Managing money is not just a fund manager’s bastion. Life insurance companies also manage policyholders’ corpus.

And these are not just pure term policies. Life insurance companies also have investment-cum-insurance products where they solicit money from policyholders and invest in equity and debt markets.

And they have fund managers to manage these policies; the aim is to generate a higher return enough to meet all redemptions as and when they happen. In fact, life insurers are among the largest investors in the domestic market, led by the Life Insurance Corporation of India (LIC).

Meet Poonam Tandon, Chief Investment Officer of private life insurer IndiaFirst Life Insurance, who is in charge of investing retail policyholders’ money.

Although fund managers of insurance companies do not quite share the pressure that mutual fund managers face, particularly in terms of short-term withdrawals, insurance companies too are in chase of returns.

In an interaction with Moneycontrol, Tandon tells us how retail investors should deploy their money in the current scenario.

Is it safe to invest in equities today?

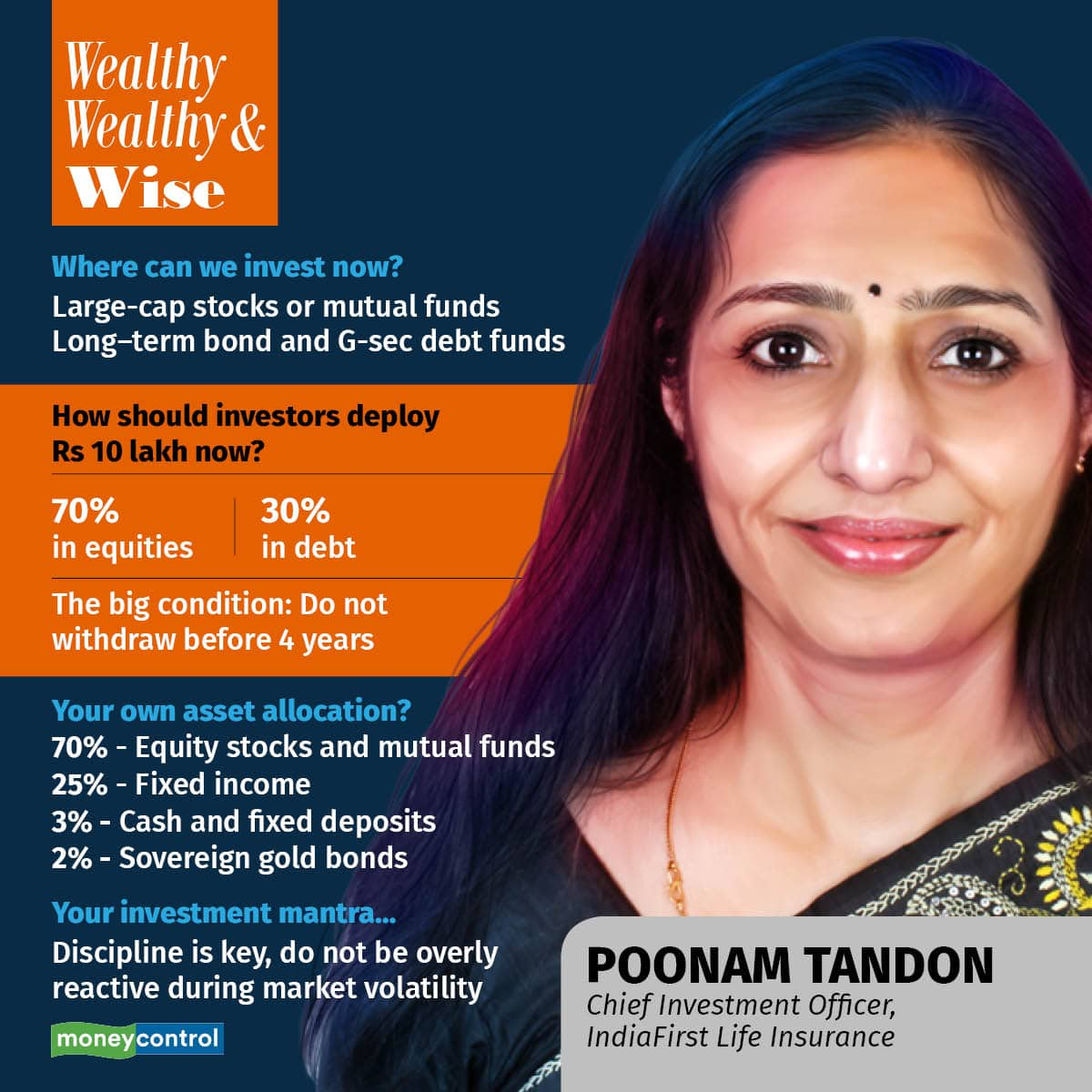

Market conditions are good for equity investments, especially in the Indian scenario, although the global markets are going through turbulence. Investors should look at larger allocation to large-cap stocks and funds, as these have emerged stronger during the pandemic.

Also, large institutional inflows are likely to be seen in these stocks. Put simply, look at investing in strong companies with healthy balance sheets and excellent track records in terms of growth as well as corporate governance. You should focus on these parameters, irrespective of whether you are into individual stock-picking or looking to invest through mutual funds.

What would your advice be for someone looking to invest Rs 10 lakh now?

The advice would depend on the individual’s age, risk appetite, life stage and so on. However, if you have Rs 10 lakh which you won’t need it for the next three to four years, you can consider putting 70 percent in equity and 30 percent in debt. In 3-4 years, it is likely to give inflation-beating returns.

How should investors go about deploying funds in fixed-income instruments, in the context of rising interest rates?

Look at investing in long-duration and sovereign bond funds and fixed-maturity ETFs. The yields have gone up by 175 bps in the ten-year bellwether bond from the lowest point in 2020, during the pandemic.

The Monetary Policy Committee has continued with its ‘withdrawal of accommodation’ stance, which translates into a higher interest rate regime considering that the inflation is higher than the tolerance level of 4-6 percent.

The fact also remains that other powerful central banks of the world are increasing rates aggressively to curb inflation. We can still expect a few more hikes. For those investing for the short-term, debt funds with a three-year modified duration would be a good bet too.

With volatility in the markets likely to continue, how can investors insulate themselves against the risks?

Although there will be volatility in the short term, those looking to invest for the long term should use this opportunity to increase their allocation to good quality large-cap funds and stocks.

However, if they are not confident about dealing with this volatility, they should at least remain invested instead of selling or withdrawing from their portfolios when (stock) prices are lower. They should also invest as per their risk appetite and not take on risks they cannot afford to.

What is the ideal asset allocation for retail investors?

There is no one-size-fits-all formula. It depends on your age, risk profile, life-stage and liabilities. A young investor who has just started her career can invest a majority of her savings in equities, as this will ensure a large retirement corpus. Those who are close to retirement can invest more in debt and a small percent in equities.

Middle-aged individuals with loans, children’s education expenses and parents’ medical expenses might have their plates full but should still try to set aside some amount to create a retirement corpus with some portion in equity.

It is always best to invest systematically, spread your risks, and review your portfolio periodically, but not be overly reactive during periods of volatility.

What are the risks that retail investors should be aware of?

There could be a liquidity crunch in the system due to the tightening (rise) of interest rates. Short-term rates are expected to increase. Central banks world over are in tightening mode, so globally there could be headwinds. Markets may not have fully factored in geopolitical tensions. So it is necessary to keep a little bit of spare money in cash with you – up to 3 percent of your portfolio should be in cash, instead of deploying all that you have.

Diwali is around the corner, and many of us look to buy gold or real estate during this time…

You can look at allocating around 5 percent of your portfolio to gold – sovereign gold bonds are a good option for retail investors. There is no credit risk as the government of India is the issuer and it also gives a coupon income every six months with a tax advantage in the long term. As far as real estate is concerned, it should be only for residential purposes. Real estate is an opaque sector with several challenges in buying or selling properties. If you want to take exposure to real estate, REITs are better alternatives.

How do you invest your own money?

I have invested in equities, mutual funds, ETFs, tax-free bonds, sovereign gold bonds and fixed deposits. Depending on market movements, I keep making switches.

My portfolio is tilted towards equities - around 70 percent of my portfolio is made up of equities, while 25 percent is into fixed income instruments. Cash and fixed deposits make up 2-3 percent of my portfolio, with 2 percent being invested in sovereign gold bonds.

Your investment mantra…

Be a disciplined investor. Do not be overly reactive in times of market turbulence. Ensure that you invest separately towards long- and short-term goals, and do not withdraw investments meant for long-term purposes (such as retirement) to fund short-term needs. Always invest through regulated entities.