencing the quality of our service today.

My LinkedIn: www.linkedin.com/in/seekjo

Disclosure: I/we have a beneficial long position in the shares of UPST either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.