InPlay Oil: The Price Is Still In Play For Market-Beating Returns

Summary

- This stock priced for up to 100% returns.

- With the ample free cash flow and low leverage I expect dividends or share buybacks in the near term.

- IPO has among the lowest Finding, Development & Acquisition Costs (FDA) per barrel and among the highest recycle ratios among its peer group.

Thinkhubstudio/iStock via Getty Images

We shall refer to InPlay Oil Corp as InPlay herein. All figures in CAD unless otherwise noted.

Introduction

I have written on this "deep value" investment that is InPlay Oil Corp. (OTCQX:IPOOF) a couple times in the past, most recently in August 2021. As you may recall I had stated:

Everything about this investment screams "cheap" which is a rarity in today's market. InPlay's debt reduction strategy and assets make this a low downside/high upside investment. Even if there is an adverse fall in commodity prices in the near term, I don't think this company is going away. It is very rare indeed that we see even a junior E&P company trading at a discount to NAV using only 2P reserves and using very conservative strip pricing. Using 3P reserves for NAV would imply an outrageous 65% discount to NAV meaning the stock has ~300% upside.

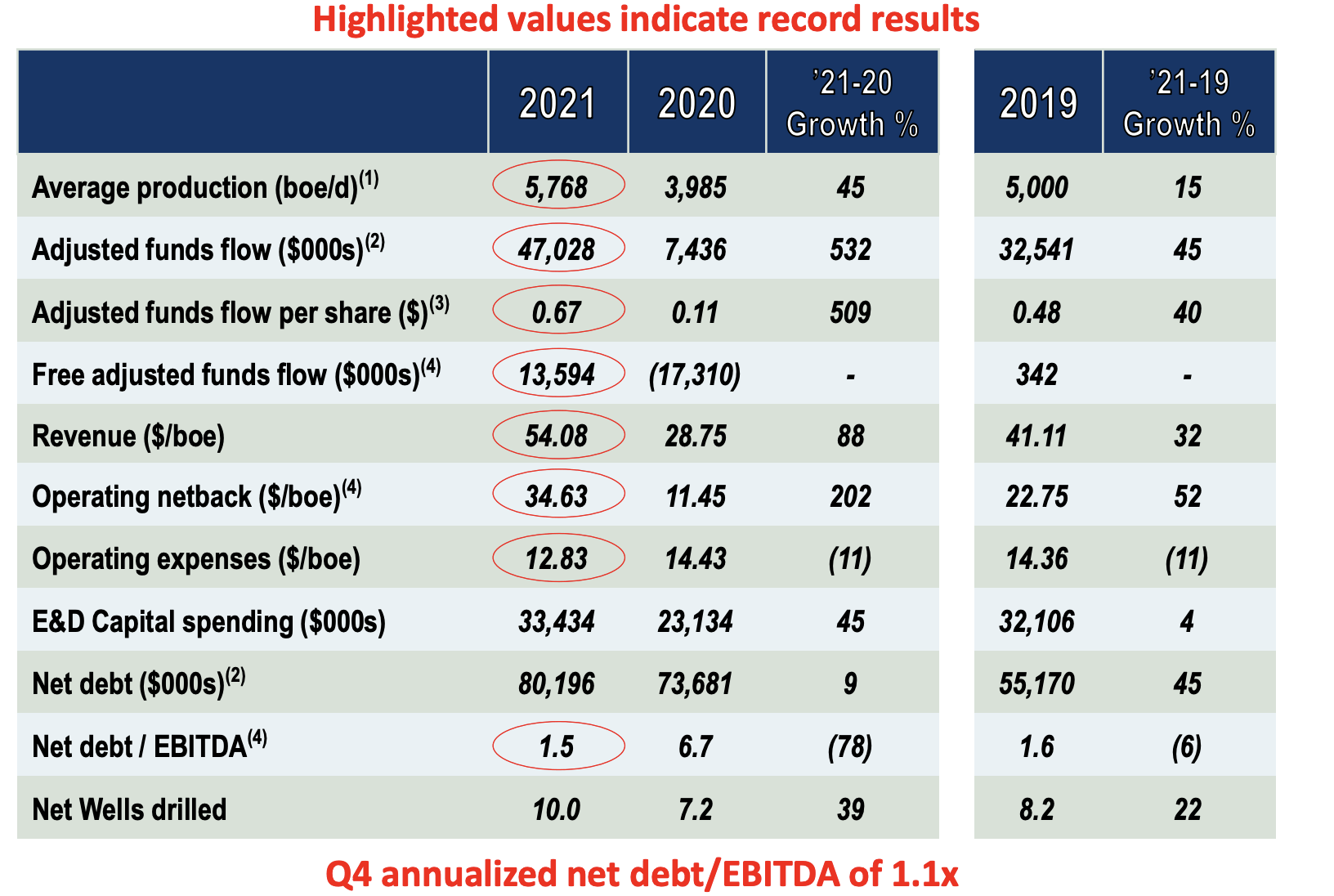

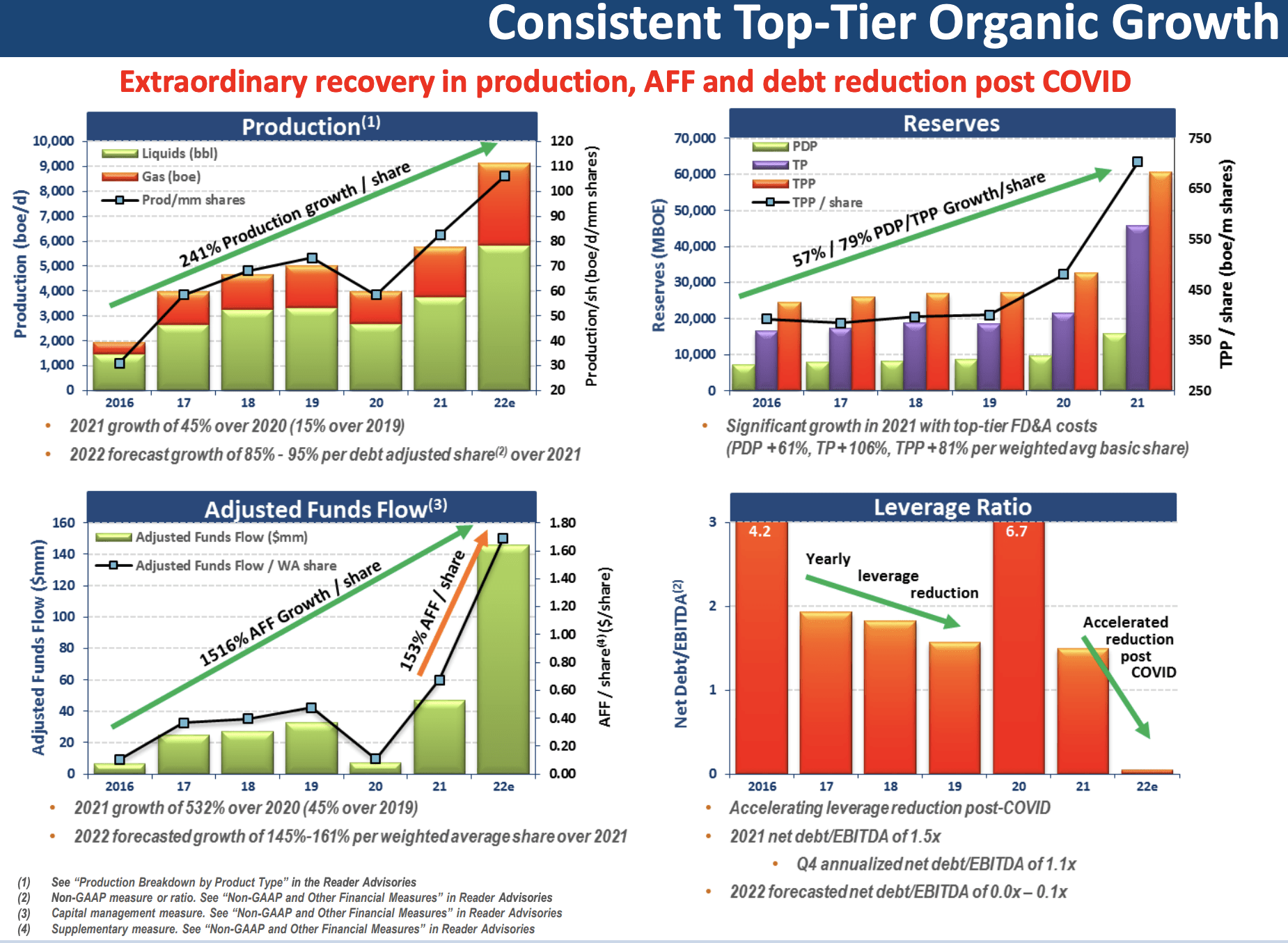

There is perhaps no company that has benefited more from rising oil prices than InPlay as rising commodity prices combined with a record year in production led to its highest profitability in its history at $13.6MM or $0.67/share. InPlay was able to increase production 45% from the previous year while only increasing net debt 9% (only 21% of CAPEX was financed), leading to a massive drop in leverage YoY from 6.7x to 1.5x using Net Debt/EBITDA.

2022 Forecast (InPlay Oil) 2022 Forecast (InPlay Oil)

On November 30, 2021 InPlay completed the acquisition of all of the issued and outstanding Prairie Storm shares pursuant to the PS Arrangement. Under the PS Arrangement, the holders of Prairie Storm shares received $0.2514 in cash and 0.0524 of an InPlay Share for each Prairie Storm share held, resulting in the payment of an aggregate of $39.9 million in cash and the issuance of an aggregate of 8,320,335 InPlay shares to the former holders of Prairie Storm shares. This led to 50% and 125% YoY increases in proved developed (PDP) and total proved reserves (TP). InPlay has confirmed production will increase to 8,900-9,400 boe/d from fiscal 2021 which is a 54% YoY increase.

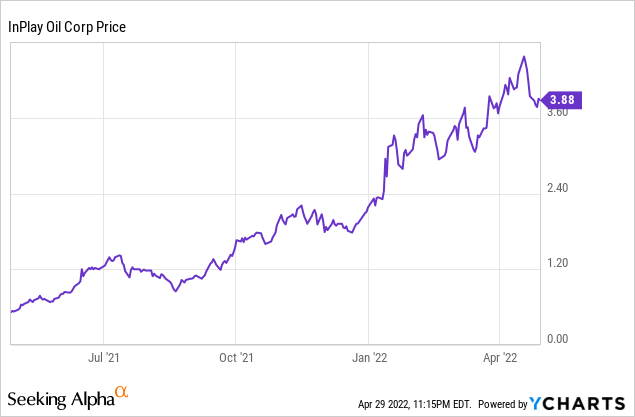

InPlay's impressive results have resulted in massive returns to shareholders (more than 200% since August 2021). Although the price has pulled back in recent weeks as it reached a high of $4.50/share in mid-April but has likely fallen as a result of a pullback in oil prices. Despite these large gains the party is not over as the company still has the potential to make major returns to shareholders.

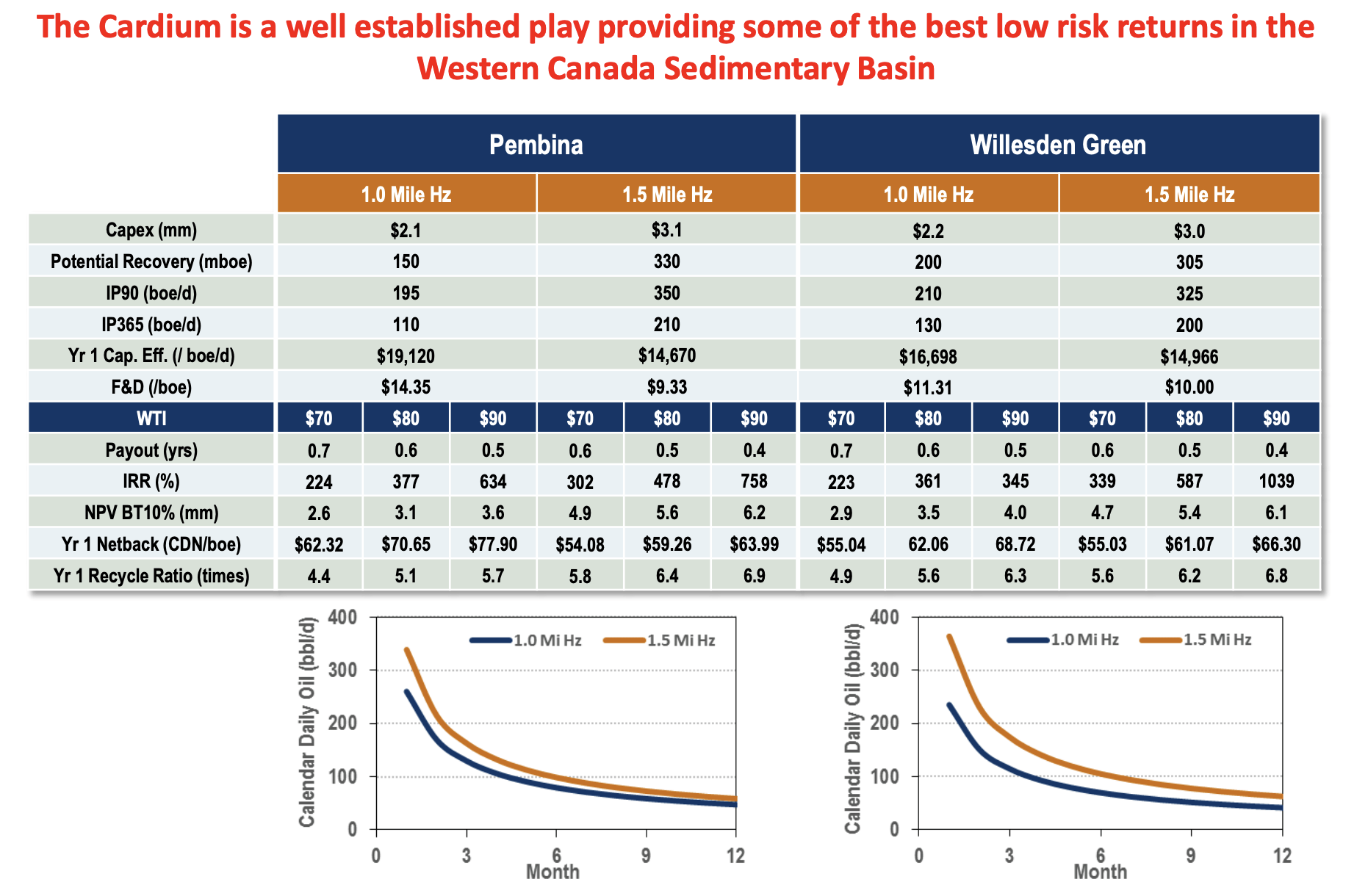

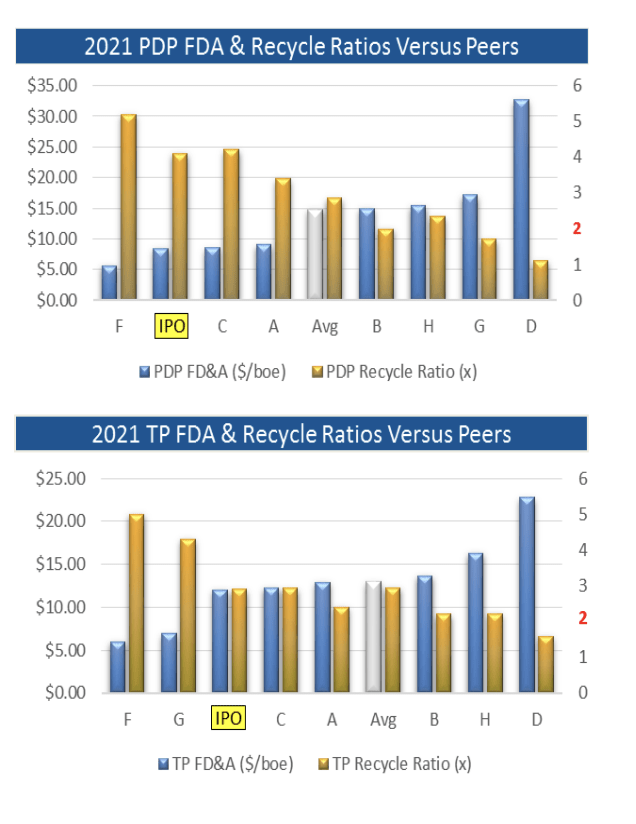

InPlay's cardium assets require more CAPEX to develop than traditional plays, but the higher initial production from these wells results in very low payback periods (less than 6 months at today's prices) and very high IRR at more than 480%. In fact, InPlay has among the lowest Finding, Development & Acquisition Costs (FDA) costs per barrel and among the highest recycle ratios at 2x (Recycle Ratio: $1 capital invested returns $x) among its peer group.

The surprising this is in spite of this InPlay only trades in the middle of the pack of its peer group.

Investment Thesis

2022 Forecast (InPlay Oil) 2022 Forecast (InPlay Oil)

The EIA has made the following forecasts:

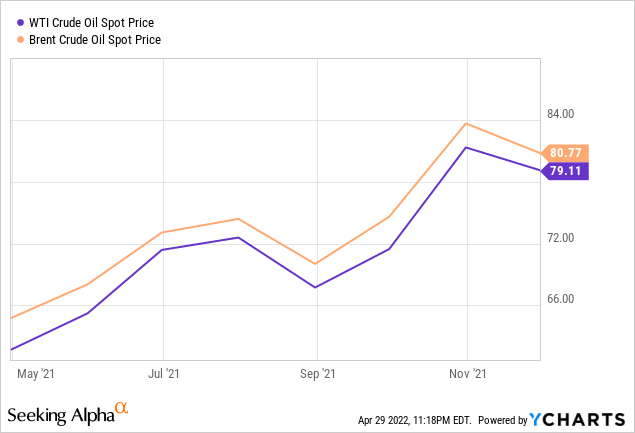

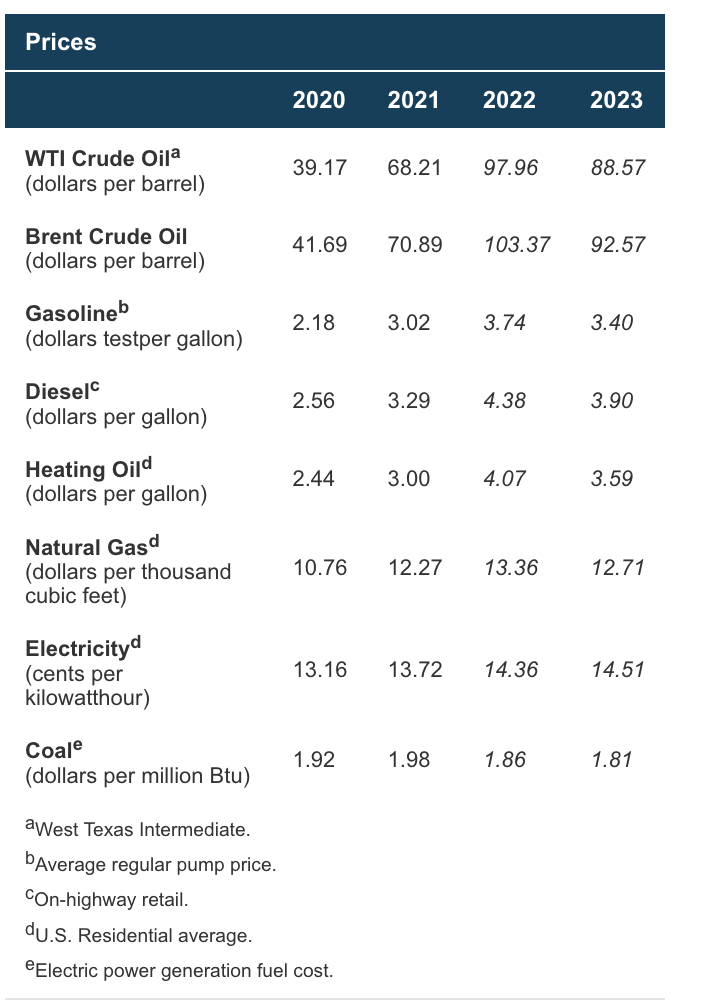

The Brent crude oil spot price averaged $117/bbl in March, a $20/b increase from February. Crude oil prices increased following the further invasion of Ukraine by Russia. Sanctions on Russia and other actions contributed to falling oil production in Russia and created significant market uncertainties about the potential for further oil supply disruptions. These events occurred against a backdrop of low oil inventories and persistent upward oil price pressures. Global oil inventory draws averaged 1.7 million barrels per day (b/d) from the third quarter of 2020 (3Q20) through the end of 2021. We estimate that commercial oil inventories in the OECD ended 1Q22 at 2.61 billion barrels, up slightly from February, which was the lowest level since April 2014.

We expect the Brent price will average $108/b in 2Q22 and $102/b in the second half of 2022 (2H22). We expect the average price to fall to $93/b in 2023. However, this price forecast is highly uncertain. Actual price outcomes will depend on the degree to which existing sanctions imposed on Russia, any potential future sanctions, and independent corporate actions affect Russia's oil production or the sale of Russia's oil in the global market. In addition, the degree to which other oil producers respond to current oil prices, as well as the effects macroeconomic developments might have on global oil demand, will be important for oil price formation in the coming months. Although we reduced Russia's oil production in our forecast, we still expect that global oil inventories will build at an average rate of 0.5 million b/d from 2Q22 through the end of 2023, which we expect will put downward pressure on crude oil prices. However, if production disruptions-in Russia or elsewhere-are more than we forecast, the resulting crude oil prices would be higher than our current forecast.

SHORT-TERM ENERGY OUTLOOK (www.eia.gov)

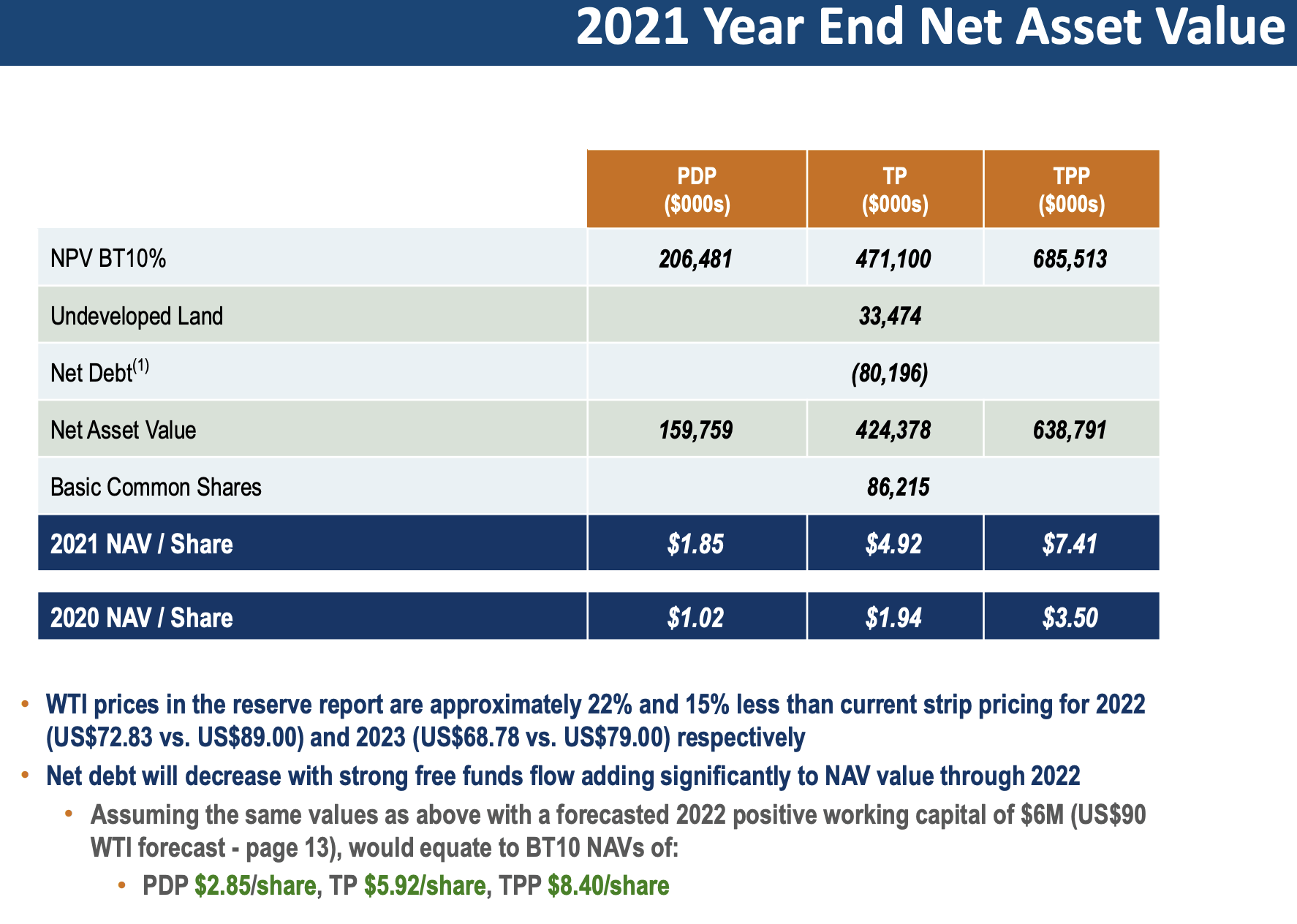

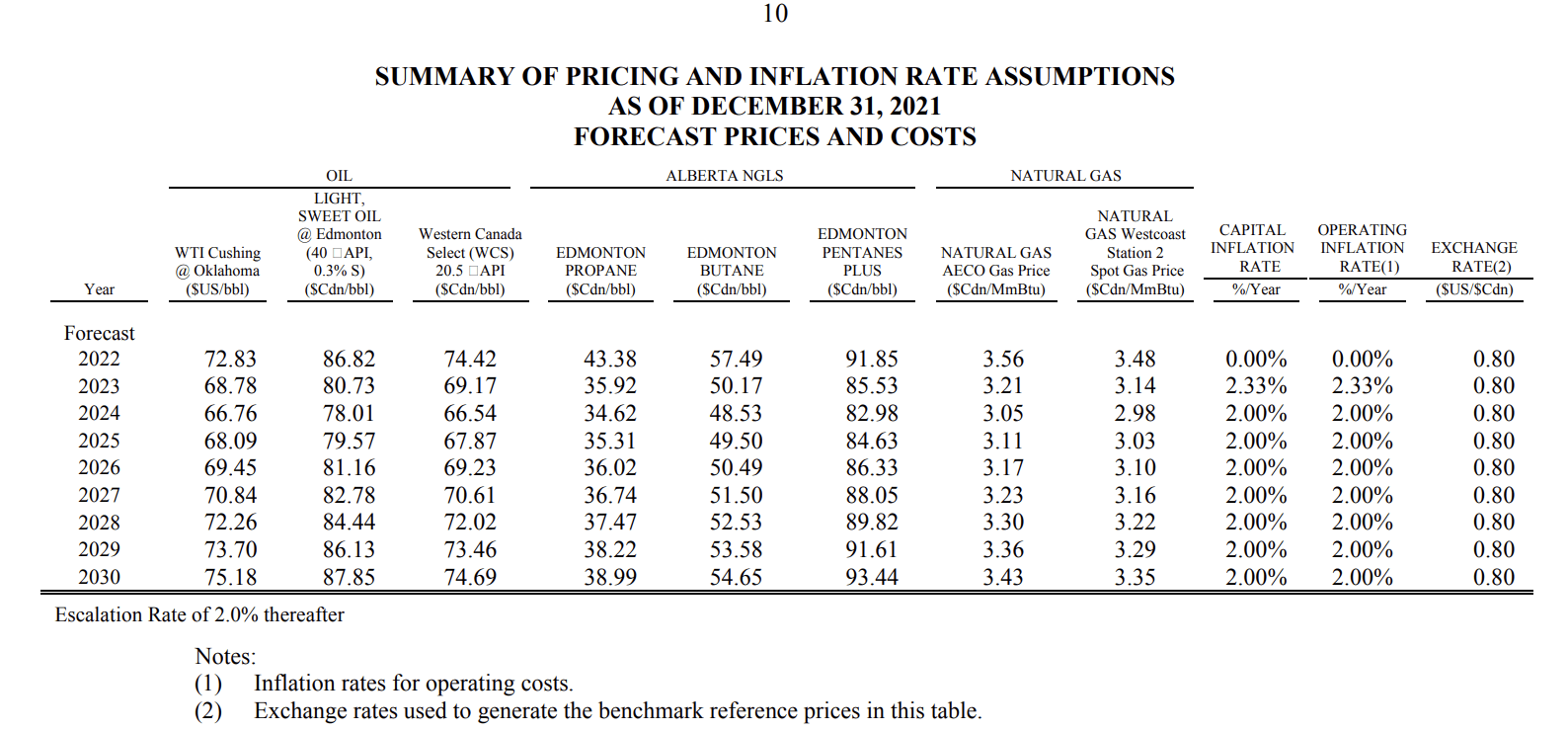

InPlay does boast a NAV of $4.92/share in their 2022 Forecast on their total proved (TP) reserves alone which is ~30% above its market price. This is theoretically the minimum price InPlay would receive if they were to monetize these reserves. These numbers do have to be taken with a small grain of salt as InPlay does tend to neglect G&A expense. That being said, it would seem that as an investor you are getting exposure to all probable reserves for the price of just the proved which implies as much as 100% upside. InPlay has also used fairly conservative pricing assumptions as per the 2021 Reserve Report as oil prices have been around $80/bbl USD for most of 2022 and they actually assume fairly stagnant pricing over the next 8 years around ~$70/bbl USD, even backward pricing until 2026.

2022 Forecast (InPlay Oil) 2021 Annual Information Form (Sedar)

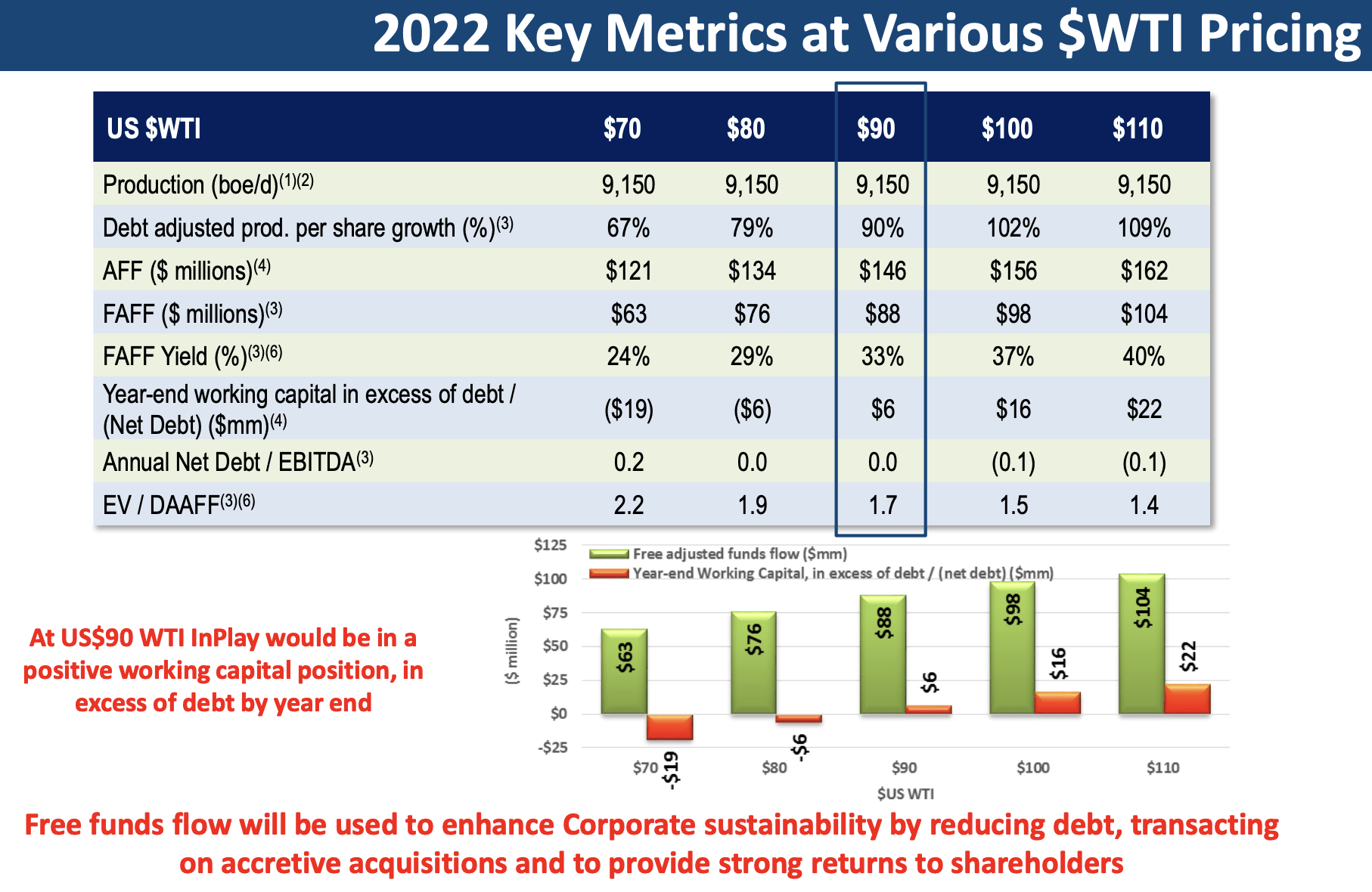

At even $80/bbl USD which is well below what has been forecasted by the EIA as per above, the free cash flow yield is extremely high at 23%.

2022 Forecast (InPlay Oil)

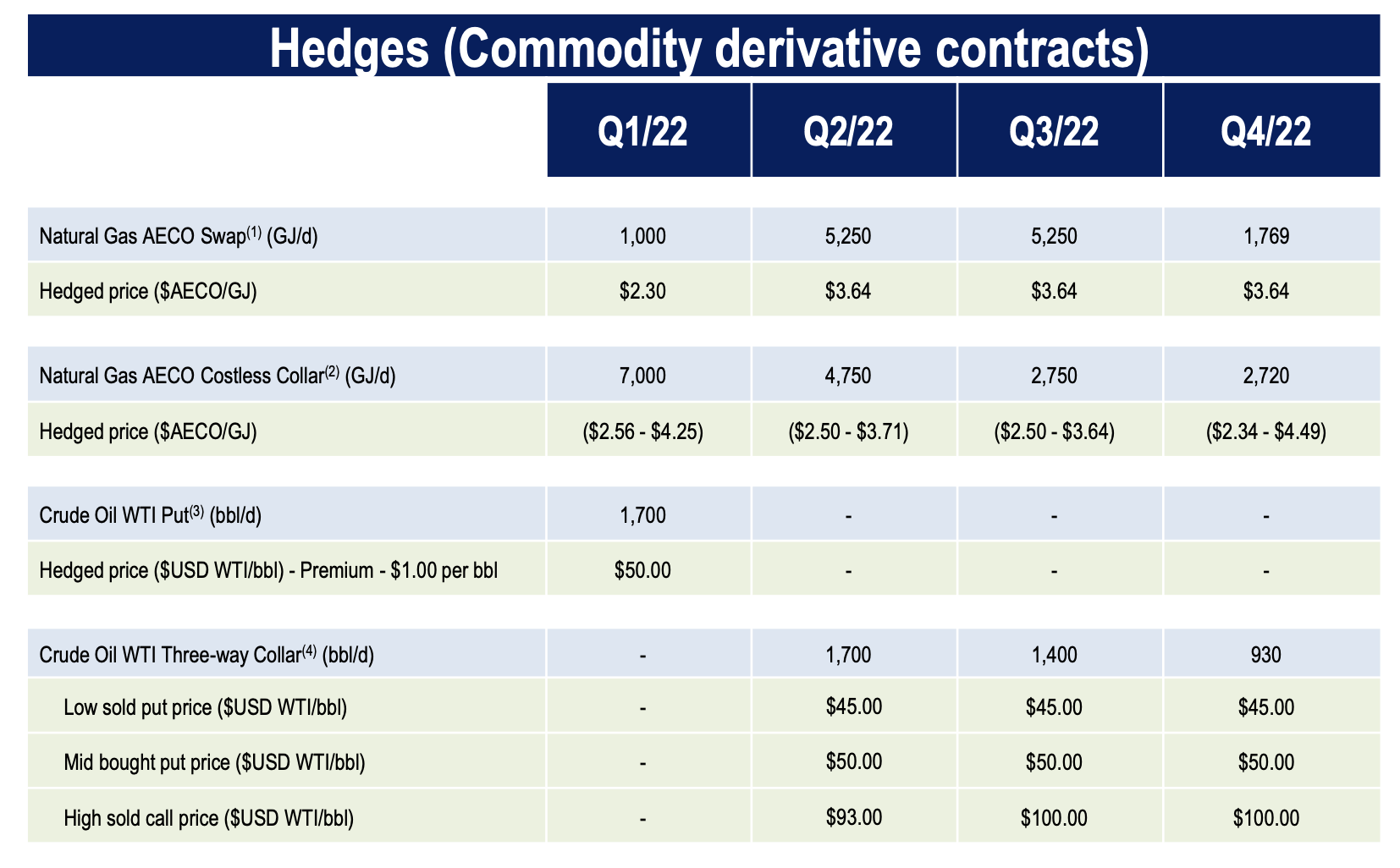

InPlay does tend to have an odd hedging program with the "three-way collar." That being said they typically hedge as much as ~20% on the downside at around $45-$50/bbl using puts but also sell puts at $45/bbl to recoup some of the premium paid. However, oil prices have not been that low in over a year now and almost outside the realm of possibilities as far as industry experts are concerned so therefore I am not concerning myself with those options that are likely to expire OTM. InPlay has however only capped their upside on less than 20% of production over the remainder of the year at fairly high prices ($93-$100/bbl) and therefore has plenty of room for NAV growth over the coming year.

2022 Forecast (InPlay Oil)

Risks to consider

Everything about InPlay screams "cheap", and with their low leverage position should remain in a sound financial position should there be a freak event that causes even a meteoric plunge in oil prices.

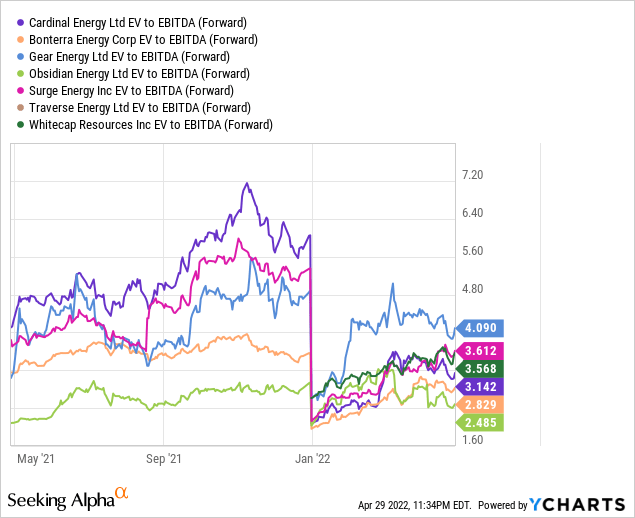

The analyst community agrees with this assertion, they believe InPlay trades at the cheapest valuation of its Canadian E&P peers relative to its 2022E debt adjusted cash flow, and even foresee its cash position overtaking its debt.

2022 Forecast (InPlay Oil)

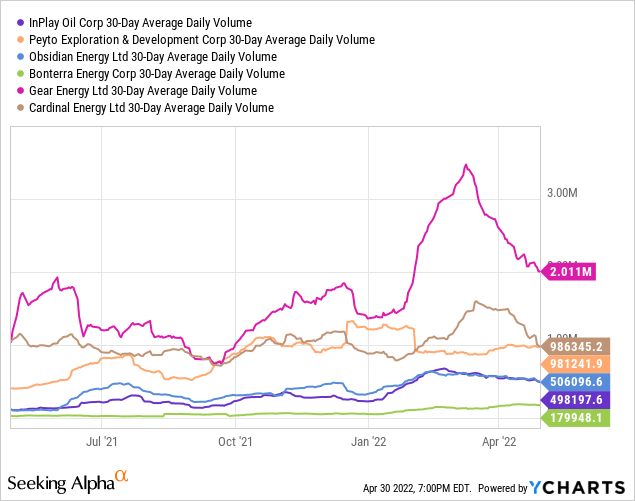

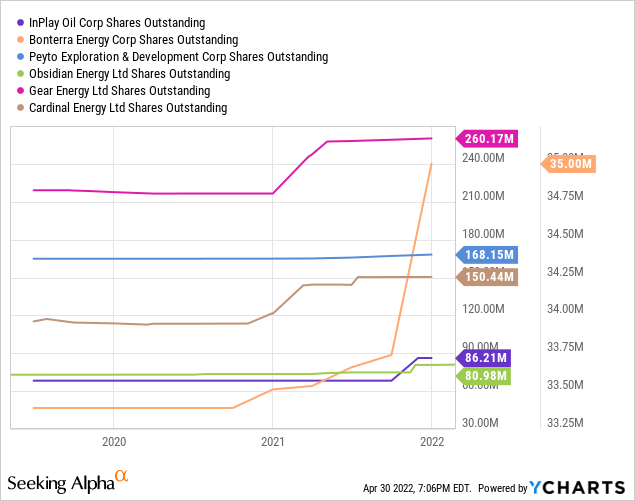

The main reason this stock is so "cheap" is its lack of liquidity which makes it unattractive for most institutional funds. Amongst other Canadian peers with market capitalizations less than $1 Billion it has amongst the lowest trading volumes and shares outstanding with only Bonterra Energy Corp. (OTCPK:BNEFF) and Obsidian Energy Ltd. (OBE) having comparatively low trading volumes and shares outstanding. According to Morningstar the top 20 small cap funds who do have any ownership make up less than 1% of its outstanding shares. That being said these stocks have a tendency to explode as institutional investors do take notice.

This stock is also not a fit for income investors as it has never paid a dividend. On October 30, 2020, InPlay entered into a term loan with the Business Development Bank of Canada under their Business Credit Availability Program (BCAP) which provided them with a non-revolving $25 million, second lien, four-year term loan facility to enhance liquidity. This facility is restrictive in that it will not allow payment of any dividends or even share buybacks without permission and are not permitted to use OLOC funds at all for these purposes. Given the expected free adjusted cash flow of $83-$92 Million for 2022 at $80/$90/bbl USD and as leverage falls, shareholder returns in the form of dividends and share buybacks should not too far away which will help close the discount to NAV.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of IPOOF either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.