Klepierre: Solid 2022 Results Reaffirm Bullish Thesis

Summary

- Klépierre delivered solid results for 2022 and has now basically recovered from the Covid crisis.

- Most key metrics, such as occupancy, continued to show improvement, even if the increase was relatively modest compared to the third quarter numbers.

- We believe that shares are undervalued, with a significant discount to NAV and trading at only ~10x guided net current cash flow per share for 2023.

Eva-Katalin/E+ via Getty Images

We continue to believe there is a lot of value in the shares of European class A shopping mall companies, perhaps even more than the US REITs like Simon Property Group (SPG) and Macerich (MAC), which we also consider deeply undervalued. Recently we wrote about Unibail Rodamco Westfield (OTCPK:UNBLF) and their 2022 results. It is now Klépierre's (OTCPK:KLPEF) turn, as the company just reported its end of fiscal year results. The first thing we'll note is that occupancy continued improving during the final quarter, but only slightly. Klépierre had finished the third quarter with occupancy at 95.6%, and it ended the year at 95.8%, therefore generating an improvement of only ~20bps. We believe that occupancy gains will prove more challenging going forward, but on the positive side, the high occupancy level will allow the company to focus more on increasing leasing spreads. On this subject, the company reported a 4.1% positive reversion, on top of 3.7% indexation, but we were expecting a higher number. For comparison, Unibail Rodamco Westfield's leasing spreads were better at +6.2%. Still, the two companies have a different geographic mix, which explains some of the difference.

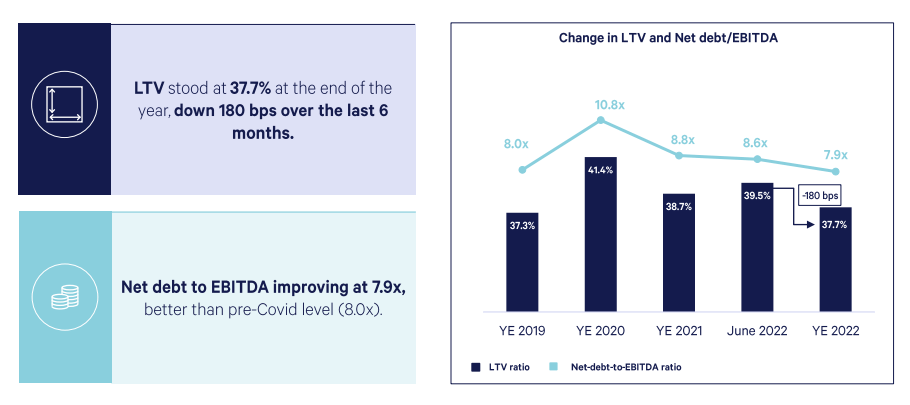

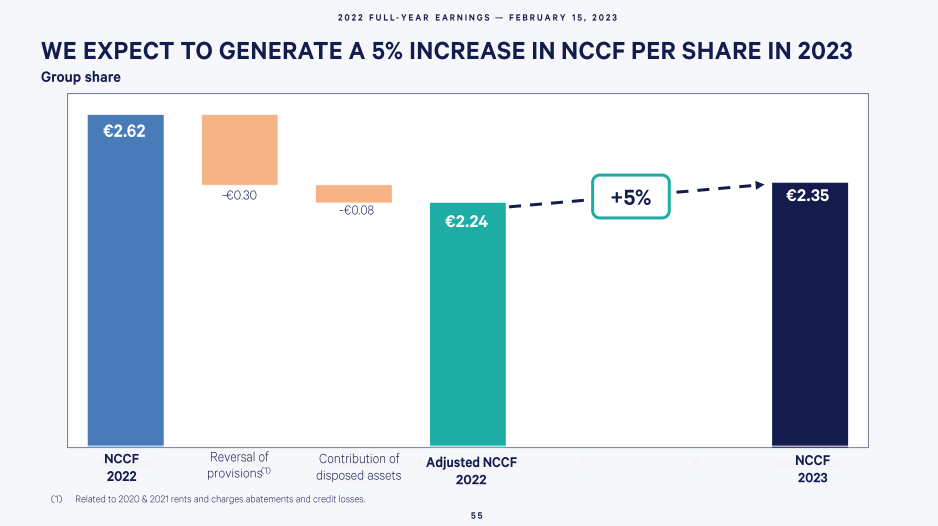

The strongest indicator Klépierre put out was net current cash flow up 20.1% versus 2021 to €2.62 per share, beating their mid-range initial guidance by 13%. It is important to note that this number includes some rent recovery from previous years, so perhaps it is better to use the 2023 net current cash flow guidance for valuation purposes. Net current cash flow per share for 2023 is guided at €2.35, putting the forward valuation multiple at ~10x based on the recent share price. The company confirmed it is paying a dividend in 2023 of €1.75 per share, which at current prices represents a dividend yield of ~7.4%, and it is very well-covered by net current cash flow. The balance sheet is also in excellent shape ending the year with a net debt to EBITDA of 7.9x, loan to value of 37.7%, and interest coverage ratio of 10.0x. While Macerich and Unibail Rodamco Westfield are trading with much cheaper valuation multiples, Klépierre's slightly higher valuation can be justified by its stronger balance sheet. Compared to Simon Property Group, the valuation is very similar, since it is trading with a forward P/FFO of ~10.4x, but we still find Klépierre more attractive given our belief that premium European shopping malls are likely to prove more resilient to the e-commerce threat as mall space per capita is much lower. Simon Property Group investors also have some exposure to Klépierre, as it is the largest shareholder with roughly 22% of the shares.

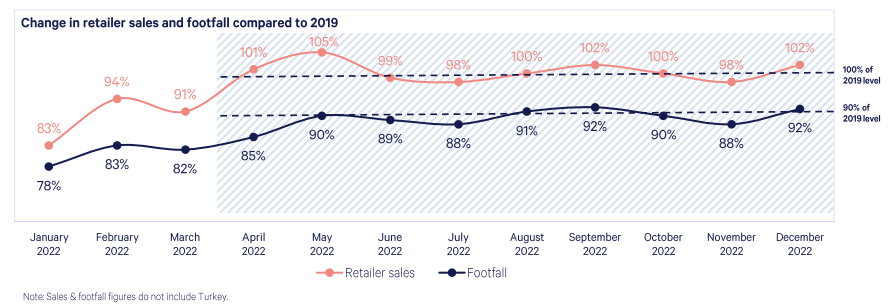

Retailer Sales

One of the big positives for Klépierre in 2022 is that its tenants are now reporting sales above pre-Covid 2019 levels. For instance, in December tenant sales averaged 102% of 2019 levels. Unfortunately this is not enough to compensate for the inflation experienced since 2019, meaning there is still significant room for improvement. Foot traffic remains about 10% below pre-pandemic levels, showing consumers are visiting less often but buying more per visit.

Klépierre Investor Presentation

Leasing

In 2022 Klépierre completed 1,360 leases, including 974 renewals and re-lettings, with a 4.1% positive reversion rate. This is on top of the 3.7% indexation applied in January 2022. Unibail Rodamco Westfield's leasing spreads were better at +6.2%, but Klépierre improved their average reversion number from the ~3% the company had reported as of their third quarter. Meaning that leases in Q4 must have brought the leasing spread average up for the year.

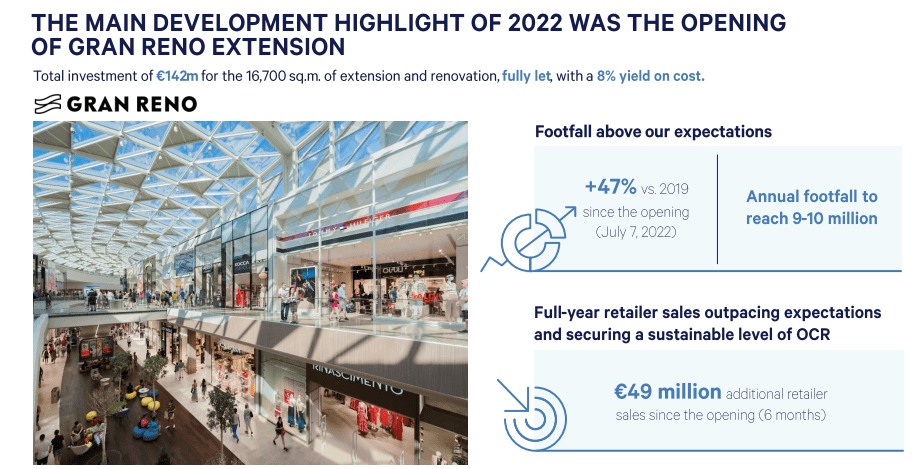

Development Pipeline

Klépierre has no retail greenfield projects, focusing instead on renovations or extensions, and mixed-use projects. In 2022 Klépierre focused mainly in delivering the Gran Reno extension in Bologna Italy, and the refurbishment and extension of Grand Place in Grenoble, France, which is expected to be delivered at the end of 2023. The retail projects pipeline stands at €634 million and the mixed-use project pipeline at €1.17 billion. The company is getting very good returns on these projects, for example, both the Gran Reno extension and the Grand Place extension are forecasted to have an 8% yield on cost.

Klépierre Investor Presentation

Balance Sheet

As previously mentioned, one of the differentiating factors of Klépierre is its strong balance sheet. It ended the year with consolidated net debt of €7,479 million compared to €8,006 million at the end of 2021. The company has a stable BBB+ investment grade credit rating from S&P Global (SPGI), and ended 2022 with €2.8 billion in liquidity. Net debt to EBITDA and loan to value have now basically recovered to pre-Covid levels.

Klépierre Investor Presentation

The company has a reasonable debt maturity schedule with a 6.5 years average maturity, although we would like to see it a bit higher. For example, Unibail Rodamco Westfield has an 8.3 years average debt maturity. The debt to be refinanced in 2023 and 2024 is not negligible, and will probably cause the average cost of debt to rise somewhat from the very low average cost of debt of ~1.2%. The company has an active interest rate hedging policy that has also helped mitigate the impact of rising rates.

Klépierre Investor Presentation

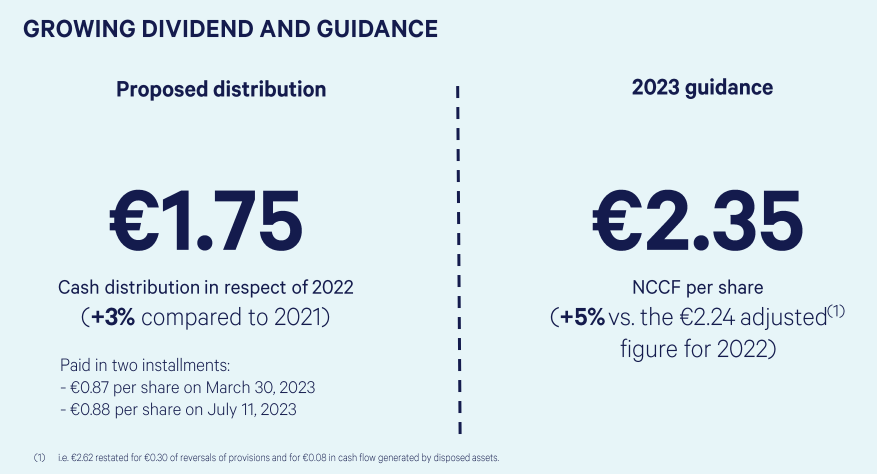

Dividend Yield

The dividend was increased by a modest ~3%, and is scheduled to be paid in two installments. A €0.87 per share on March 30, 2023, and the second of €0.88 per share to be paid in July 11, 2023.

We find the increase a little disappointing, but can understand why the company might prefer to err on the side of caution after what the industry went through due to the Covid impact, and the headwinds brought by increasing e-commerce penetration.

Klépierre Investor Presentation

Guidance

After adjusting for disposed assets and the reversal of provisions, net current cash flow per share is guided 5% higher in 2023. Importantly, this does not include the impact of any potential disposals in 2023. The main assumptions with respect to guidance are that retailer sales will be at least equal to 2022, that occupancy will remain stable around the current level, and that it will have a stable rent collection rate. We believe these assumptions show the company is being conservative, and should it make further occupancy and leasing revisions gains, it should be able to exceed guidance.

Klépierre Investor Presentation

Valuation

The company's EPRA Net Tangible Asset Value ended the year at €30.9 per share. This means that at current prices of ~€23.5, shares are trading with more than a 20% discount to the net tangible asset value. Since January 2021 the company has sold a significant amount of assets, and the sales have averaged only a 2.4% discount to book value. We therefore believe the company's NAV to be a good measure of intrinsic value, and that shares are probably at least 15-20% undervalued at current prices.

Klépierre Investor Presentation

Risks

A big headwind that Klépierre is currently facing is the increasing interest rate environment, which will likely make its average debt cost move higher as the company refinances.

The other big risk is e-commerce penetration continuing to increase. So far Class A shopping malls have proven resilient, and have been transforming themselves to be more experiential destinations. Klépierre also has the advantage that shopping mall space per capita is relatively low in Europe, and there is very little new supply coming online.

Conclusion

Klépierre delivered solid results for 2022, and has now basically recovered from the Covid crisis. Most key metrics continued to show improvement, such as occupancy, even if the increase was relatively modest compared to the third quarter numbers. We continue to believe that shares are undervalued, with a significant discount to NAV and trading at only ~10x guided net current cash flow per share for 2023. The company confirmed a dividend will be paid for 2023, even if the increase was a modest ~3%. Given the improvement in fundamentals and the attractive valuation we are maintaining our 'Strong Buy' rating.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of KLPEF, MAC, UNBLF either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities. Before buying or selling shares, you should do your own research and reach your own conclusion, or consult a financial advisor. Investing includes risks, including loss of principal.