VICI Properties: The First Line Of Defense Against Volatile Markets

Summary

- VICI shares remained resilient against market selloff, demonstrating a loyal shareholder base and a renewed interest in alternative assets from institutional investors.

- The MGP acquisition diversified its tenant base, but revenue is still limited to the gaming industry, sensitive to economic cycles.

- Investors should expect a stable dividend and a slight increase in share value, mirroring rising real estate prices.

- Most of VICI debt is tied to fixed-rate notes, protecting it from rising interest rates, at least in the short run.

RandyAndy101/iStock Editorial via Getty Images

Investment Thesis

VICI Properties (VICI) shares remained resilient in the face of the market selloff. The previous article highlighted why investors should expect capital gains augmenting its 5% dividend. Since then, shares rose 5.2%, bringing a total return to 6.6%, against an 8% decline in the broader market.

Multiple factors support the company's valuation, including a renewed interest in properties as an alternative asset class as institutional investors realize the importance of properties as a diversification instrument. This idea proved its worth during the market selloff.

Investors might benefit from adding a high-yielding dividend stock such as VICI as a source of stable income, supported by long-term, triple net lease contracts. Nonetheless, one should note that although this dividend is a defensive income source, it is not immune to a recession.

Revenue Trends

During the pandemic, VICI collected 100% of the rent from its tenants. This doesn't say about its occupants as much as the importance of the service it provides. Paying rent is a priority for any business. Its largest two customers, Caesars Entertainment (CZR) and MGM Resorts, have a history of bankruptcy.

Still, as public companies, its tenants have access to the capital market, creating a safety net or a cushion if they fall under. There are other lines of defense put in place to protect VICI. It is industry practice to collect rent in advance and multiple months of deposit against any unpaid rent.

The concept of a gaming REIT is new, and today, there are only two such trusts among the 1,100 REITs registered with the IRS and the 225 registered with the SEC. As prospects of a recession increase, we find it challenging to assess the dynamics of a recession in the gaming REIT sector, especially given the revenue concentration, making it hard to diss a tenant, giving them bargaining power. I imagine a scenario where CZR or MGM asks for a deferral of rent on some properties during a recession. VICI management will find it hard to say no to a customer representing more than 40% of its revenue.

Yesterday, VICI closed the MGM Growth Properties (MGP) deal, which slightly increased tenant diversity, but still, its largest two tenants represent a significant portion of revenue, as shown below.

VICI Properties

VICI owns one of the most iconic properties in the world, located in some of the most sought-after commercial zones with the highest sale per square foot rates globally. One can argue that when push comes to shove, VICI will find helping hands from the states and municipalities interested in gaming tax dollars to find new tenants. These dynamics offset risks inherent from the lack of alternative uses of gaming properties. In my view, VICI shareholders will enormously benefit if management diversifies outside the gaming sector.

Financial Position

From my understanding, VICI funded the MGP acquisition through $11 billion of debt, and ~200 million in new shares, bringing the total value of the acquisition to $17 billion. The deal significantly alters VICI's financial position, tripling debt and increasing the number of shares outstanding by 26%. Investors should expect a $1 billion increase in revenue, representing a 66% jump from TTM sales of $1.5 billion before the acquisition.

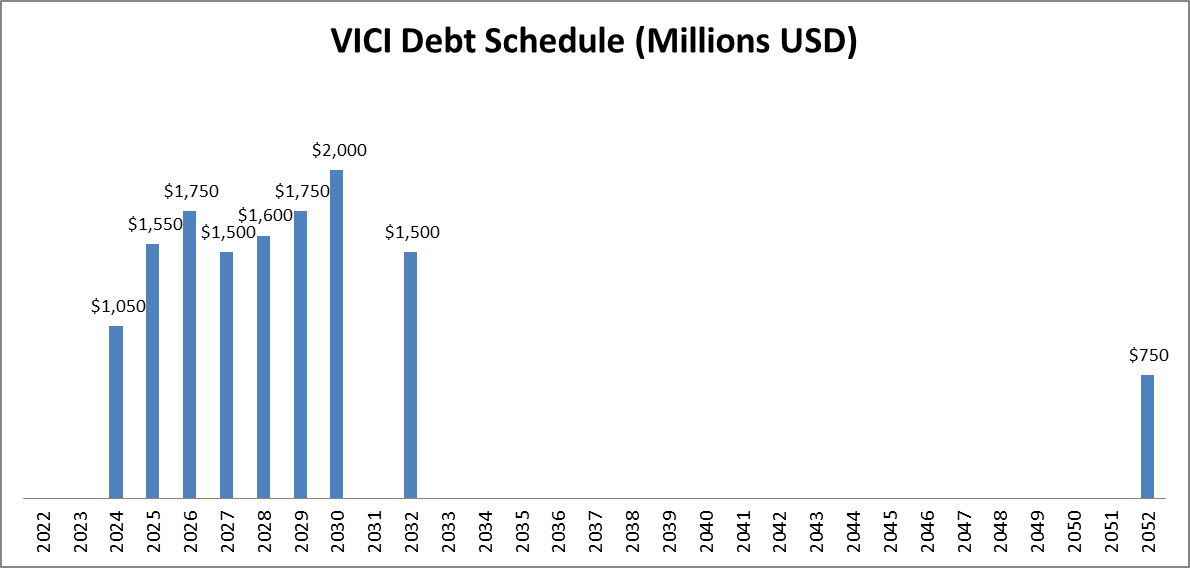

What comes to mind is the effect of rising interest rates on the company. Most of VICI's term debt is fixed-rate notes, protecting it from rising interest rates until maturity. Below is the proforma maturity schedule of VICI's debt after the MGP tender.

VICI Properties, Morningstar

VICI doesn't need to worry about rising interest rates until 2024 when it will need to refinance the $1.05 billion debt it inherited from MGP. At that time, it will most likely face a steeper borrowing cost than it did MGP issued these notes a few years ago. These dynamics are mirrored in the depreciating prices of VICI's notes it held before the acquisition, pushing effective yields higher as the Fed tightens monetary policy. For example, the price of its 4.25% notes maturing 2026 fell from $104 to 95, raising the effective yield to 5.5%.

The company's leases contain CPI escalators. However, the benefits are limited by the rent contracts setting limits on these escalators. For example, in some lease contracts, the total rent increase can't exceed 3%, compared to the current level of inflation, equal to 8.5%. At the same time, the company also has minimum rent growth, set at 2%.

All-in-all, I believe VICI enjoys a solid financial position. The company recently gained a credit rating upgrade from Moody's to Ba1, one notch below investment grade. Diversification beyond gaming property will help reduce the risk inherent in the industry's cyclicality.

Summary

I believe that the current market selloff validates institutional investors' move towards real estate as an alternative asset class to diversify portfolios and reduce risk. Companies such as Blackstone (BX) have been expanding their portfolio to meet institutional investors' demand for properties as diversification tools. These dynamics as mirrored VICI's resilience in recent weeks.

Despite scaling debt, VICI's financial position remains solid. A substantial increase in revenue accompanies the rise in debt. Added benefits of diversification contributed to Moody's decision to upgrade the company's ratings.

VICI owns some of the most iconic real estate in the world. Its property portfolio offers investors an inflation hedge, augmenting its 5% dividend yield.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of VICI either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.