For an airline that magnificently executed its plan to bring in the first 100 aircraft, there have been many hiccups since the induction of “neos” started – all beyond the control of the airline

IndiGo, India’s largest airline by fleet and domestic market share, will declare its earnings for the second quarter of financial year 2022-23 on November 4.

The results and subsequent investor call are much awaited by the aviation and investment community for more than one reason this time: reports that IndiGo is inducting wet-leased wide body aircraft for the first time; it’s the first investor call for Pieter Elbers, the new CEO; the first quarterly results after the launch of Akasa Air; and the loss in Q1 even though it recorded the highest ever revenue and flights in its history.

The question is whether the airline will cross the Rs 10,000 crore revenue mark, as it did in Q1 for the first time after 10 quarters. One would also get to know the impact of the removal of fare caps on the bottom line.

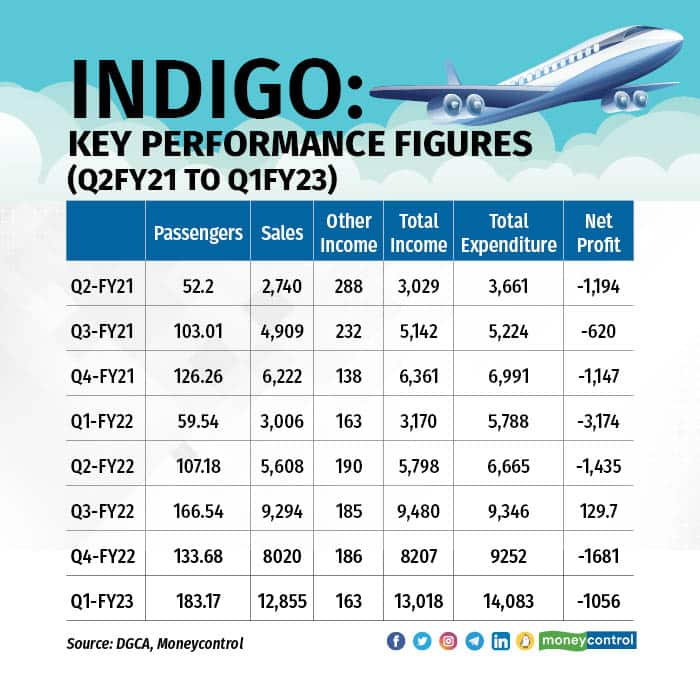

With revenue of Rs 13,018 crore in Q1, the airline still ended up with a loss of Rs 1,056 crore, all of which was attributed to currency exchange losses. There has been little respite on this front since then and in fact things have moved the other way round.

Q2 highlights

The airline closed the quarter with a market share of 58 percent, a 1.7 percent gain over the last quarter. The airline carried 17.5 million passengers in Q2, which was 4.4 percent lower than the previous quarter, when it carried 18.3 million people. IndiGo has been able to gain market share by not sliding as much as overall passenger traffic, which dipped 7 percent.

The number of IndiGo’s passengers was 5 percent more than in the October-December quarter of FY22, when the airline last recorded a profit (Rs 129.7 crore). Oil prices peaked in July and while they have declined since then, they remain higher than in the previous quarter, which would have put further pressure on the cost side. Fuel comprises 35 percent to 40 percent of airline expenses, putting profitability under question.

More complicated is the slide of the rupee. From the start of the quarter to its last day, the rupee has depreciated 5 percent against the dollar. Leasing and maintenance costs are dollar denominated and the airline may not return to a profit due to mark-to-market losses.

What is certain is that the airline will once again cross the Rs 10,000 crore revenue mark in Q2 on the back of passenger numbers and the elimination of fare caps. The fare caps were abolished from August 31, leading to a drop in fares to stimulate demand. The airline could see a drop in yields as compared to its recent past.

What to watch out for

The rupee has depreciated 9 percent against the dollar over the span of one year. This directly increases dollar-denominated costs for airlines such as leasing.

The airline also announced progressive reinstatement of salaries. Employee costs were 7.5 percent of total expenditure last quarter, but costs keep changing. In isolation, the costs went up 11.4 percent sequentially.

A couple of IndiGo’s aircraft were grounded due to supply chain issues with the engine manufacturer. Is there compensation built in for that? Will the carrier announce the induction of wet-leased wide body aircraft? Where would it deploy them?

IndiGo: Key performance figures (Q2FY21 to Q1FY23)

IndiGo: Key performance figures (Q2FY21 to Q1FY23)

Tail note

The hope is that the likely drop in yields will be compensated by increased passenger numbers. But the airline has not had the best of load factors, which is an indicator that it has decided to hold on to yields over passengers.

Challenges on the supply side with aircraft manufacturers and subsequent delays in engines and newer deliveries has meant that capacity addition in Indian skies has been moderate.

For an airline that magnificently executed its plan to bring in the first 100 aircraft, there have been many hiccups since the induction of “neos” started – all beyond the control of the airline.

Any plan to induct wide body aircraft could cause a massive drain on finances. The airline has cumulatively lost Rs 11,000 crore over the past 20 quarters. The ongoing quarter could well decide IndiGo’s future path like never before.