Who's Buying Medical Properties Trust Stock?

Summary

- Clearly, frustrations are mounting for Medical Properties Trust, as the share price has dropped by over 22% year-to-date.

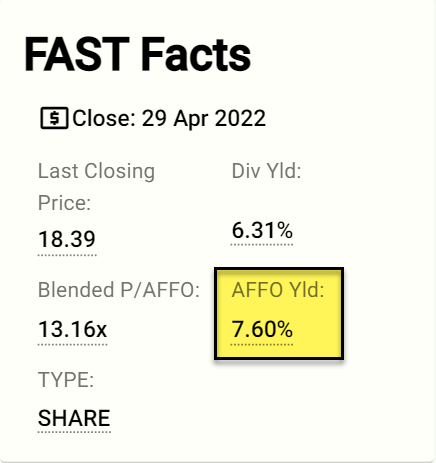

- With an equity multiple of 7.6%, it’s difficult for MPW to invest in new healthcare properties. So, it must resort to other methods.

- MPW is now yielding 6.3%, and our price target is $27.00 per share… which translates into a total return forecast of 45%.

- I do much more than just articles at iREIT on Alpha: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

akinbostanci/iStock via Getty Images

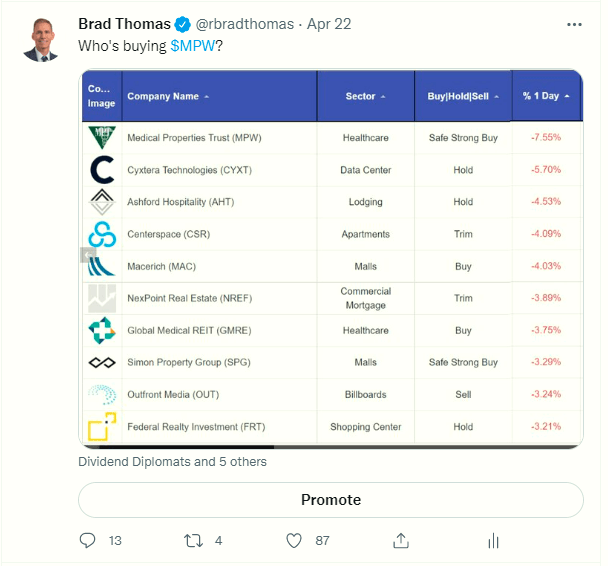

A few days ago, before Medical Properties Trust, Inc (NYSE:MPW) announced Q1-22 earnings, I posted this on Twitter:

(Source: @rbradthomas)

That same day, shares slid by over 7%. And, as you can see below, shares are down by around 8% since April 22.

(Source: Yahoo Finance)

On Thursday, April 28, MPW announced its Q1-22 earnings. And during its conference call, CEO Edward Aldag explained (emphasis added):

“In my overall remarks today, I will also take time to address a few other points that have been raised in recent reports and media coverage about [us]. While we typically don't respond to the various third-party reports of this nature and some of this information may seem like real estate one-on-one, we have heard from many of you, our shareholders, and others that we should take the opportunity to set the record straight and correct some of the erroneous information that has been published.” (Emphasis added.)

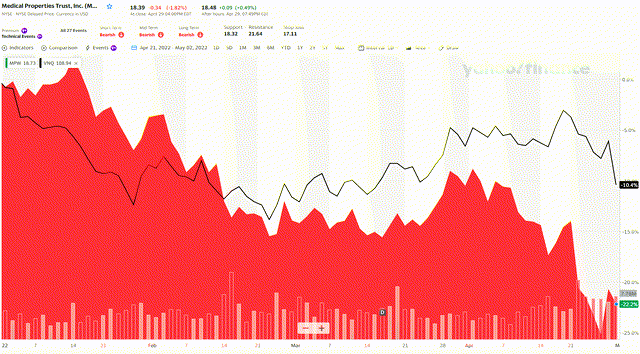

Clearly, frustrations are mounting for MPW. That much is obvious, based on how shares have dropped over 22% year-to-date. Whereas, the Vanguard Real Estate Index Fund (VNQ) is only down 10%.

(Source: Yahoo Finance)

MPW Isn’t Stacking Up (At Least In This Regard)

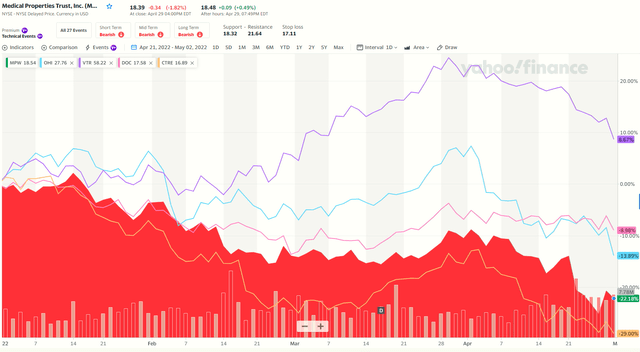

Most of MPW’s peers have outperformed it, except for CareTrust REIT (CTRE), as seen below:

(Yahoo Finance)

One of MPW’s most notable challenges is to grow its business by utilizing its cheapest forms of capital. And, of course, common equity is not one of them.

(FAST Graphs)

With an equity multiple of 7.6%, it’s difficult for MPW to invest in new healthcare properties. As such, it must resort to other methods. Consider what CFO R. Steven Hamner said about his company:

“… we have estimated a range of accretive acquisitions in 2022 of between $1 billion and $3 billion. We are confident the investment opportunities are there. But the ultimate volume this year will be related to the amount and timing of our access to attractively priced equity capital.” (Emphasis added.)

It’s also important to note how management doesn’t like its current equity pricing. It made that clear on the call. This dynamic could cause MPW to acquire only a portion of the $4 billion to $5 billion of opportunities it otherwise could.

As it is, to help finance current acquisition expectations, the company must sell assets and various joint ventures. Fortunately, MPW has a good history of using JVs – including the recent 50% stake it sold in a $1.7 billion Steward portfolio to Macquarie Asset Management. (Incidentally, Steward is still its largest tenant.)

It’s also provided us with some new transparency in hopes of clearing up some of the “erroneous information” out there. Needless to say, this could help it return to its previous valuation level.

In which case, it would issue equity to generate attractive investment spreads. The kind of numbers we’d be happy to be part of.

Medical Properties Trust's Management Provides Some Clarity

On last week’s earnings call, Medical Properties Trust defended claims regarding straight-line rent write-offs and Centers for Medicare and Medicaid Services ("CMS") coverage ratio comparisons.

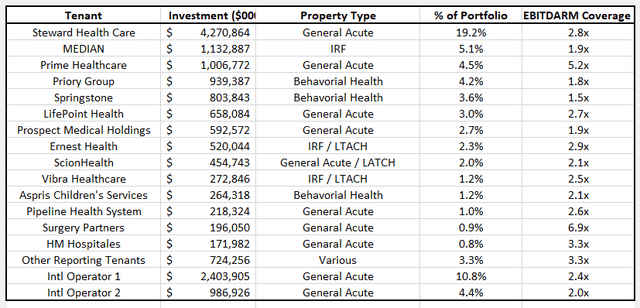

Detailed tenant disclosures are important for investors to be able to look over. And I’ve often challenged MPW to provide more transparency in that regard. So, I’m happy to see it offer details about its top five.

This new color on key operators should be very helpful for analysts and investors – especially given the fact that most all its tenants are citing some signs of improvement. For example:

- Steward’s reported coverage was 2.8x

- Median was 1.9x

- Prime was 5.2x

- Priory was 1.8x

- Springstone was 1.5x.

Aldag explained on the Q1-22 earnings call (emphasis added):

“First, let me point out as I have numerous times, EBITDARM [earnings before interest, taxes, depreciation, amortization, rent, and management fees] in these calculations come straight from property level GAAP basis financial reports we received from our tenants, which include their annual audited financials at year-end.

“Except an extremely rare or unusual circumstances such as the COVID grants for 2020 and 2021, and some minor immaterial prior period updates, no adjustments have been made to these numbers.

“These EBITDARM numbers are trailing 12 months for the period ending 12/31/21. We use earnings before interest, depreciation, amortization, rent and management fees, and the actual cash rent amounts owed to [MPW].” (Emphasis added.)

That’s worth exploring more, so let’s do precisely that…

More From The MPW’s Mouth

Aldag also added (emphasis added):

“There have been a couple of recent reports from third parties outside of the company that have tried to use CMS cost report NOI [net operating income] numbers to show profit margins and equate that to a lease coverage comparison. CMS uses different definitions and allows different deductions for items such as depreciation, amortization, interest, and other items than what is required in GAAP financial statements.

“Furthermore, they include all rental and lease payments and interest payments among other items. Therefore, when quoting the profit margins, one must keep in mind that all [MPW] rent and other rent and interest has already been accounted for in those numbers. By definition, the CMS cost reports could actually show a negative profit margin and all of the rent and interest being paid at the same time.”

This comment is specifically related to a short report where an analyst used CMS-reported NOI to make lease coverage comparisons.

However, as Aldag pointed out, CMS uses different definitions to calculate such ratios. So the cost it reports imply negative profit margins for all operators… which is negated by EBITDARM coverage ratios.

(iREIT on Alpha)

In regard to Steward, which amounts to 19.2% of its total portfolio, MPW explained:

“Steward has kept coverage ratios at or above the industry standard and has remained flat close to an almost 3x coverage for the past three quarters. One item of note is that the recent acquisitions in the Miami region continue to far exceed our original expectations.

“And just as a reminder, the HCA Utah transaction is projected to close by the end of the second quarter of this year. Notwithstanding the value we have generated from Steward being one of our tenants, Steward accounts for an increasingly smaller portion of our portfolio as we continue to invest domestically and internationally in non-Steward hospitals.”

Notably, salary wages and contract labor are also well below budget. And utility/food costs have not experienced hugely incremental impact from inflationary pressures.

Medical Properties Trust Q1 Earnings Results

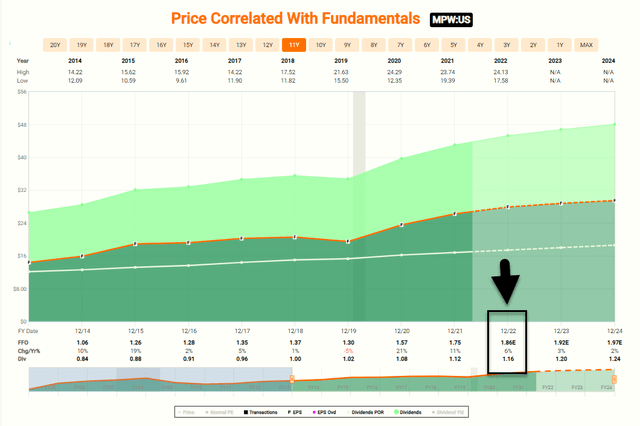

For Q1-22, MPW generated normalized funds from operations (FFO) of $0.47 per diluted share. Meanwhile, full-year 2022 guidance was $1.78-$1.82 per share.

The hospital REIT changed how it presents FFO guidance to provide more transparency over its acquisition pipeline. As noted, it’s providing an investment volume of $1 billion to $3 billion in 2022…

Or $4 billion to $5 billion if it can improve its equity cost of capital.

(FAST Graphs)

That’s part of why MPW’s cost of capital is considered at risk and why shares have pulled back. And then the “erroneous information” published has put more pressure on shares still.

But that’s just created a better buying opportunity for you and me.

In Conclusion…

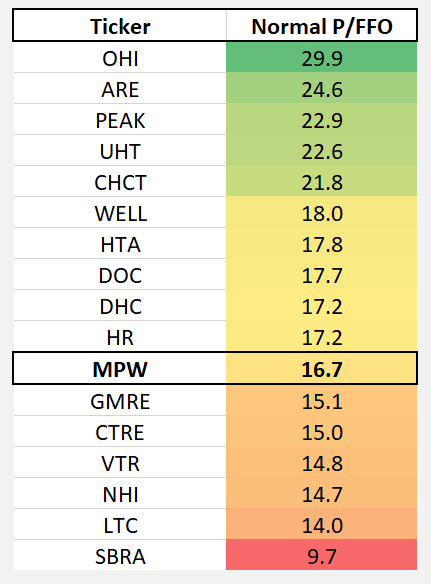

We all know valuation is more of an art. But as a REIT scientist, I like to utilize all available data and resources anyway.

Let’s start with MPW and its healthcare peers’ p/FFO:

(Source: iREIT on Alpha)

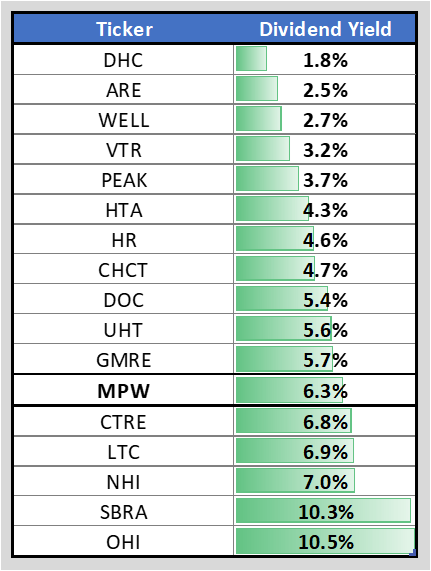

And their dividend yields:

(Source: iREIT On Alpha)

We’ve been following MPW for around a decade. So I must credit management for its underwriting acumen.

It always maintains discipline to drive strong FFO performance, despite industry pressures.

Plus, labor issues seem to be improving for MPW’s tenants. And even if they don’t this quarter, MPW says its operators should withstand the pressure until CMS adjusts Medicare rates to sufficiently offset inflation.

(Their current portfolio EBITDARM rent coverage ratio is 2.7x.)

Yes, the next set of quarterly coverage ratios could be down slightly thanks to labor pressures January-February. But MPW’s tenants collectively saw signs of improvement in March-April.

That’s why I want to thank all that “erroneous information.” It has allowed me to buy more shares on the cheap.

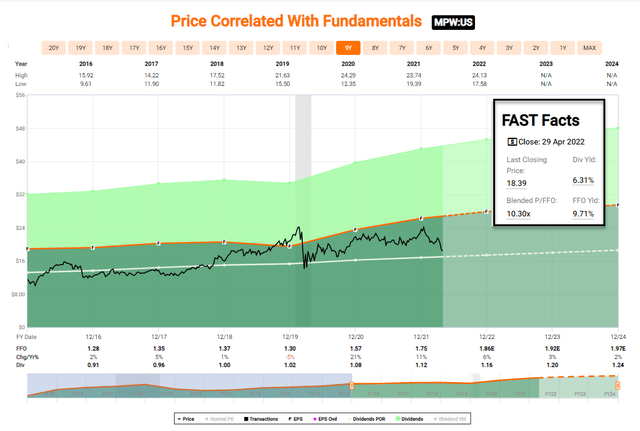

(Source: FAST Graphs)

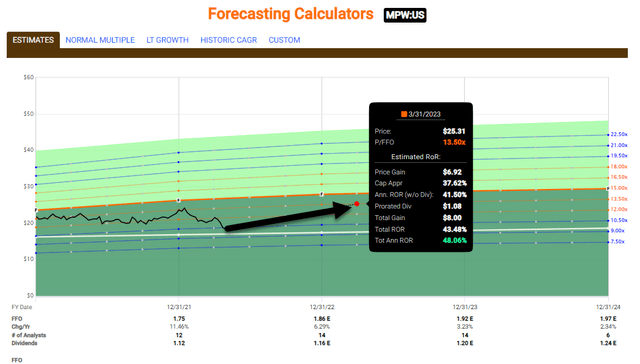

Shares now yield 6.3%, and our price target is $27… which translates into a total 12-month return forecast of 45%.

(Source: FAST Graphs)

We just loaded up the truck.... beep beep... Thank you, Mr. Market!!!

Get My New Book For Free!

Join iREIT on Alpha today to get the most in-depth research that includes REITs, mREIT, Preferreds, BDCs, MLPs, ETFs, and we recently added Prop Tech SPACs to the lineup. We are also adding an all-new NAV tool this week called NAV-igate to help members screen for value. Nothing to lose with our FREE 2-week trial.

And this offer includes a 2-Week FREE TRIAL plus my FREE book.

This article was written by

Brad Thomas is the CEO of Wide Moat Research ("WMR"), a subscription-based publisher of financial information, serving over 6,000 investors around the world. WMR has a team of experienced multi-disciplined analysts covering all dividend categories, including REITs, MLPs, BDCs, and traditional C-Corps.

The WMR brands include: (1) The Intelligent REIT Investor (newsletter), (2) The Intelligent Dividend Investor (newsletter), (3) iREIT on Alpha (Seeking Alpha), and (4) The Dividend Kings (Seeking Alpha). Thomas is also the editor of The Forbes Real Estate Investor and the Property Chronicle North America.

Thomas has also been featured in Forbes Magazine, Kiplinger’s, US News & World Report, Money, NPR, Institutional Investor, GlobeStreet, CNN, Newsmax, and Fox. He is the #1 contributing analyst on Seeking Alpha in 2014, 2015, 2016, 2017, 2018, and 2019 (based on page views) and has over 96,000 followers (on Seeking Alpha). Thomas is also the author of The Intelligent REIT Investor Guide (Wiley).

Thomas received a Bachelor of Science degree in Business/Economics from Presbyterian College and he is married with 5 wonderful kids. He has over 30 years of real estate investing experience and is one of the most prolific writers on Seeking Alpha (2,800+ articles since 2010). To learn more about Brad visit HERE.Disclosure: I/we have a beneficial long position in the shares of CTRE, MPW either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Author's note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: written and distributed only to assist in research while providing a forum for second-level thinking.