Herbalife Nutrition: Q4 Earnings Could Be The Turning Point

Summary

- Herbalife Nutrition beat expectations for the fourth quarter, with EPS of $0.53, which topped forecasts by $0.19.

- The company's debt burden is a concern, but the management is committed to reducing it, which could drive investor confidence.

- HLF stock appears undervalued not only based on fundamentals but also on its stock chart.

- Even when including the net debt as part of the valuation, the company seems to be trading at a significant discount to its estimated intrinsic value and its historical average.

DNY59

Introduction

Herbalife Nutrition (NYSE:HLF) has just released its financial results for the fourth quarter and full year of 2022, reporting a decline in net sales compared to the previous year. The company has faced significant challenges in adapting to changes in consumer spending and inflationary pressures.

Despite the challenges, Herbalife still managed to beat expectations for the fourth quarter. I believe the strong earnings beat combined with its currently low valuation could be the catalyst needed for the stock to move closer to its intrinsic value.

Q4 2022 Earnings

Herbalife Nutrition reported fourth quarter net sales of $1.2 billion and the full year $5.2 billion, respectively. These figures represent a decline of 10.4% and 10.3% when compared to the previous year. The company saw a decline in revenue across all regions year-over-year, with China experiencing the largest decline at 45.5%, followed by EMEA and North America.

The company believes that macroeconomic inflationary pressures presented ongoing challenges to members' operations and customer demand during the quarter. Although currency pressure eased toward the end of the quarter, the U.S dollar remained significantly elevated over the prior year. The normalization of these pressures going forward should result in a corresponding improvement in revenue.

With EPS of $0.53, which topped forecasts by $0.19, the bottom line outperformed expectations as well. Active spending control was credited with helping the company manage margins and increase profitability, which led to the earnings surprise. Additionally, the company expanded and accelerated its previously announced transformation program.

Valuation

At the moment, the stock is at a low single-digit earnings multiple, which is usually given to companies that have unpredictable and fluctuating profits, or a lot of debt. In my opinion, the reason for the low valuation is due to both of these factors and a general pessimistic attitude towards the industry.

I think the main reason behind the low valuation is the significant decline in EPS observed in the past year which saw a decline of -29% combined with the expected decline of -23% this year.

The industry as a whole is currently experiencing a slowdown, and it may take some time for things to turn around. Herbalife has been facing challenges in adapting to the changes in consumer spending. However, the company's new CEO, Michael O. Johnson, who has previously served in the same role, has promised growth with the launch of Herbalife 2.0. While it's uncertain if the new strategy will be successful, the positive earnings beat is certainly a good start.

Now on to the future. Here's my promise, our sales will grow and our results will improve. I'm fully aligned with our Board, our investors, our distributors and our employees to usher in a new era of growth for Herbalife.

The company's high level of debt relative to its market capitalization at a standard 15 earnings multiple reinforces the argument for a deservedly lower multiple. In its latest quarter, Herbalife reported a net debt of approximately $2.5 billion, which is significant when compared to not only their current market cap, but also to their market cap of around $4.1 billion at a 15 earnings multiple.

If we include the net debt to the market capitalization and calculate the price per share at a 15 earnings multiple, we can estimate the intrinsic price to be ~$28. I believe this estimate is conservative, as it factors in the large amount of debt the company is currently carrying.

The management expressed a commitment to reducing the heavy debt burden. I believe this will be a catalyst for the stock to return to its intrinsic value. As the debt is gradually paid off, concerns about its sustainability should subside, which could drive investor confidence.

We ended the quarter at 3.47x gross debt to adjusted EBITDA, which is above our target leverage ratio of 3.0x. The company plans to use free cash -- free cash flow generation in 2023 to reduce our overall debt.

It's worth noting that the undervaluation isn't unique to Herbalife, as other major players in the industry, including Usana, Medifast, and Nu Skin, are also experiencing similarly low valuations. The industry as a whole is experiencing a slowdown, which may take some time to turn around.

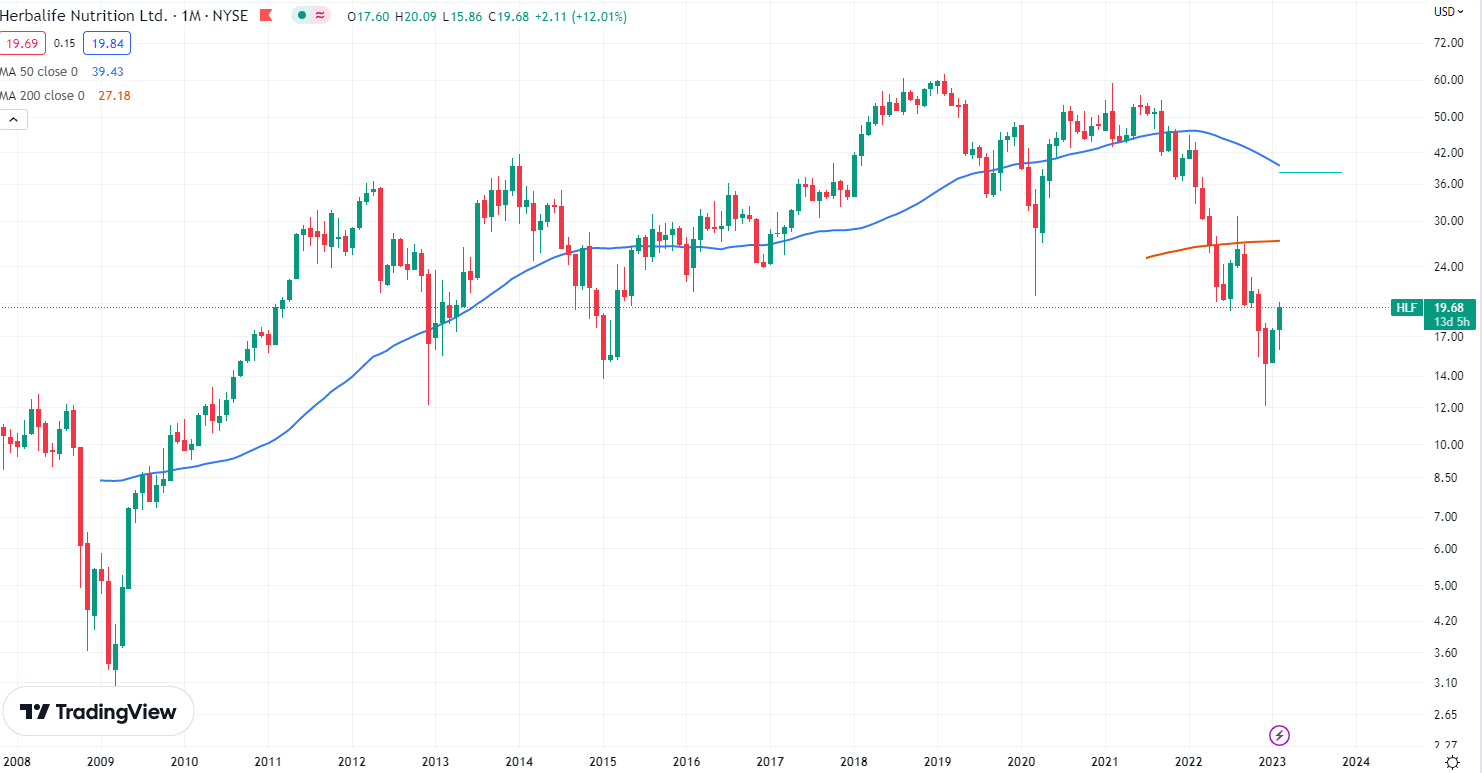

Stock Chart

Quick disclaimer: A technical analysis in itself is not a good enough reason to buy a stock, but combined with the company's fundamentals, it can greatly narrow your price target range when you buy.

Herbalife appears undervalued not only based on fundamentals but also on its stock chart. For the past 10 months, the company has been trading significantly below its 200- moving average. This is significant because, although declining at the moment, the company's EPS is still expected to recover and grow in the future.

A return to its 200 moving average would put the stock at ~$27, which is in line with the estimated conservative intrinsic valuation of ~28.

Tradingview.com

Final Thoughts

Despite facing challenges such as slow growth, significant debt, and being part of an industry that is currently receiving low valuations, I continue to believe that the company is undervalued. Even when including the net debt as part of the valuation, the company still seems to be trading at a significant discount to both its estimated intrinsic value and its historical average multiple of 12.84, suggesting a margin of safety of approximately ~44%.

The recently announced earnings report shows encouraging signs of recovery, which adds to the argument for a higher valuation. Additionally, both of the factors contributing to the current low valuation - stagnant growth and high debt - are being actively addressed and improved upon. The company is making efforts to reduce its debt and the CEO has promised to focus on both growth and stabilization.

Given these factors, I maintain my "Buy" rating on the company.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of HLF either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.