More Chinese Developers Are Scrambling to Dodge Debt Defaults

(Bloomberg) -- One of China’s top 20 biggest developers is joining a host of others looking to delay bond payments to dodge defaults, after debt crises in the industry have effectively shut them out of the overseas financing market.

Yango Group Co. is seeking to extend three of its dollar notes as “existing internal resources may be insufficient,” according to a filing. The Shanghai-based builder, which ranked as the 18th biggest in the nation by contracted sales, intends for the move to improve liquidity and avoid default, it said.

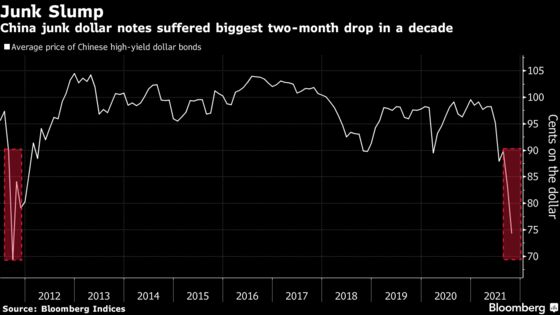

The company’s shares fell as much as 8.4% Monday in Shenzhen, hitting a seven-year low. Chinese dollar high-yield bonds are falling for an eighth-straight day Monday after tumbling nearly 9 cents on the dollar last month, closing out the worst two-month slide in a decade.

More property firms have been scrambling to avoid missing debt deadlines recently, as a government clampdown on the real estate sector and a liquidity crisis at giant China Evergrande Group make it tougher for firms to roll over their dollar debt. Other recent examples include Xinyuan Real Estate Co., which last month secured approval on an exchange offer for a bond.

“We will see more of such offers or even defaults in coming weeks and months,” said Eddie Chia, portfolio manager at China Life Franklin. “Yango is a top developer that had normal operations, albeit slightly more leverage, but clearly it is threatened by a confidence crisis. The other developers in the dollar bond market are much smaller than Yango, and most issuers cannot survive if the market is closed.”

Extending payment deadlines are a temporary solution. Investors are betting that granting reprieve now will allow firms to improve their liquidity when the primary market re-opens for China’s riskier borrowers, though it’s unclear when that may happen.

Fitch Ratings highlighted that Xinyuan’s default risks remain high, for instance, even after it raised its issuer default rating on the firm to CC from restricted default.

Even if builders can delay their near-term bond repayments, they may still struggle to shore up their financial health as sales slow and profits tumble. China’s top 100 developers saw their revenue fall 32.2% compared to the previous year in October.

Rising scrutiny over China’s weakest players also means not all firms will be able to secure bond extensions. Modern Land China Co. failed to repay either the principal or interest on a $250 million bond late last month after it earlier terminated a proposal to extend the bond’s maturity by three months.

At least four builders defaulted last month as limited access to refinancing channels threatened a wave of deliquincies. Some of China’s worst-performing dollar junk bond borrowers have some $2 billion in onshore and offshore bond payments due November.

This week’s developer payments include:

- Scenery Journey $41.9 million coupon on note due 2022: Nov. 6

- Scenery Journey $40.6 million coupon on note due 2023: Nov. 6

- Zhenro Properties Group Ltd. $13.7 million coupon on note due 2023: Nov. 6

- Central China Real Estate Ltd. $7.79 million coupon on note due 2023: Nov. 7

©2021 Bloomberg L.P.