Table of Contents

Offering ITC benefit under GST will bring down property rates by 10%: CREDAI

Update on August 13, 2021: Developers’ body CREDAI has urged the government to allow input tax credit (ITC) to builders, saying that this move could bring down the cost of purchase for home buyers by 10%.

Under the new GST regime, a 5% tax is charged without ITC on under-construction properties that are not under the purview of the definition of affordable housing. On affordable housing, the GST rate is 1%, without ITC.

“Owing to the prevailing exorbitant construction costs, we strongly believe that such a move could rationalise housing prices by 10% and spur the supply of affordable housing projects across tier-1 markets,” the CREDAI said, in a statement on August 10, 2021.

“Currently, the total value of per sq ft GST cost in India lies anywhere between Rs 360 and Rs 500, varying from project to project. Owing to the prevalent scheme, this results in a proportionate increase in the construction cost, which is ultimately borne by the home buyers, impacting their purchasing power and overall demand for homes,” the CREDAI stated, indicating that the ITC foregone was more than the GST chargeable at 12%.

Considering that the average housing rates across India range from Rs 4,000-4,500 per sq ft, the absence of ITC leads to an approximate increase in housing prices by Rs 400-450 per sq ft, the CREDAI said.

“While the implementation of GST has been a complete game-changer for the entire economy in the last four years, we strongly believe that Indian real estate still requires certain tweaks and measures, to ensure a more conducive environment for all stakeholders,” CREDAI national president Harsh Vardhan Patodia said, adding that the inability of developers to avail of input tax credit under the current composition scheme was adversely impacting construction costs and housing prices.

The association is also of the view that some construction materials like cement, taxed at 28%, need to be brought down to 12%-18%. “With the increase in prices of cement, steel and metals among others, the GST component on input services have gone up tremendously. All such increases in GST affect the general public at large. In such a scenario, it would be better that there is an opportunity for builders to opt for ITC and charge 12% GST,” said Atul Banshal, CFO, Experion Developers.

All about GST on real estate

Among the many taxes that home buyers have to pay on property purchase is the Goods and Services Tax or GST on flats.

Many changes have already been made in the GST tax regime, in a short span of time since it came into force in July, 2017. Even though it has been four years since the launch of the GST regime, the real estate sector still feels there is a lot of scope for improvement in the regime, which was introduced with much fanfare. While the government has yet to deal with these issues and more, we examine the implications of the GST for real estate in general and home buyers, in particular in this article.

Taxes before GST implementation

Before the GST came into force, a variety of state and central taxes were imposed on buildings, through the course of the construction of a housing project. While these taxes increased the cost of project development for developers, no credit against this tax was available to the builders against the output liability. Some of the taxes that real estate developers had to pay before the GST came into force included Value Added Tax (VAT), Central Excise, Entry Tax, LBT, Octroi, Service Tax, etc. The cost incurred on these taxes by builders, was then transferred to the property buyer.

Moreover, as buyers had very little clarity over the various taxes and the applicable rates, developers were also in a position to manipulate numbers, to keep the deal to their best advantage. For a common buyer, it would have been an uphill task, to find out the VAT, Central Excise, Entry Tax, LBT, Octroi and Service Tax rate applicable on property construction.

After GST implementation

With much fanfare, the GST regime was launched in India on July 1, 2017. Touted to be the biggest tax reform in India after Independence, the GST subsumed multiple indirect taxes, to offer a uniform regime to the tax payer. Initially, the GST for real estate was kept higher but the Narendra Modi-led government, which launched the revolutionary tax regime, reduced the rates in 2019. This was done, in a bid to make properties more affordable to the common man and to boost its ambitious ‘Housing for All by 2022’ target.

Types of central and state taxes that GST subsumed

Listed below are the types of central and state taxes that the GST subsumed:

Central taxes

- Excise Duty

- Customs Duty

- Special Additional Duty of Customs

- Service Tax

- Central Sales Tax

- Central surcharge and cess on supply of goods and services

State taxes

- State Value Added Tax

- Entertainment Tax

- Luxury Tax

- State Excise Duty

- State surcharge and cess on supply of goods and services

- Taxes on advertisement

- Purchase tax

- Taxes on lotteries, gambling and betting

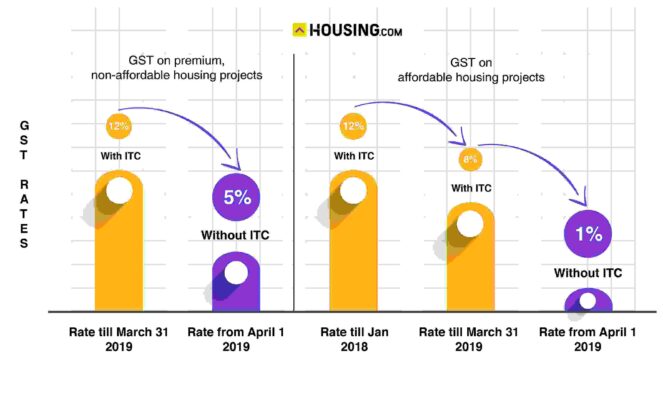

GST rate on real estate

With the intent to simulate demand amid a prolonged slowdown, the government has reduced the GST rate on property transactions significantly. This could potentially lower the buyers’ pay-out by 4%-6% on the overall purchase, believe experts.

| Property type | GST rate till March 2019 | GST rate from April 2019 |

| Affordable housing | 8% with ITC | 1% without ITC |

| Non-affordable housing | 12% with ITC | 5% without ITC |

While the new tax rate without input tax credit (ITC) will apply on all new projects, builders were given a one-time option to pick between the old and the new rates by May 20, 2019, for their ongoing projects. This offer was valid only for projects which were incomplete as on March 31, 2019. The government’s decision came, after the developer community raised concerns on the tax liability in the absence of ITC.

What is input tax credit (ITC) under GST?

A unique characteristic of the GST law is its ITC system, which makes it different from the previous tax system in India. From the start of a housing project, till its completion, a real estate developer pays tax multiple times on the purchase of goods and services. Under the GST regime, the builder would get input tax credit when he pays his output tax.

Example:

A developer has to pay Rs 25,000 as tax on his final product. The builder has already paid Rs 21,000 as input tax, while purchasing materials such as steel, cement, paint, etc. In this scenario, he would have to pay only Rs 4,000 as output tax, after adjusting the input tax credit.

GST on construction services

While real estate in India does not directly fall under the purview of the GST regime, various activities and services in the sector are taxable under the new regime. Following are the rates at which associated activities in the construction sector are taxed, under the GST regime in India:

| Under-construction home bought under the PMAY Credit-Linked Subsidy Scheme (CLSS) | 8% |

| Under-construction home bought without the subsidy | 12% |

| Works contract for affordable housing | 12% |

GST rate on construction and building materials

The Goods and Services Tax (GST) covers real estate in India through works contracts and building and constitution works, as all components used in the development work attract GST. To put it simply, covered under the new regime is the Indian construction industry, which continues to attract high rates of taxes through a blend of levies imposed on the purchase of various building construction materials.

Read out our article on GST rate for cement, construction and other building materials, for a comprehensive list of rates.

What is affordable housing as per GST?

According to the government-determined definition, housing units worth up to Rs 45 lakhs qualify as affordable housing. However, the unit must also conform to certain measurements. A housing unit in a metropolitan city qualifies to be an affordable house, if it costs up to Rs 45 lakhs and measures up to 60 sq metres (carpet area). The Delhi-National Capital Region, Bengaluru, Chennai, Hyderabad, the Mumbai-Mumbai Metropolitan Region and Kolkata are categorised as metropolitan cities. A housing unit in any other city barring the ones mentioned above in India, qualify to be an affordable house, if it costs up to Rs 45 lakhs and has up to 90 sq metres of carpet area.

GST on maintenance charges for housing societies

Flat owners are liable to pay 18% GST on residential property, if they pay at least Rs 7,500 as maintenance charge to their housing society. Housing societies or residents’ welfare associations (RWAs) that collect Rs 7,500 per month per flat, also have to pay 18% tax on the entire amount. Housing societies which have an annual turnover of less than Rs 20 lakhs are, however, exempted from paying the GST. For the GST to be applicable, both the conditions should apply – i.e., each member should pay more than Rs 7,500 per month as maintenance charge and the annual turnover of the RWA should be higher than Rs 20 lakhs.

The government has also clarified that the entire amount is taxable, in case the charges exceed Rs 7,500 per month per member. For example, if the maintenance charges are Rs 9,000 per month per member, the 18% GST on flats will be payable on the entire amount of Rs 9,000 and not on Rs 1,500 (Rs 9,000-Rs 7,500). Also, owners with multiple flats in the same housing society will be taxed for each unit separately.

On the other hand, RWAs are entitled to claim ITC on tax paid by them on capital goods (generators, water pumps, lawn furniture, etc.), goods (taps, pipes, other sanitary/hardware fittings, etc.) and input services such as repair and maintenance services.

CHS has to pay GST on maintenance: Maharashtra AAR

Update on July 20, 2021: The Maharashtra Authority for Advance Rulings (AAR) has ruled that the Goods and Services Tax (GST) is chargeable against the maintenance charges collected by a cooperative housing society (CHS) from its members, if the amount exceeds Rs 7,500 per month. The reiteration of the fact was made when the AAR delivered its order in a case related to Andheri-based Emerald CHS, recently.

Since maintenance charges are treated as a consideration received for supply of goods and services, a CGHS has to levy and collect GST at 18% on the maintenance charges, if these exceed Rs 7,500 per month, per member. However, since a CHS, with an annual turnover of Rs 20 lakhs or less, does not have to register itself and does not quality as a distinct entity under the new tax regime, it is not liable to pay any GST on maintenance charges it collects from its members.

Meanwhile, the Madras High Court has ruled that the GST is applicable to monthly maintenance amount exceeding Rs 7,500 only and not on the full amount. The verdict by the HC overturns a 2019 circular issued by the Central Board of Indirect Taxes and Customs, which said exemption should be granted only if the charges are limited to Rs 7,500 per month and that the full amount would be taxed beyond that.

The court order also quashed a 2019 order that said that an exemption was permissible, only if the contribution was up to Rs 7,500 and that the entire amount would be taxed if the monthly maintenance charges exceeded that amount.

Update on November 17, 2020: The Maharashtra bench of the GST Appellate Authority for Advance Rulings (AAAR) upheld an earlier ruling by the GST Authority for Advance Rulings, stating that cooperative housing societies would have to pay GST on maintenance charges they collect, if the monthly subscription or contribution charged from members was more than Rs 7,500 per month and the annual aggregate turnover is Rs 20 lakhs or more.

GST on rent

Landlords do not have to pay GST on real estate rental income, as long their premises are let out for residential purposes. However, the GST regime treats renting out of residential property for business purposes as supply of services, thus, including rental income under its purview. An 18% GST on residential flats is charged on such rental income under the new regime, if the rent amount per year exceeds Rs 20 lakhs. In this case, landlords also have to register themselves, to pay the GST on their rental income.

Unlike under the Service Tax regime, the threshold limit for applicability of GST has been increased from Rs 10 lakhs per annum to Rs 20 lakhs. So, many of the landlords who were covered under the Service Tax regime, will go out of the indirect tax net, under the GST. On letting-out of commercial properties, a GST at 18% is levied.

Landlords do not have to pay GST on electricity charges recovered from tenants: Gujarat AAR

Landlords do not not have to pay the GST on electricity recovered from tenants, the Gujarat Authority for Advance Ruling (AAR) for Goods and Services Tax (GST) has said, saying these charges are not included in the value of supply. The Gujarat AAR passed the order on a plea of Gujarat Narmada Valley Fertilizers & Chemicals. Under the GST laws, when a landlord incurs an expense while providing a service to the tenants, he does not have to pay the GST on the amount he recovers from the tenant. The law does make it mandatory for the landlord to pay the GST on the rent amount, as mentioned in the rent agreement.

“The applicant has cast an onus on the lessee to pay the charges in respect of the electric power used by them directly to the electricity company. It cannot be said that the electricity charges would be covered by Section 15(2)(c) of the CGST Act, 2017, for the sole reason that the rate for renting of premises has been fixed at an amount and the electricity charges are to be borne by the lessee, as per the actual usage of electric power by them in terms of the agreement,” the AAR said in its verdict.

However, it added that electricity charges would not be included in the value of rent while computing the GST, only when the rent agreement clearly states that the tenant would bear the electricity charges on actuals. This means that the rent agreement must mention that the tenant would bear the electricity charges on actuals, apart from paying the rent, for the landlord to avoid paying GST on the electricity charges recovered from the tenant.

“The electricity charges collected by the landlord from the tenant at actuals based on the reading of the sub-meters is covered under the amount recovered as a pure agent, in terms of the provisions of Rule 33 of the CGST Rules, 2017, in respect of the lessor. The decision would apply only in respect of the agreement under discussion and the analogy of this decision would not be applicable to different sets of circumstances,” the AAR said.

No GST applicable on rent received from backward classes welfare department, rules AAR

The Authority of Advance Ruling (AAR) in Karnataka has said that GST is not applicable on rent received from the backward classes welfare department. The order by the AAR was made with reference to an application, where one Sri Puttahalagaiah had rented his property to run a post-metric girl’s hostel for a rent of Re 1 per month under an agreement with the extension officer of the backward classes welfare department.

GST on home loan

While there is no applicability of the GST on home loan repayment as far as the borrower is concerned, financial institutions offer several ‘services’ as part of home loans. Based on the fact that these are services, the applicability of GST comes into picture. Consequently, if you are taking a housing loan, the bank would charge GST on the processing fee, technical valuation fee and legal fee.

GST on government housing schemes

The government has clarified that government-led mega housing projects meant for the common man, will attract only 1% GST under the new regime. These housing schemes include as the Jawaharlal Nehru National Urban Renewal Mission, the Rajiv Awas Yojana, the Pradhan Mantri Awas Yojana and housing schemes of state governments.

Impact of GST on affordable property

The presence of multiple taxes prior to the GST may not have impacted property prices excessively. Nevertheless, it made tax computation a tedious process for the home buyer. Consequently, not many buyers would venture to find out the various taxes that added up to the final cost of the property. Although several teething issues remain, the effect of GST on property, is that it offers better clarity to home buyers about their tax liability, than the previous regime. With the GST impact on real estate sector resulting in greater transparency, buyers would have more faith in the taxation of property transactions in India. Moreover, properties could become more affordable, even if the rates are reduced marginally. Here’s a look at how to calculate GST on flats’ purchase in the affordable housing segment:

| Affordable housing | GST on affordable housing before April 1, 2019 | GST on affordable housing after April 1, 2019 |

| Property cost per sq ft | Rs 3,500 | Rs 3,500 |

| GST rate on flat purchase | 8% | 1% |

| GST | Rs 280 | Rs 35 |

| ITC benefit for material cost of Rs 1,500 at 18% | Rs 270 | Not applicable |

| Total | Rs 3,510 | Rs 3,553 |

The sales of under-construction housing units has witnessed a slowdown after a peak at the start of the 2010s. The government has since, stepped in, to give this segment a boost by reducing the GST and increasing the tax deduction limit on home loan interest repayment to Rs 3.50 lakhs. In the Interim Budget 2019, the government inserted a new Section 80EEA, to offer an additional benefit of Rs 2 lakhs, to first-time buyers of affordable properties. The GST impact on real estate sector, combined with these cost advantages, are gradually expected to boost buyer sentiments.

Recall here that among the costs that builders in India had to bear on housing project development were excise duty, value-added tax, customs duty, inputs and service tax on approval charges, architect professional fees, labour charges, legal charges and entry taxes on raw materials.

For developers, an increase in demand would help them to sell off their stock and thereby, not have to worry about paying taxes on inventory. Data available with PropTiger.com show that real estate developers in India’s eight prime residential markets are sitting on an unsold stock of over 7.23 lakh homes.

Impact of GST on luxury property

Under the new GST rates, buyers of luxury properties will save more than they would have earlier. Here’s a look at how to calculate GST on flat purchase in the luxury segment:

| Luxury housing | Before April 1, 2019 | After April 1, 2019 |

| Property cost per sq ft | Rs 7,000 | Rs 7,000 |

| GST rate on flat purchase | 12% | 5% |

| GST | Rs 840 | Rs 350 |

| ITC benefit for material cost of Rs 13,000 at an average of 15% | Rs 126 | Not applicable |

| Total | Rs 7,714 | Rs 7,350 |

While the government has already slashed the GST rates for real estate and there might be no scope for further lowering of rates for the sector, industry experts are of the view that lowering of rates on other goods and services, may trigger investments in real estate at a time when home sales have dipped, because of the economic crisis following the Coronavirus pandemic.

Industry bodies, such as the ASSOCHAM and NAREDCO, have already suggested that the government reduce the GST on various goods and services by up to 50% for a fixed tenure. “For ‘money to spend’, the simplest option is to reduce GST on various goods and services. Money going to more sellers and producers, as a result of lower GST, will result in more transactions, effectively boosting the demand-side, in turn creating need to produce more. This will not just increase jobs across segments but also fuel demand for raw materials,” NAREDCO president Niranjan Hiranandani was quoted by the media as saying. “This step has the potential to positively impact the overall rate of recovery. For real estate, it will incentivise the ‘fence sitters’ to stop procrastinating and take a ‘buy’ decision,” he added.

GST as a tool to revive sales

Caught in the middle of an over five-year demand slowdown and high levels of inventory, cash-starved builders in India had extremely low scope for price reduction in the post-Coronavirus lockdown period. However, to make home purchases more lucrative for buyers, a majority of them offered a complete waiver on the GST during the festive season, to boost sales. Most developers, who were approached by this writer to offer their quotes on festive sales, said they had offered complete waivers on GST and stamp duty, to attract buyers during the much-talked about festive season that was instrumental in helping the economy recover to some extent, after the lockdown.

See also: Will 2020’s festive season bring cheer to India’s COVID-19-hit housing market?

GST fact check: Did you know?

|

Must-know facts about GST

GST is not applicable on ready-to-move-in properties; it is applicable on under-construction properties only

It is important to note that the GST does not cover the real estate sector under its ambit. The tax rate applicable on a property building is charged under ‘work contracts’. This is precisely why a developer cannot charge GST on the sale of ready-to-move-in homes. Upon completion and after receiving the occupancy certificate, a property is categorised as ready-to-move-in and is out of the purview of work contract. In short, the GST would apply on the sale of under-construction properties that have yet to receive the OCs. It also begs mention here that in the previous regime, buyers also had to pay service tax on the purchase of ready-to-move homes.

However, since the developer/owner has paid GST as part of the purchase, he would eventually package this expense as part of the overall cost of the property. This basically means that while there is no GST applicability on ready homes, the buyer ultimately pays it anyhow.

GST is not applicable on land transactions

The sale of land is also outside the purview of the GST on construction services, as the sale does not involve the transfer of any goods or services. As the cost of land is a crucial factor that determines property prices, GST provides a standard abatement of 33% of the total contract value, towards value of land for taxable real estate transactions.

Example: How to calculate GST on under-construction property

Suppose that an under-construction property worth Rs 100 is sold by a builder to a buyer. To calculate the GST on building, Rs 33 will be counted out as the land value and the GST on construction would apply only on the remaining Rs 77.

GST on sale of developable plots

While there are no GST implications on the sale of plots, the same is not true if the land parcel for which the transaction is recorded qualifies as developable land.

Before the Gujarat Authority for Advance Rulings (AAR) in a ruling specified that the sale of developed plot was a ‘service’ and thus, taxable under the current regime, the general understanding was that the sale of developable land was out of the purview of the GST. This is because a listing in Schedule-III of the CGST Act establishes that the sale of land and the sale of buildings will be treated neither as supply of goods nor as supply of services.

Gujarat AAR ruling on sale of developable plots

While delivering its judgment on a case of a Surat-based applicant, the Gujarat AAR said that construction of plotted developments or similar structures fall under Schedule-II Para 5 Clause (b) of the Central Goods and Services Tax (CGST) Act. In June 2020, the Gujarat AAR said that providing amenities like water, electricity and other primary facilities as part of a plot sale, constitutes rendering of services and therefore, attracts the services tax under the GST. It also clarified that the sale of ‘developed plots’ with primary amenities is not equivalent to the ‘sale of land’.

Even though the Gujarat AAR ruling is legally applicable on the individual case, it might act as a precedent for other AARs, to issue similar verdicts in case of future disputes. That is a highly likely scenario since Schedule-III of the CGST Act also states that the sale of land does not attract the GST, only if the transaction relates to the transfer of ownership of land exclusively. Schedule-II, Clause 5(b) of the CGST Act states that construction of any complex, building or civil structure meant for further sale is considered as supply of service and would thus attract the GST.

Rate of GST on developable land

In view of the AAR verdict, buyers will have to pay 18% GST, if they are investing in developable plots. Before the GST regime, sale of immovable properties was excluded from the purview of the value-added tax and thus, only direct taxes like stamp duty and registration charges were paid during such transactions.

What is developable land?

This begs the question: Are not all plots developable? The answer is, no. Only those plots, where the owner has obtained all the necessary permissions from local and municipal authorities to carry out future development over the land parcel, qualify as developable plots. To facilitate the future development, the owner also has to develop the basic infrastructure. If any or all of these activities have been performed on the land parcel, it would qualify as developable land:

- Demarcation of plot

- Ground leveling

- Boundary wall construction

- Road construction

- Construction of overhead tanks

- Laying work of water pipelines

- Laying work of underground sewerage lines

- Setting up of water harvesting facility

- Setting up of sewage treatments plants

- Development of landscaped gardens

- Setting up of a drainage system

GST impact on stamp duty and registration charges

Despite the demands made from time to time, ever since the GST regime into force, to discontinue stamp duty and registration charges on property, the government has made no move on this front. Hence, property transactions in India continue to attract stamp duty and registration charges. While states levy stamp duty in the range of 5%-10%, the registration charge is either 1% of the property value or a standard fee.

Note: GST on flat registration: There is no GST on the registration charges that are paid while registering a property.

Can we except GST to subsume stamp duty and registration charges in future? Experts do not think so.

“A large part of the revenue earned by states in India, is through stamp duty on property deals. If states were to let go of this income, the exchequer would suffer much higher losses than it already does. This fact leads us to believe the possibility of the GST subsuming the two charges are nil, at least in the foreseeable future,” says Prabhansu Mishra, a Lucknow-based lawyer.

GST real estate timeline2000 The then PM Atal Behari Vajpyee sets up a panel to design a GST model. 2004 The then finance ministry’s advisor Vijay Kelkar recommends that GST replace the existing tax system. 2006 Former finance minister P Chidambaram sets April 2010 as the deadline for GST implementation in his budget speech. 2011 March 22: Government tables 115th Constitution Amendment Bill in the Lok Sabha, to introduce the GST. 2014 December 18: Cabinet approves 122nd Constitution Amendment Bill to GST. December 19: FM Arun Jaitley introduces the Constitution (122nd) Amendment Bill in the Lok Sabha. 2015 May 6: Lok Sabha passes GST Constitutional Amendment Bill. May 12: The Amendment Bill is presented in the Rajya Sabha. 2016 September 2: 16 states ratify the GST Bill; President gives assent to the Bill. September 12: Cabinet clears formation of the GST Council. September 22-23: The GST Council meets for the first time. November 3: The Council decides on a four-slab tax structure of 5%, 12%, 18% and 28%, plus additional cess on luxury and sin goods. 2017 July 1: GST is rolled out; 8% rate proposed on under-construction properties. 2019 February 24: Government reduces the GST rate on under-construction property to 5% from 12%, and 1% from 8% on affordable housing. May: Government gives builders a one-time option to choose between the old GST rate with ITC or new lower GST sans ITC. Those not making a choice are automatically switched to the new regime after May 20. |

Can we expect further GST cuts in 2021?

Most real estate developers are offering GST-free deals to home buyers, to boost housing sales in the aftermath of the Coronavirus pandemic, as the scope for offering pre-COVID-19 discounts is extremely limited.

Real estate developers, who are currently reeling under the impact of a demand slowdown, because of the ongoing Coronavirus-induced economic difficulties, feel that more benefits under the GST regime must be offered to the real estate sector in view of the new situation, to incentivise investment in under-construction properties – a segment that is losing out to the ready-to-move-in homes segment, as the former attracts GST while the latter does not.

“Most of the demand today is for ready-to-move-in properties, which do not attract any GST. Developers, on the other hand, require working capital to execute ongoing projects. Due to a lack of buyer interest in under-construction homes, developers would be unable to access one of the formerly ‘conventional’ funding options: interest-free capital raised directly from the market,” says Ashok Gupta, CMD, Ajnara India Ltd.

According to NAREDCO president Niranjan Hiranandani, further reduction in GST rate for the entire sector would augur well for real estate.

“The economic recovery is scaling up gradually in the backdrop of festive tailwinds, buoyant capital markets, softening of home loan interest rates, record high foreign reserve and FDI, increasing employment rate and optimistic demand impetus. A cut in GST will go a long way in strengthening sustainable demand and build positive consumer confidence for H2 FY 21-22,” he said.

However, since the GST on affordable housing is already at its lowest level, there is hardly any scope for lowering it further. As the luxury housing segment has been at the receiving end of a demand slowdown, some tweaking of rates for this segment could revive demand in this segment.

Latest news on GST

Builders donating medical equipment to battle second wave of COVID-19 seek GST exemption

Even as they scale up efforts to help authorities battle the extraordinary medical emergency caused by the second wave of the Coronavirus pandemic, the real estate community has demanded they be offered GST exemption on equipment they have been purchasing, to donate to hospitals.

The government levies GST in the range of 12%-18% on equipment used to battle against the various complications caused by the virus in an infected patient, including oxygen plants, oxygen concentrators, oximeters and oxygen cylinders.

The Jodhpur Builders’ and Developers’ Association has, for example, written to the state administration, seeking GST waiver on the purchase of such equipment, in order to be able to buy more such products which India urgently requires in the wake of soaring infections. The association recently started the process to import 25 oxygen concentrators from China.

Failed land transactions can attract GST

The Gujarat Authority for Advance Rulings has said that if a seller exits a contract, by forfeiting the advance money paid by the buyer, this move will be termed as ‘a service’ under the Central Goods and Services Tax Act, 2017, and thus, attract GST. This means that even in case of failed property deals, GST will be applicable. According to the Authority, this forfeiture of advance money will be taxed as supply and the person forfeiting the money will be considered the supplier. The ruling by the AAR came, in response to a case related to a textile company, Fastrack Deal.

Pass on GST gains to buyers, NAA tells builders

November 16, 2020: In a move that might result in real estate developers in India being more forthcoming in passing on the benefits of GST cuts, the National Anti-profiteering Authority (NAA) has, in November 2020, ordered two builders to cut prices of flats to pass on the profiteered amount to buyers, with 18% interest.

GST cut not always beneficial for the industry: Finance secretary

November 3, 2020: Finance secretary Ajay Bhushan Pandey has said that GST rate cuts send a wrong signal to domestic business/industries, as well as international investors. Keeping that in view, a rate cut should be done once in a year after intensive analysis of all sectors, he said, adding that a rate reduction does not necessarily benefit industries.

Signature Builders guilty of not passing the benefit of additional ITC to home buyers

October 26, 2020: The National Anti-Profiteering Authority (NAA) has found Signature Builders guilty of not passing the benefit of additional ITC to the home buyers. The NAA, however, imposed no penalty on the builder since no penalty provisions were in existence between 2017 and 2018, when the builder violated the provisions of Section 171 (1). Under the GST law, penalties for violation of rules are prescribed under Section 171 (3A).

GST applicable on one-time maintenance deposit that builders collect: AAR

The goods and services tax (GST) is applicable to the one-time maintenance deposit that builders collect from home buyers, the Gujarat bench of the Authority for Advance Rulings (AAR) has said. According to the Authority, this charge falls in the category of supply of services and is non-returnable in nature. The AAR, however, added that the GST will be deducted from the maintenance amount when this money is actually spent in carrying out maintenance works in future.

Recall here that most real estate developers collect a one-time maintenance deposit from home buyers, before the formation of the residents’ welfare associations or cooperative housing societies that take over the responsibility of maintenance from the builder. After the formation of the RWA and CHS, they become solely responsible for the maintenance work and can come up with their own set of rules for calculating maintenance charges. The builder would no longer be able to have a say in the matter.

This individual liability of home buyers is calculated on the basis of the size of the property – a certain per sq ft rate has to be paid by the home buyers. The entire amount collected from buyers as a one-time maintenance charge is then deposited into a common fund and is used for its intended purposes as and when required.

Since there has been an absolute lack of clarity on laws governing collection of this levy, there have been various instances, where disputes have arisen between buyers and developers on the applicability of GST on the one-time maintenance charge.

It has been a common practice among developers to deduct GST at the rate of 18%, right after the collection and then deposit the remaining amount into the common fund. After the AAR ruling, developers will have to deposit all the amount without any GST deduction.

Also note that builders were not liable to pay service tax on such maintenance deposits before the GST regime became applicable in 2017.

With the AAR’s ruling, RWAs and CHSs can now collect the GST from society members as and when the time to utilise this amount comes, since the builder would charge this levy initially. In essence, it is only a deferral of the payment, as far as home buyers are concerned.

Industry disappointed as Budget 2021 keeps quiet on GST

Demand for rate uniformity in Budget 2021

The housing segment was expecting further rationalisation of the GST rates in Budget 2021, as a support move from the government. While the government had lowered the rate for affordable housing to 1%, the industry was of the view that a uniform rate of 1% should be levied on all under-construction projects, irrespective of the ticket size. However, they were a disappointed lot, following the Budget on February 1, 2021, as finance minister Nirmala Sitharaman decided to maintain silence on the subject.

“It was important to bring back the input tax credit as part of the GST reforms and lower the rates for purchase of raw materials. This would have helped reduce the cost of construction. A waiver of GST on under-construction projects, could also have boosted demand in real estate,” said Lindsay Bernard Rodrigues, co-founder and director of Bennet & Bernard Group.

According to Vikas Garg, deputy MD, MRG World, some clarity on the input tax credit would have made matters better for the industry, considering that the prevalent economic situation makes it almost impossible for real estate developers to deliver projects on time, amid the monetary pressure that is being further stoked by the demand slowdown.

See also: Budget 2021: Lack of tax incentives leave home buyers, builders disappointed

GST real estate FAQs

Is real estate included in GST?

GST is applicable on under-construction properties that have not yet received the OC (occupancy certificate).

What is the current GST rate in India for real estate?

With effect from April 1, 2019, 1% GST is charged on affordable residential apartments without ITC, while 5% GST without ITC is charged on other residential properties.

What is GST for under construction property?

With GST rate cut on under-construction properties, the GST for under-construction affordable housing units is 1%, while for non-affordable projects it is 5%, without input tax credit.

How GST impact real estate in India

The GST Council’s decision to reduce the GST rates for under-construction residential housing projects will lead to marginal traction in demand and bring in more transparency for home buyers.

Who pays GST on real estate?

GST is paid by the home buyer and investor, when investing in under-construction properties.

Does a builder have to purchase all goods and services from registered suppliers only to claim ITC?

A promoter should purchase at least 80% goods and services from registered suppliers.

I am a beneficiary of PMAY and carpet area of my house being constructed in an ongoing project is 150 sq metres. Am I eligible for new rate of 1% on same?

You are eligible for the new GST rate of 1%, if the developer has not exercised the option to pay tax on construction of apartments at the old rate of 8%.

Can a developer take deduction of actual value of land involved in the sale of a unit, instead of taking deduction of deemed value of land?

No, only one-third abatement is offered towards value of land while charging GST.

Since when do new GST rates apply?

The new GST rates without ITC, will apply on all housing projects launched after April 1, 2019.

What tax rate is applicable if part of the payment for an under-construction unit is paid after March 31, 2019?

The new flat GST rate 2020 will apply on the part payment, unless the builder has decided to go with the earlier tax rate.

What are the 3 types of GST?

GST in India is of three types: Central Goods and Service Tax (CGST), State Goods and Services Tax (SGST) or Union Territory Goods and Services Tax (UTGST), and Integrated Goods and Services Tax (IGST).

Comments