Fed chair Jerome Powell

The level of hype heading into the annual central banking symposium in Jackson Hole, Wyoming, is even more intense than usual, and it’s easy to understand why. The US is battling the worst inflation in four decades, and investors are eager to sniff out clues about the Federal Reserve’s next moves. But history shows that all the brouhaha is overdone, and the real direction in markets will come from economic data streaming in over the ensuing months.

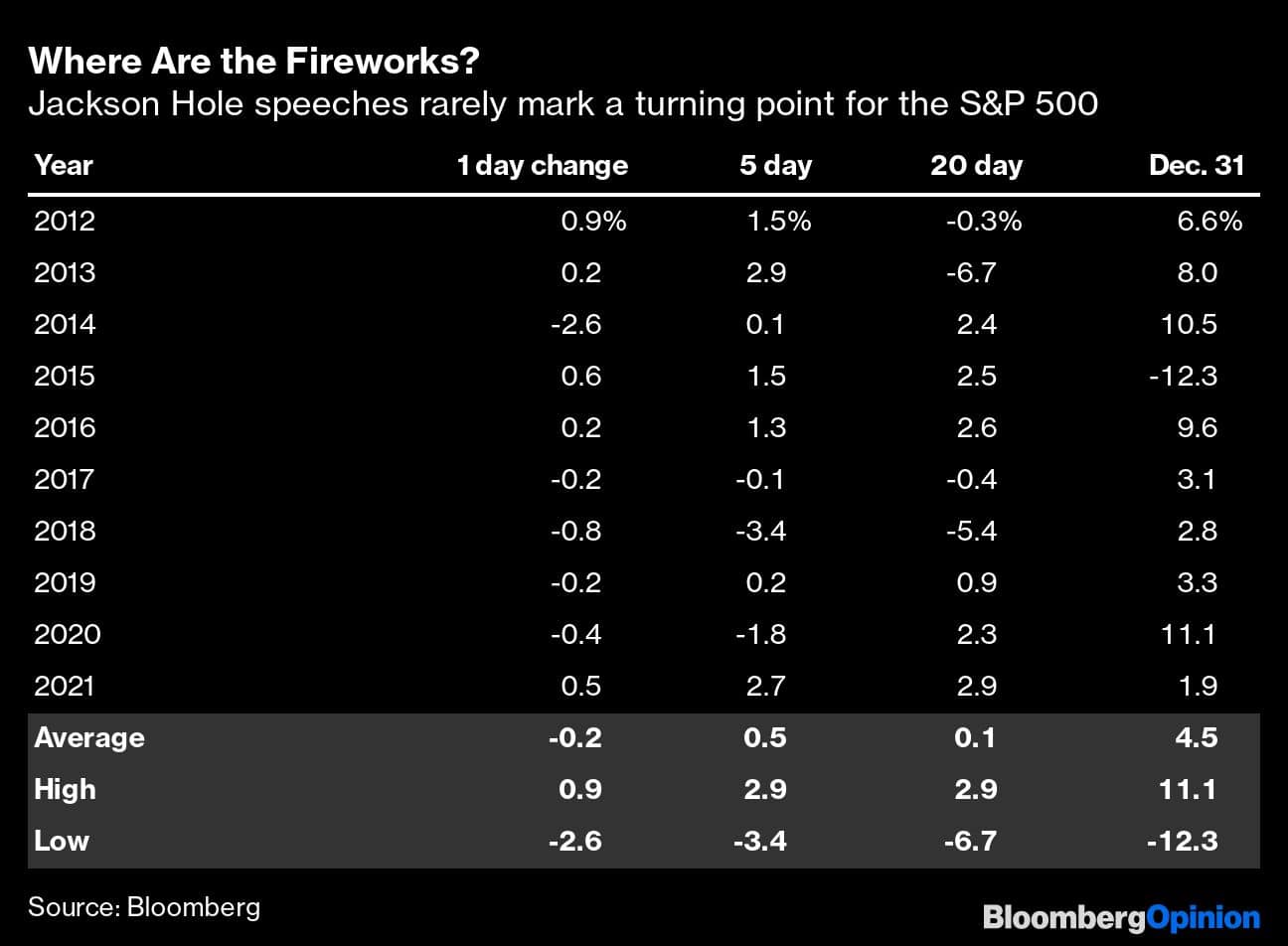

By the numbers, Jackson Hole is almost never the pivotal moment it’s made out to be. In the past decade, the S&P 500 Index has lost 0.2% on average on the day of the marquee Fed speech (usually the chair’s address). The index was typically up 0.5% after five days; 0.1% after 20 days; and 4.5% by the end of the year, counting from the day of the speech. In other words, the typical moves are less than one standard deviation, and there isn’t a whole lot of dispersion around the mean. The chair’s speech is generally no big deal.

Where Are the Fireworks? | Jackson Hole speeches rarely mark a turning point for the S&P 500

The largest single-day rally in the period came last year when Fed Chair Jerome Powell cheered markets by saying that personal consumption expenditures inflation, then at 4.2%, was “likely to prove temporary” and that near-zero interest rates remained appropriate. That was an unusually tradeable message as markets extended their gains through the end of the year. But it was also woefully incorrect in its diagnosis of the problem, and Powell ended up paying for his initial reluctance to react. By now, the market has given back all those gains.

The most ferocious of the selloffs was the 2.6% single-day drop in 2019, but it wasn’t actually Powell’s speech that did the damage. He declined to provide new forward guidance and delicately validated already dovish market expectations. Ever the upstager, President Donald Trump stole the show in part by criticizing the Fed’s failure to cut rates faster and by also threatening China on Twitter in a brewing trade war. It was Trump that upended the trading session, not Powell.

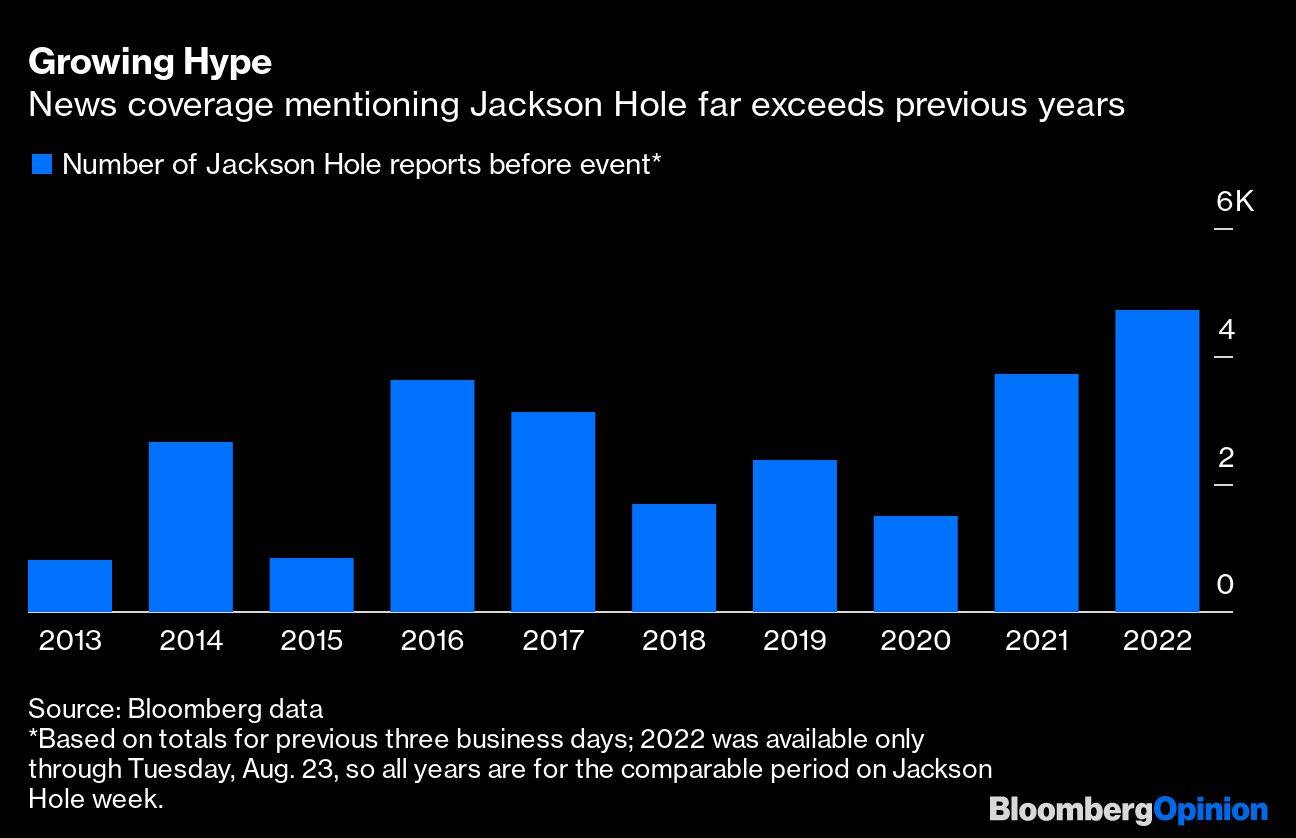

The founders of the 44-year-old conference would probably find the hysteria something to behold. The Federal Reserve Bank of Kansas City started the symposium in 1978 with an initial focus on world agricultural trade, and it has been gaining notoriety steadily since it moved to Jackson Hole in 1982, with former Fed Chair Paul Volcker attending that year. Data shows that top news organizations have churned out more Jackson Hole reports before the event this year than at any other time in the past decade.

Growing Hype | News coverage mentioning Jackson Hole far exceeds previous years

Certainly, the extra intrigue makes some sense. The peak in headline inflation may be in, but there’s much remaining uncertainty about how fast it will decline — and how far. It’s still not clear how the Fed will react if inflation gets bogged down next year in the 3% to 5% range and the economy is slipping into a serious recession.

There could be some incentive for Powell to bring out his inner hawk, of course. The Fed relies on markets to efficiently transmit its policies, and financial conditions have loosened considerably over the past couple months, although a lot of that comes down what’s happened with corporate bond spreads and stocks — Fed fund futures and short bonds appear to be more or less where policy makers would want them. At the same time, mortgage rates are cooling the housing market rapidly and risk triggering home equity losses, so hawkish jawboning will require some nuance. Without implying a higher terminal rate, Powell could achieve some tightening by pledging to keep rates high through 2023 or until the Fed achieves some milestone in the inflation fight.

But don’t expect Powell to shock the world on Friday. Economic data on growth, inflation and jobs will prove to be the real catalysts through the end of the year. A significant broadening of the disinflationary trend over the next couple of months could change the market narrative, as would any sign that wage growth is moderating and won’t remain an enduring upward force on inflation. As for Powell, he’s likely to follow in the great tradition of Jackson Hole symposiums and not rock the boat. Would he take a slight and gradual tightening of financial conditions? Absolutely. But the last thing he wants is to engineer a crash, and he’ll err on the side of delivering a tepid nothingburger if that’s what he thinks it takes.