The Beachbody Company: How Much The Story Changes In Two Years

Summary

- Beachbody is a health and wellness platform that took the SPAC route to public markets.

- This company is a cautionary tale for investors to stay away from rosy projections and celebrity sponsor/endorsement of investments.

- As an investor or just as an observer of stock markets there are plenty of lessons to be learnt here.

Jovanmandic/iStock via Getty Images

Then & Now

A child of the pandemic, the company (NYSE:BODY) went public in 2021 through much fanfare. Among the many boosts the pandemic provided to certain industries, in-home fitness was one of the most popular ones. There were many companies who took advantage of the trend and I certainly don’t blame the companies for making-hay-when-the-sun-shone. But it was up to the investors to do their due diligence. Instead, investors looked the other way and bought into the company's story of growth and projections, TAM, hype and celebrity endorsements along with complete disregard for valuation. Now we are left with a penny stock that didn't meet any of its promises and has no concrete plans to put themselves back on the map. In my write-up below, I will aim to compare the story across the two years and see what lessons an investor can learn from this.

Celebrity endorsement

Shaquille O'Neal along with other executives raised money for a SPAC that eventually merged with Beachbody. At the time his name was plastered every where to "sell" the deal to investors. Anyone who bought into this hype have a more than 95% drawdown on their investment that they have no answer for.

I am highlighting this as a first red flag for investors. Anytime a company starts off an investment pitch by hiring celebrities to endorse its products or say prime celebrities are involved in the company, its time to start being cynical on the investment (Most recent example, Tom Brady and FTX) Of course, it could be unfair to say this but an investor has to remember - Business is business, personal is personal. Never mix the two.

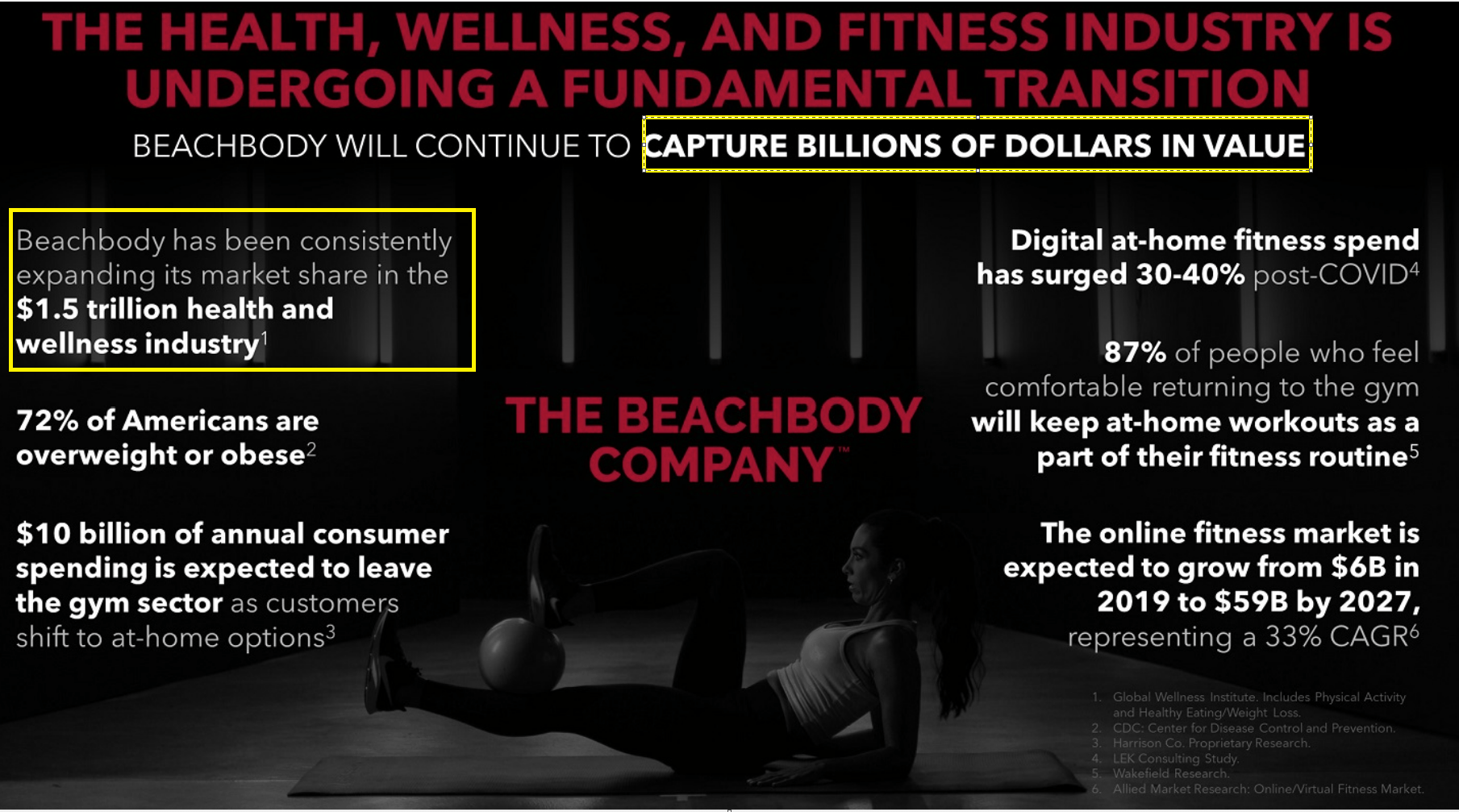

TAMSanity

I saw this term coined by Jim Chanos, the famous short seller of our generation. It's a play on the abbreviation for Total Addressable Market. In essence what this means is that companies throw big numbers on the addressable market and since they are going after it, it is implied and sometimes explicitly said that it would translate to their topline. It is up to the investors to take this with a grain of salt. During investor presentations two years ago, I did feel the company was guilty of this and some of the numbers on their presentation were laughable.

Company's investor presentation on SEC website

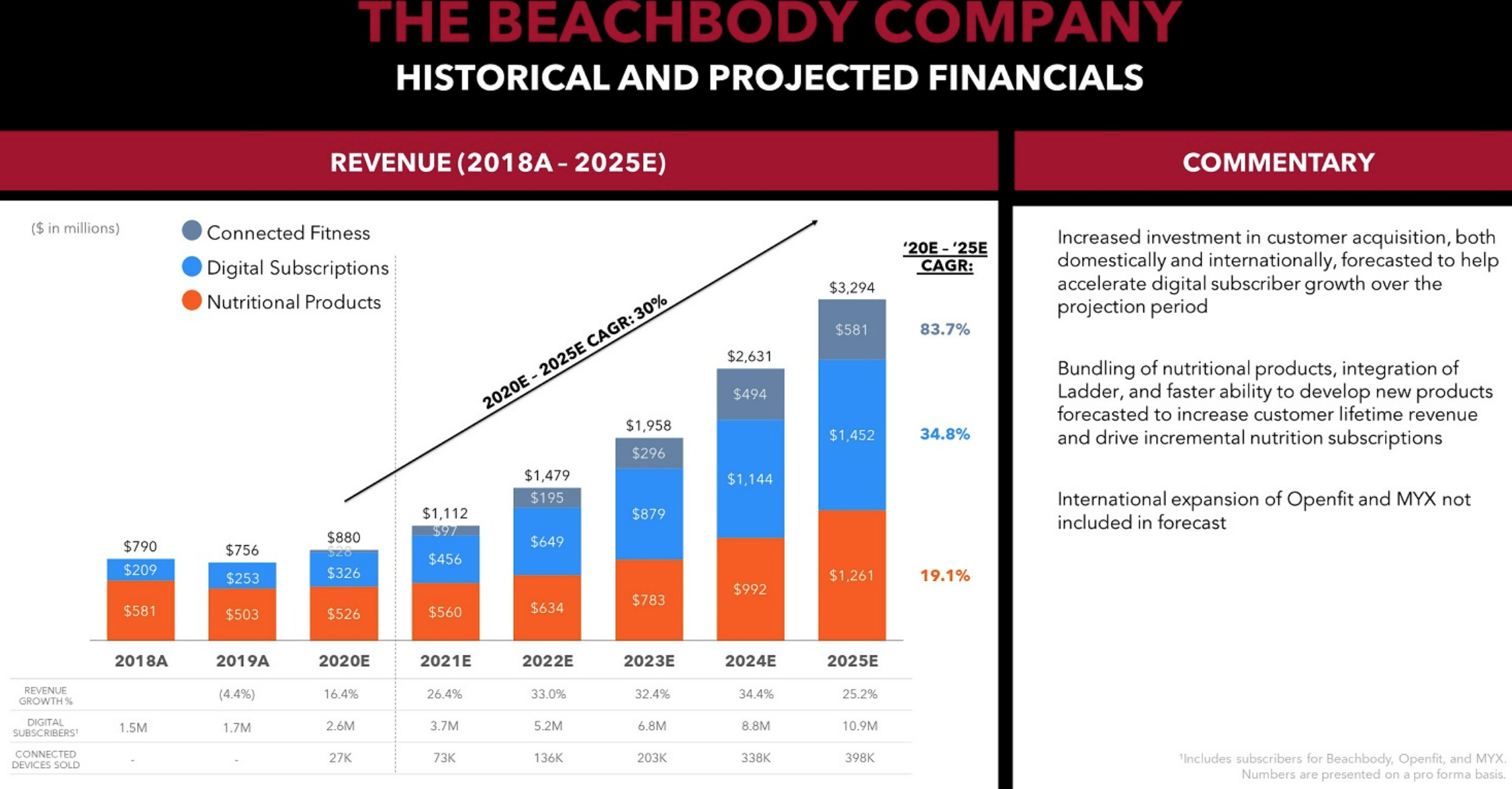

Projections

One of the earlier advantages of taking the SPAC route to public market was that the sponsors could include projections as part of the deal. Although some of these rules may have been tightened now, it still leaves a majority of the public to make up the numbers to pump an investment and this lesson will serve us well regardless of the new SEC rules. The company barely showed any growth in its prior years but projected growth numbers from 15 to 35%. It had its own language to justify this rosy growth projections and this is yet another area where investors need to be skeptical.

Company's investor presentation in SEC website

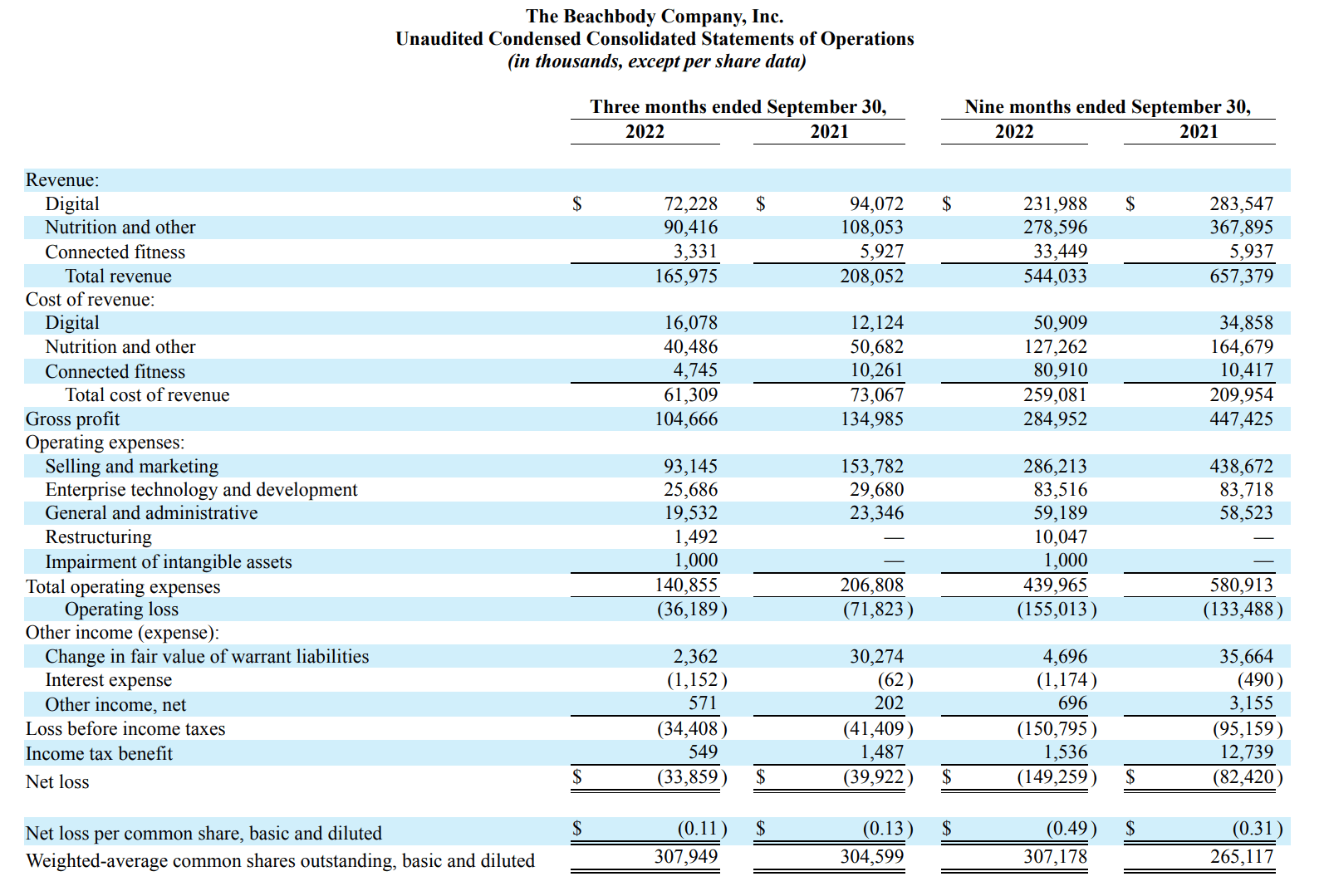

Fast forward to now the company is no position to meet its projected numbers for 2022. For the nine months ended on September 30, 2022 when compared to the same time period of 2021, total revenue decreased by 17%, and net loss was $149M compared to $82M of last year! Their revenue from the last 9 months ($544M) has a long way to catch up to their projections of $1.4B!

Maybe it's my optimism that is lacking and I need to believe in them more!

Seeking Alpha Filings

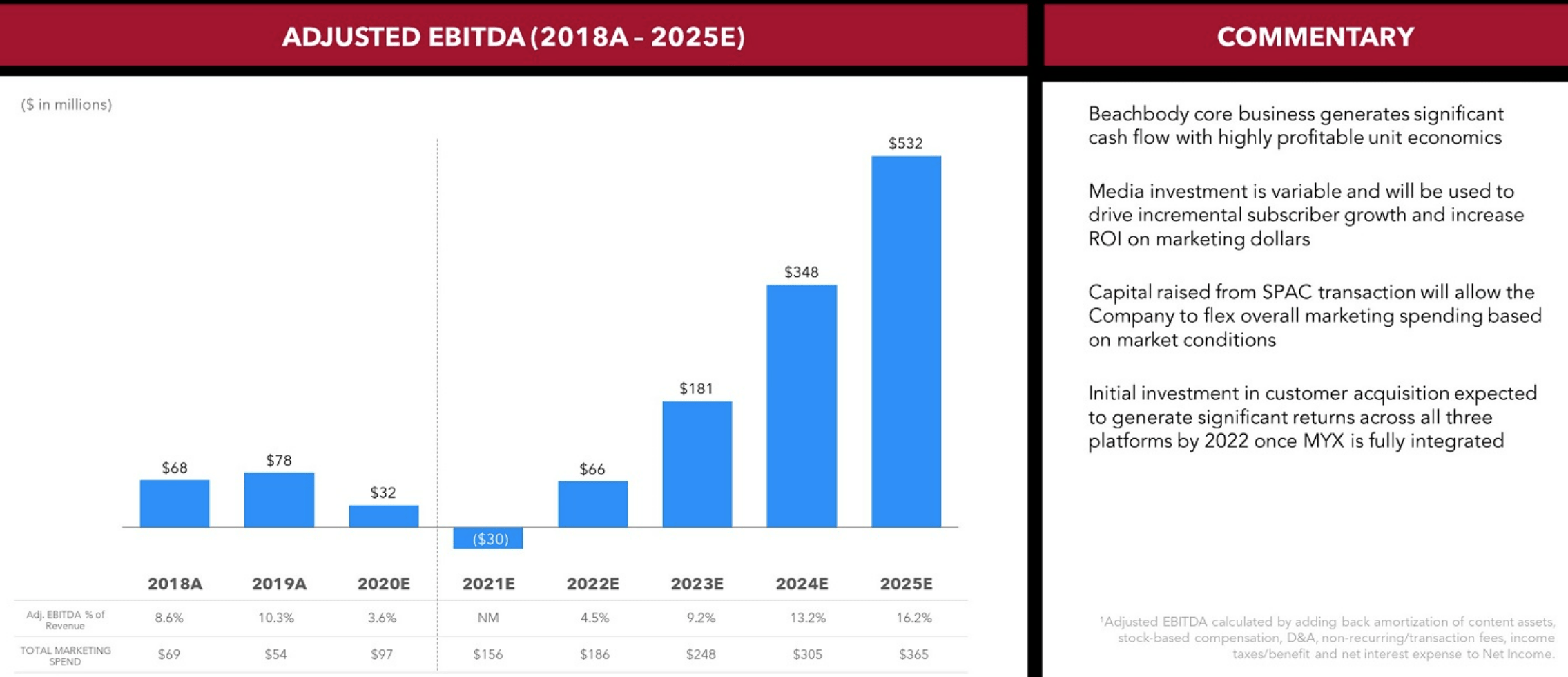

Adjusted EBITDA

Every time you hear 'EBITDA' substitute it with 'bull**** earnings

- Charlie Munger

This is not only EBITDA but adjusted EBITDA! This is a famous metric many times used to pump investments and show that the company is/would be profitable. EBITDA is already a made up metric (non-GAAP) but when you say adjusted it means it's made up even more! From their deck, they were already projecting a negative adjusted EBITDA the following year but for the years after, the company claimed this would just start shooting higher by some justification.

Company's investor presentation in SEC website

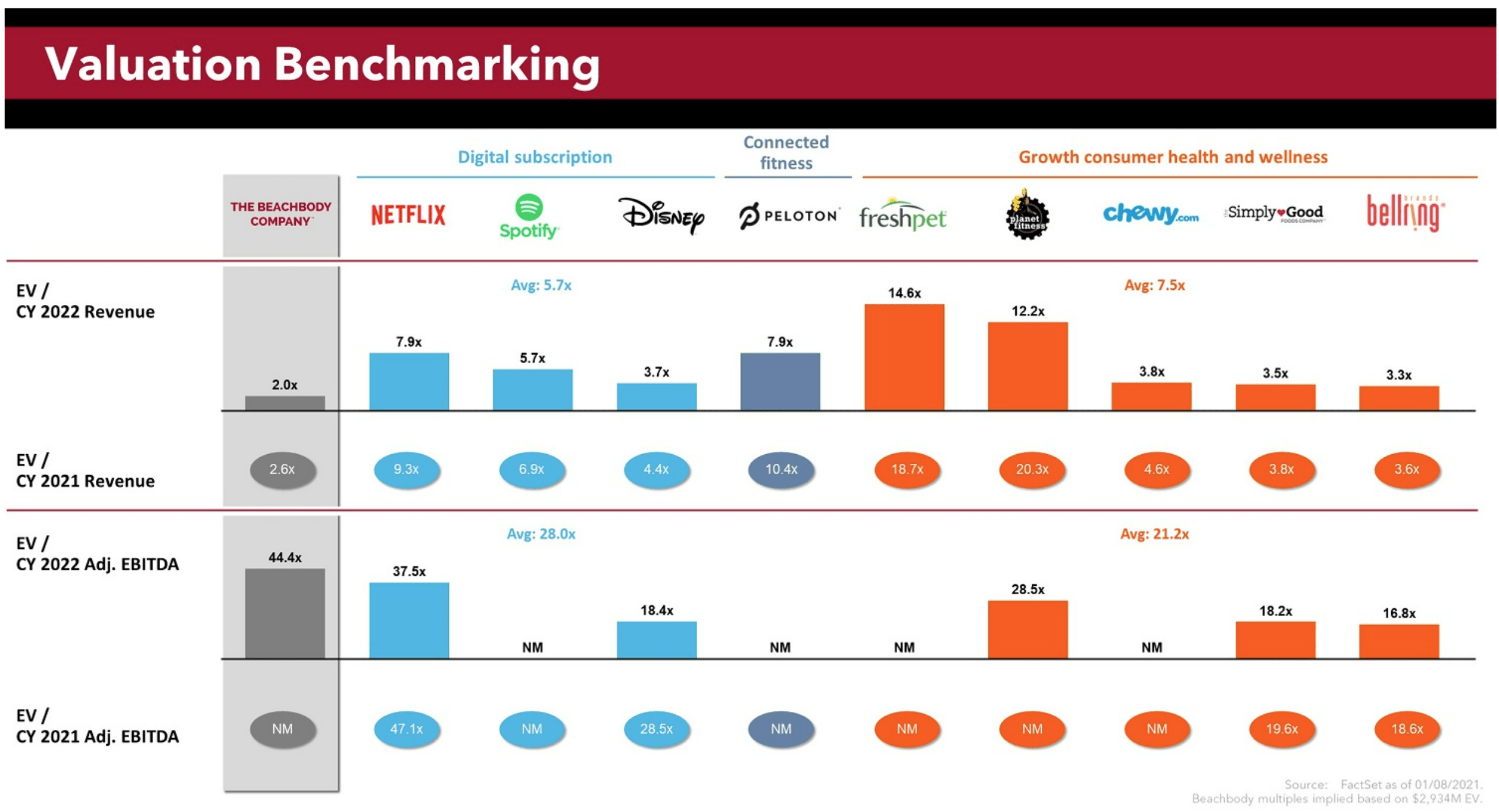

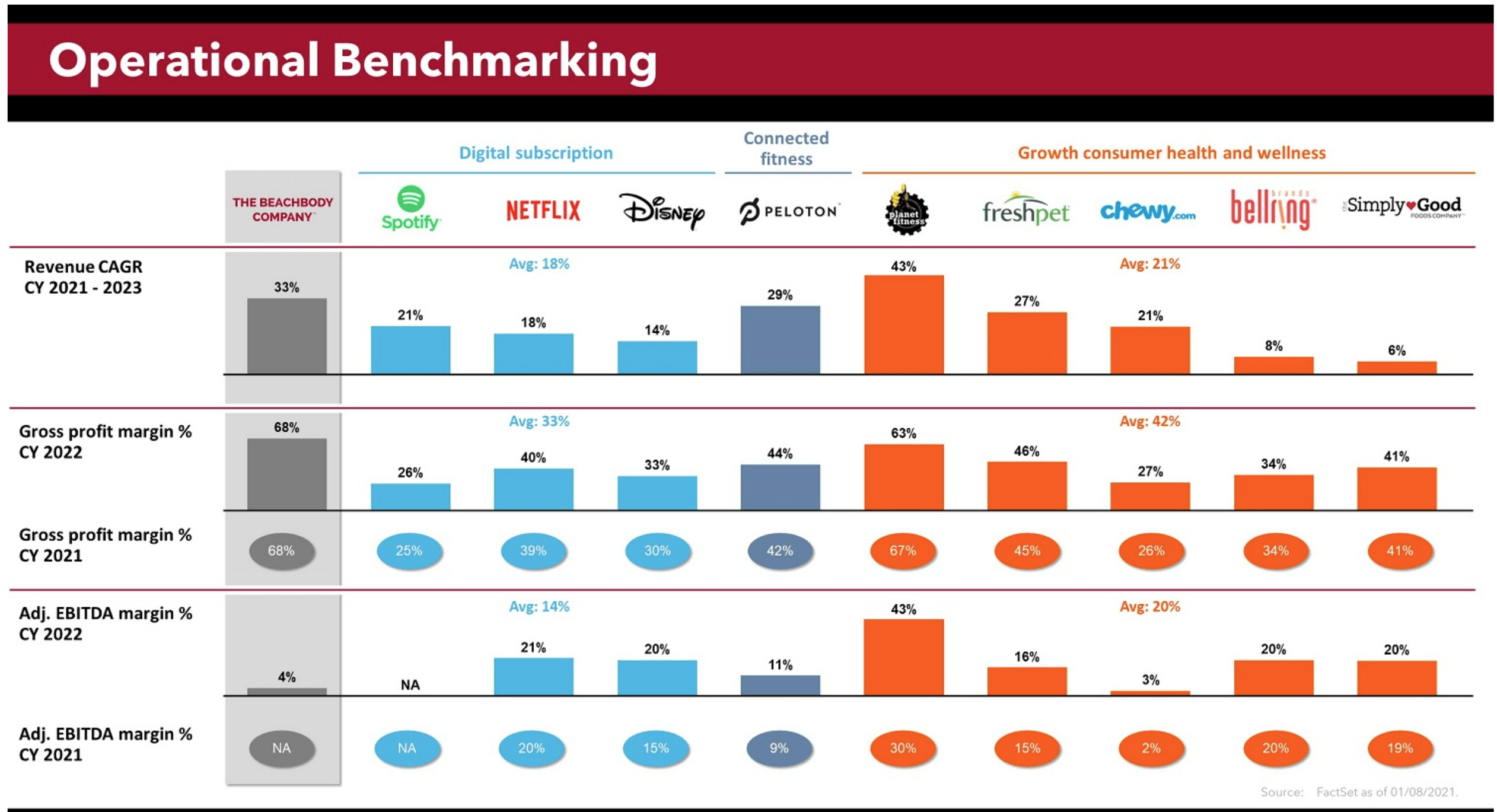

Valuation

When selling this merger to prospective investors the comparables shown by the company made little sense. On the digital subscription side, it was comparing its EV/R to established mega caps like Netflix and Disney and on the consumer health and wellness there was Chewy. I guess if you cherry pick your competitors it's easy to make your case on anything.

Company's investor presentation in SEC website

Company's investor presentation in SEC website

Fast forward to now, valuations make a little more sense. The company is still deeply unprofitable so most metrics are not applicable. Currently at a PS ratio of 0.25, it looks cheap after its 95% drop. But its growth is continuing to crater and if history is any indicator it will continue to get cheaper.

Final Call

The company's debt is well covered by its cash on hand. This will allow it to survive for the short term. But its unprofitability and negative cash flows means its cash runway is limited. Unless they can raise money through debt or by other means, the future looks grim for the company. Its valuation looks cheap and unless an investor looks at this from a valuation standpoint and mixes this with some more speculation, it's hard to make a case for this company. I rate this as a Strong Sell.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.