Highlights

- Indian market’s outperformance part of the global liquidity tsunami

- Markets were resilient during the Spanish Flu a hundred years ago

- The second wave of the pandemic risks demand disruption and margin pressure for India Inc

- Corporate India bracing for a bumpy ride but hopeful of a strong H2; a lot depends on vaccination

- Pandemic a blessing for large corporates, Nifty earnings unlikely to face much heat

- Valuation expensive but could look reasonable on a strong FY23 recovery

- Strong structural liquidity support a game changer – any pullback an opportunity to go long

-----------------------------------------------------------

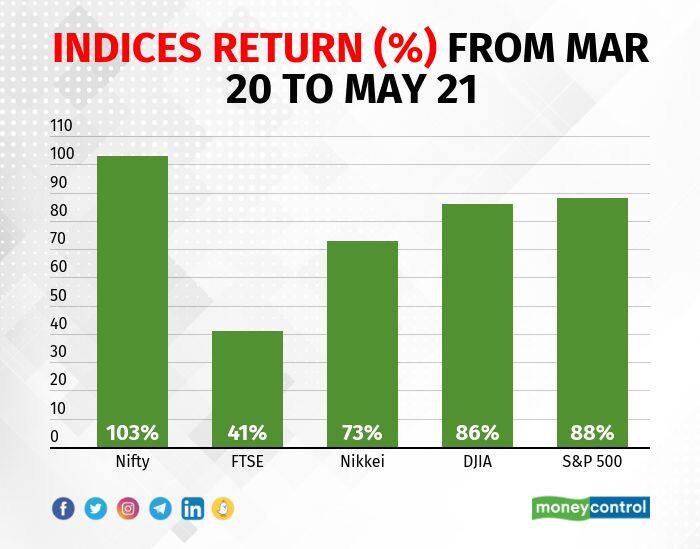

Markets touching a lifetime high amid a raging second wave of the deadly COVID pandemic in India has taken many by surprise. But isn’t it déjà vu? Last year, after an initial knee-jerk reaction that barely lasted a few weeks, the markets rose like a phoenix from the depths of despondency to usher in a bull market, in spite of the pandemic.

Source: Yahoo Finance

While globally this was supported by unprecedented fiscal support and monetary easing that protected many of the developed economies from collapsing, in India, despite moderate support, the markets simply rode the global liquidity wave.

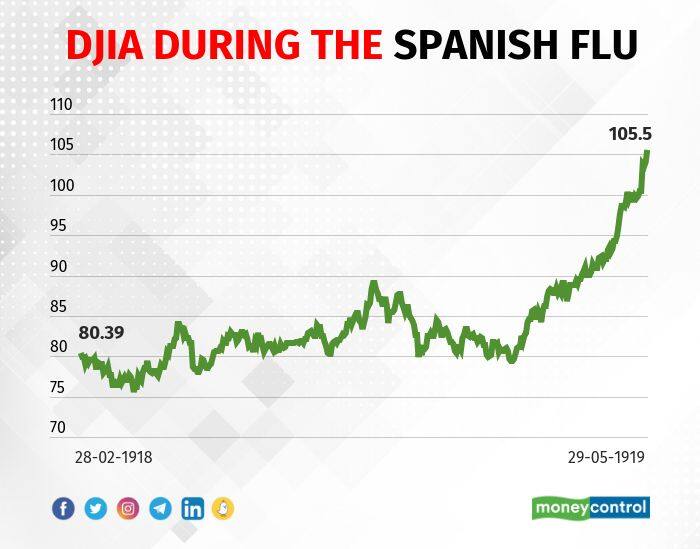

Source: DJIA

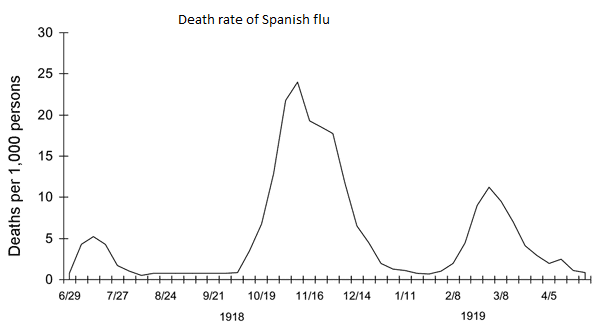

Going by the experience of the only comparable pandemic of the last century – the Spanish flu of 1918-19-- the market’s reaction wasn’t too different. Markets were largely steady with an upward bias during the period of the flu’s three phases, the second wave being the worst, similar to what we are experiencing now.

Source: Global Financial Data

Critics would argue that back in 1918, markets were celebrating the end of World War I. This time around, the celebration started with government and central bank intervention early in the crisis and the rally got its legs from the visibility of a vaccine.

While all these hold for global equities, isn’t it a stretch for India, battling a deadly second wave which has affected both lives and livelihoods?

Phase 1 of the pandemic did see a draconian lockdown, but demand came back strongly and corporates could more than recoup earnings lost in the first half, as soft input prices along with adept cost management aided their profitability. So while the celebration started amid the gloom, earnings did catch up. But is it different this time around?

The corporate sector stands to face the heat more from demand than the supply side. With rising medical expenses and fresh fears of a slowdown leading to job losses, discretionary consumption looks to be at the receiving end. The loss of productivity and localized restrictions are threatening supply chains and fuelling inflationary pressure. To make matters worse, unlike the past year, when commodity prices were benign at the onset of the pandemic due to widespread fears of a global slowdown, commodity prices are now soaring, riding on the optimism of a return to growth in many developed markets and the roll out of mass vaccination. Hence, for India-centric companies, in addition to slow topline performance, gross margin and operating margins are getting squeezed.

While most corporates acknowledge the challenges to short-term growth and profitability and are therefore bracing for a bumpy ride in the first half of FY22, there appears to be a fair degree of optimism on the second half. These hopes are riding on a relatively sharp but shorter second wave of the pandemic on expectations of wider coverage of vaccination in India, given that some of the developed markets have restored near normalcy post a decent vaccination coverage. (Read: Herd Immunity Tracker)

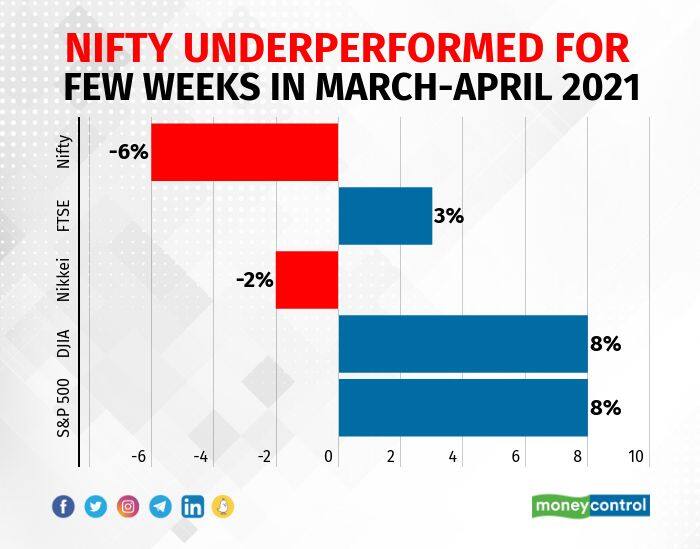

With markets making a wild swing from despondency to euphoria last year, investors do not want to miss a recovery rally this time around and are staying put in the market in the hope of a better second half. So while Indian equities decoupled for a few weeks of March and April in 2021, the losses have been recouped.

Source: Moneycontrol

What is supporting the markets when the economy is in the doldrums?

Markets are willing to live with a muted FY22, hoping for a lot of catching up in FY23. So far, the pandemic has been a boon for larger companies (where the bulk of the equity money is parked) – their better balance sheet quality and exceptional cost management have helped them sail through troubled waters. Moreover, as unorganised smaller players are losing out, the big boys have gained disproportionate market share. This is evident from the earnings report of many consumer facing companies. Hence, it is reasonable to expect that for most large companies, the catch up in earnings post pandemic would be meaningful.

Even in the near-term, thanks to the global exposure of most Nifty constituents like technology, pandemic-proof pharma, commodity rally driven metals or well-run banks with adequate capital and buffer provisions, the second wave is unlikely to make a big dent to earnings. Rural facing businesses and bottom of the pyramid lenders are facing some challenges, but these are perceived as short-term in nature.

The structural liquidity support

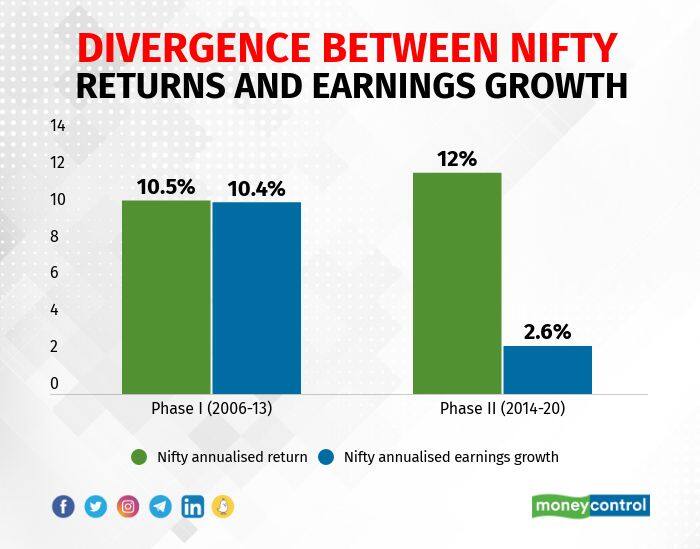

More than earnings, what seem to be lending a solid support for the markets are the supply side factors. Equities, going by the Nifty return, has been an outperforming asset class with a CAGR (compounded annual growth rate) return of close to 11.2 percent in the past fifteen years, although earnings have lagged the price performance, with Nifty earnings growing at a CAGR of only 6.7 percent over this period.

In fact, it has been a tale of two halves that has an important bearing on market return, going forward as well.

Source: Moneycontrol

In the first phase, true to the saying that markets are slaves of earnings, the annualised Nifty return over an eight year period of 2006-2013 at 10.5 percent closely tracked the annualised earnings growth of 10.4 percent. However, this strong correlation was completely broken in the second phase i.e. from 2014 to 2020, when the annualised earnings growth of 2.6 percent had been way behind annualised Nifty return of 12 percent. Several structural factors have contributed to a rally sans earnings.

Demonetisation has been an important contributor in encouraging financialization of savings. The young population with no old age security in India have been a potent contributor to equity flows as most young professionals swear by SIP (Systematic Investment Plans). The assets under management of equity Mutual Funds have risen to a staggering Rs 10 lakh crore at the end of FY21 from Rs 1.65 lakh crore in FY14 – more than six- fold rise in seven years. The pandemic has further bolstered the so called “equity cult” amongst retail investors with the past year seeing the opening of 1.43 crore demat accounts as against 50 lakhs in the preceding year. Paltry return in alternate asset classes like real estate in recent times and record low interest rates have also been extremely supportive of money flowing to equities.

A recent study of RBI analysing equity return data of 15 years suggest liquidity support to have a greater bearing on equity prices compared to economic prospects. While the surge in FPI (foreign portfolio investment) flows has been the icing on the cake post pandemic, domestic liquidity has also provided solid support to equities.

Source: Moneycontrol

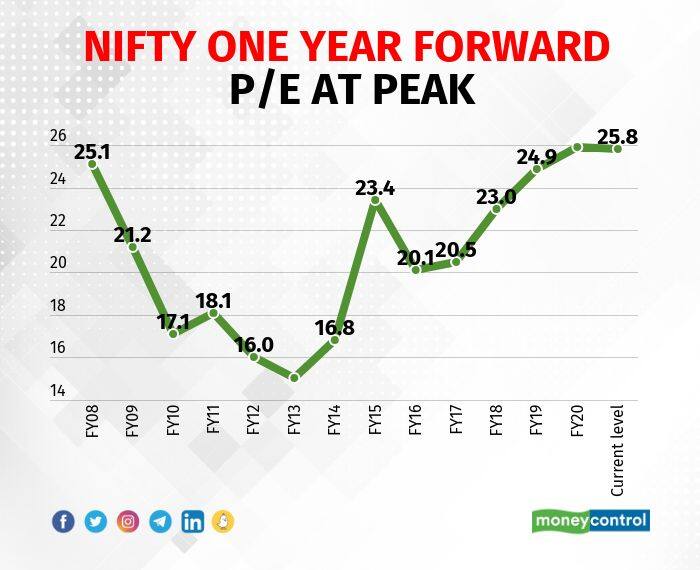

So investors in Indian equities may have to live with optical overvaluation and not shun the markets for the same. The current valuation is close to a historic peak, but could look reasonable from an FY23 perspective, should earnings recover meaningfully.

Source: Moneycontrol Research

Is it a one way street?

Certainly not, as there is always a risk of a third wave and inadequate coverage of vaccination in India that could put a question mark on the bounce back in the second half. Finally, the biggest risk to the rally comes from inflation. Once global recovery is on a firm footing, inflation, which is already lurking, might rear its ugly head beyond the comfort of developed countries’ central banks, forcing policy makers to unwind liquidity support, thus punctuating the global equity rally. However, for Indian equities, the long-term structural liquidity support is hard to ignore and any correction will therefore be short-lived. Unlike FY21 where a tide of liquidity lifted all boats, FY22 is likely to be a stock picker’s market with different businesses showing varying degree of resilience to the pandemic after weathering it for a reasonably long period. Investors, therefore, have to be discerning and follow well researched advice on stock selection. Any pull back is an opportunity to buy into long-term winners from the technology sector, well capitalised large financials, companies benefitting from global sourcing away from China, promising healthcare/pharmaceuticals, consumer companies gaining from the shift to organised plays, “Make in India” beneficiaries and select infrastructure plays with strong balance sheets.