High commission rates in life insurance policies have been a sore point with policyholders for long.

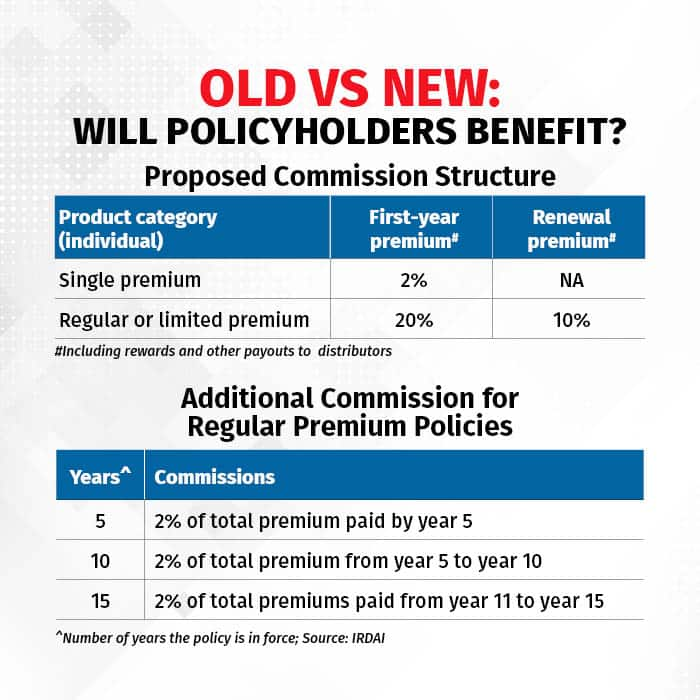

If the Insurance Regulatory and Development Authority of India’s draft paper on limiting commission pay-outs to intermediaries is finalised in its current form, several malpractices could be curbed. First-year commission cap on retail regular premium policies could be lowered from 35 percent to 20 percent.

Complaints abound of intermediaries pushing unsuitable life insurance products to individuals – for instance, unit-linked insurance policies (Ulips) and long-tenure traditional endowment policies to senior citizens. This, without informing them that their advanced age could eat into potential returns.

Moreover, many agents have a penchant for getting customers to churn policies in the initial years in order to earn higher first-year commissions, which ensured that policyholders shelled out steep surrender charges.

Advantage policyholders?

Now, in its draft paper on ‘Payment of commission or remuneration or reward to insurance agents and insurance intermediaries’ released on August 23, the regulator has proposed changing the commission structure. The proposals include more stringent ceilings on commissions that can be paid to life and general insurance intermediaries.

“This is a reform that was long overdue… The commission rates are too high, especially in the first year. This commission pay-out structure encourages agents to churn life insurance policies because commissions are bunched in the first year,” said Monika Halan, adjunct professor at the National Institute of Securities Markets (NISM). “The policyholder stands to lose when she surrenders her policies in the initial years. So, increasing the commissions in subsequent years – akin to trail commissions – is a move towards efficient rationalisation of commissions.”

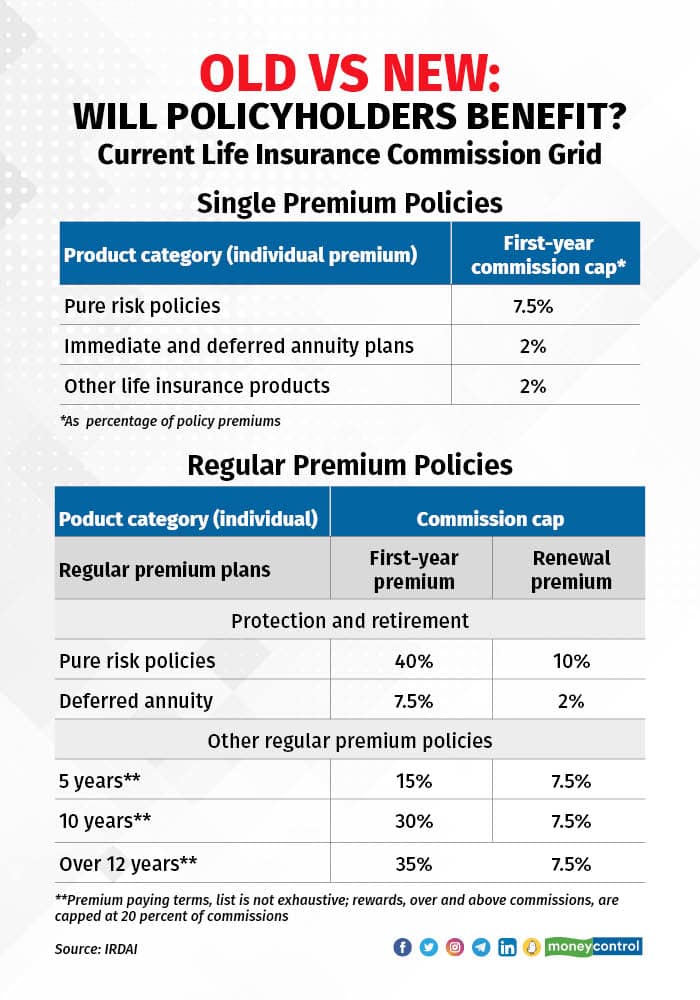

As per the IRDAI draft, commission on renewal premiums for regular premium life insurance policies other than pure risk products could go up from 7.5 percent to 10 percent, besides additional commission flow beyond the fifth year.

Maximum impact

“Most life insurance companies will have to pay lower commissions to their intermediaries if these norms are finalised,” the CEO of a private life insurance company said on condition of anonymity. “The commission pay-out structure of these companies will have to undergo a complete revamp.”

This is because the regulator has proposed a cap of 20 percent of the first-year premium for life insurers whose expenses of management (EoM) in the previous financial year exceed 70 percent of the permitted limits. Most life insurers would be in this category. EoM for life insurers include administration costs, commissions, remuneration or brokerage, and rewards to agents.

The regulator has outlined the maximum commission that can be paid to intermediaries. The ceilings also cover rewards paid, which is not the case currently.

Companies that do not breach the EoM parameter will be free to pay commissions as per their board-approved policies, giving them an edge over others from the policy sales perspective.

However, according to Emkay Global, the move won’t affect life insurers adversely, as all listed private life insurers, in practice, have been paying less than 20 percent commission on an overall portfolio basis.

“All in all, the EoM and commission payment changes prescribed in the draft regulations are far from being a negative surprise for existing listed private players, but the first-year commission cap could compel LIC to make some adjustments,” the broking firm said in a report.

Policyholders to benefit

For policyholders, this could be a positive step, though it remains to be seen whether lower commissions translate into cheaper premiums across product categories.

“This move will be positive in the long run, bringing down commission on the life insurance side. Over a period of time, the lower commissions will be passed on as benefits to policyholders in the form of reduced premiums,” said Susheel Tejuja, managing director of PolicyBoss.com. At present, commission limits are linked to product categories too.

“If the draft is finalised, life insurers will have to adhere to the cap on commissions on a portfolio-basis instead. With the overall cap, they will have the freedom to pay higher commissions for, say, traditional endowment plans and lower for Ulips, for example,” Tejuja said.

General insurance

If IRDAI’s proposals go through, general insurance companies will not be able to pay commissions, remuneration or rewards exceeding 20 percent of their gross written premium (GWP) in India in that financial year.Gross premium is the sum of premium earned through policyholders and any reinsurance premium, minus taxes paid. The same applies to standalone health insurance companies.

“In all, the regulations are a refinement of the existing regulations and in the right direction, as the industry turns incrementally mature. The draft regulations aim to reduce and merge the large number of expense and commission limits based on product segment and company’s age to a much simpler & lesser number of overall limits,” Emkay Global said in the report.