Table of Contents

- Housing for All and the introduction of Section 80EEA

- What is Section 80EEA of the Income Tax Act?

- What is the amount of deduction available under Section 80EEA?

- Further extension of Section 80EEA expected in Budget 2021

- What is affordable housing?

- Income tax deductions for interest paid on home loan

- Who is eligible to claim deduction under Section 80EEA?

- What are the conditions to claim deduction under Section 80EEA?

- What is the difference between Section 80EEA and Section 24(b)?

- What is the difference between Section 80EEA and Section 80EE?

- How home buyers can use Section 80EEA to claim maximum deduction?

- Can I claim deduction under Section 80EEA if loan was taken in 2015?

- ITR filing to claim deductions under Section 80EEA in 2020

- FAQs on Section 80EEA

Presenting the Budget for fiscal 2021-2022, finance minister (FM) Nirmala Sitharaman, on February 1, 2021, said the additional benefit under the section, provided on payment of the interest component of home loans, will be extended till March 31, 2022. In last year’s Budget the FM has extended that timeline for one year to March 31, 2021.

“In the July 2019 Budget, I provided an additional deduction of interest, amounting to Rs 1.5 lakhs, for loan taken to purchase an affordable house. I propose to extend the eligibility of this deduction by one more year, to March 31, 2022. The additional deduction of Rs 1.5 lakhs shall, therefore, be available for loans taken up till March 31, 2022, for the purchase of an affordable house,” Sitharaman said, on February 1, 2021, during her 2021 Budget speech.

“Affordable housing is set to get a boost, from the extension of the tax holiday and Section 80EEA, till March 31, 2022. Looking at the experience of the last one year, affordable housing will get more buyers, as people want to secure their lives by owning a home. The demand for affordable housing is at an all-time high,” said Pradeep Aggarwal, founder and chairman, Signature Global and chairman, National Council on Affordable Housing, ASSOCHAM.

Launched in the 2019 Budget, Section 80EEA helps first-time home buyers to save an additional Rs 1.50 lakhs per year against the home loan interest payments, over and above the Rs 2 lakhs deduction limit allowed under Section 24 (b), for the purchase of housing units worth up to Rs 45 lakhs.

Did you know that first-time home buyers in India enjoy additional deductions on income tax, if they buy the property with the help of home loans? Specific provisions have been made in the Income Tax Act, 1961, to offer exemption to first-time home buyers for purchase of affordable homes, over and above the benefits enjoyed by other categories of buyers. These include benefits under Section 80EE and Section 80EEA.

In this article, we will discuss at length Section 80EEA and answer every question around benefits, eligibility, deduction limit and more, offered to first-time home buyers under this section.

Housing for All and the introduction of Section 80EEA

In its first term that started in 2014, the prime minister Narendra Modi-led NDA government launched its pet ‘Housing for All by 2022’ programme. In order to complete that ambitious target, the central government launched several measures to encourage first-time home buyers. The introduction of Section 80EEA in 2019, was a step in that direction.

With a view to achieving the target of Housing for All by 2020, the government extended the interest deduction under Section 80EEA for loans taken during the period between April 1, 2019 and March 31, 2021.

What is Section 80EEA of the Income Tax Act?

Section 80EEA was introduced by Finance minister Nirmala Sitharaman in the 2019 Union Budget with an aim to give a boost to the centre’s ‘Housing for All by 2022’ programme, by way of offering additional tax benefits on the purchase of affordable homes.

“In computing the total income of an assessee, being an individual not eligible to claim deduction under Section 80EE, there shall be deducted, in accordance with and subject to the provisions of this section, interest payable on loan taken by him from any financial institution for the purpose of acquisition of a residential house property,” reads Section 80EEA.

What is the amount of deduction available under Section 80EEA?

Under the provisions of the section, home buyers can save an additional Rs 1.50 lakhs per year towards the interest paid on home loans, over and above the Rs 2 lakhs that they already save under Section 24 (b) .

“Interest paid on housing loan is allowed as a deduction to the extent of Rs 2 lakhs in respect of self-occupied property. In order to provide further benefit, I propose to allow an additional deduction of Rs 1.5 lakhs for interest paid on loans taken up to March 31, 2020, for purchasing an affordable house up to Rs 45 lakhs in value. Therefore, a person purchasing an affordable house, now will get an enhanced interest deduction up to Rs 3.5 lakhs,” Sitharaman said in her 2019 Budget Speech. The period covered was extended for another year in the Budget 2020.

Do note here that all categories of buyers can claim deduction on home loan interest payment under Section 24(b). The rebate of Rs 1.50 lakhs against interest payment under Section 80EEA is over and above this limit.

Further extension of Section 80EEA expected in Budget 2021

Keeping in view the economic slowdown caused by the Coronavirus pandemic and its impact on residential demand in India, industry experts are of the view that the government should announce a further extension of Section 80EEA in its upcoming Budget for 2021-2022, to be presented by the FM on February 1, 2021. As the government moves closer to its ambitious Housing For All by 2022 deadline, doing so becomes particularly crucial to support the affordable housing segment in the aftermath of the pandemic.

What is affordable housing?

It is pertinent to note here that before Section 80EEA came into effect, properties worth up to Rs 50 lakhs fell under the definition of ‘affordable homes’. With the insertion of Section 80EEA in the income tax law, properties worth only up to Rs 45 lakhs qualify as affordable homes, since September 1, 2019.

Income tax deductions for interest paid on home loan

Who is eligible to claim deduction under Section 80EEA?

The Finance Bill, 2019, further specified the eligibility to avail of benefits under Section 80EEA.

| Who can claim the rebate? Only first-time home buyers can claim benefits under this Section, as it specifies that at the time of grant of the home loan the borrower should not own any residential property.

What is the deduction for? Deduction can be claimed against home loan interest payment only.

What is the deduction limit? The deduction limit is Rs 1.50 lakhs per year.

What is the period covered? Borrowers whose home loans are sanctioned between April 1, 2019 and March 31, 2021, can claim benefits.

Which category of buyer can apply? Only individual buyers can claim deductions under this section. This means companies, Hindu undivided families, etc., cannot claim benefits.

What should be the source of the home loan? The buyer has to take the home loan from a financial institution (banks housing finance companies) and not from family members, relatives or friends.

What should be the property value? The stamp value of the property should not exceed Rs 45 lakhs.

What sort of property is covered? Buyers of residential house property can claim the benefit. It is also specified that the loan must be borrowed for buying the property and not reconstruction, repair, maintenance, etc.

What is the limitation? If a buyer is claiming deductions under Section 80EE, he cannot claim deductions under Section 80EEA. |

Can NRIs claim deduction under Section 80EEA?

Since the law does not specify whether a first-time buyer has to be a resident Indian to claim deduction, it has been interpreted by tax experts that even non-residents claim deductions under Section 80EEA.

What are the conditions to claim deduction under Section 80EEA?

What is the area limit of unit to claim deduction under Section 80EEA?

According to the Finance Bill, if the unit is located in a metropolitan city, its size should not exceed 645 sq ft or 60 sq metres. For units in any other city, the size has been limited at 968 sq ft or 90 sq metres.

Which cities are considered metropolitan cities under Section 80EEA?

Cities that are considered metropolitan for this purpose are Bengaluru, Chennai, Delhi, Faridabad, Ghaziabad, Greater Noida, Gurugram, Hyderabad, Kolkata, Mumbai and Noida.

Can deductions be claimed under Section 80EEA if the property is not self-occupied?

Section 80EEA does not specify if the property must be self-occupied, to seek the tax break. This also allows buyers who are living in rented accommodations to claim deductions while also claiming HRA benefits under Section 80GG.

Can joint owners claim deductions under Section 80EEA separately?

In case the joint owners are also co-borrowers, they can both claim Rs 1.50 lakhs each as deductions under this Section, provided they meet all the other conditions.

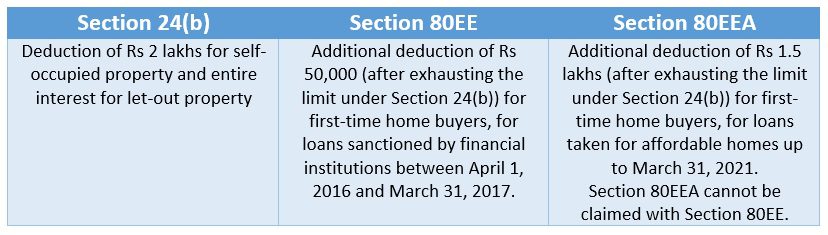

What is the difference between Section 80EEA and Section 24(b)?

Buyers can claim deductions under both, Section 24(b) and Section 80EEA, and enhance their total non-taxable income to Rs 3.50 lakhs, if they meet the eligibility criteria. However, deductions under Section 80EEA can only be claimed after exhausting the Rs 2-lakh limit under Section 24(b).

| Category | Section 24(b) | Section 80EEA |

| Possession | Must | Not required |

| Loan source | Banks or personal sources | Only banks |

| Deduction limit | Rs 2 lakhs or entire interest* | Rs 1.50 lakhs |

| Property value | No specification | Rs 45 lakhs |

| Loan period | Loans taken after April 1, 1999 | April 1, 2019 to March 31, 2021 |

| Buyer category | All home buyers | First-time individual home buyers |

| Lock-in period** | None | None |

*While a rebate of Rs 2 lakhs is allowed for self-occupied property, the entire interest is allowed as deduction in case of let-out property.

**Section 80C specifies that buyers should not sell the property for five years, to claim deductions. This is known as the lock-in period.

What is the difference between Section 80EEA and Section 80EE?

First-time buyers claiming deductions under Section 80EE cannot claim deductions under Section 80EEA. This is specifically mentioned in the law.

| Particulars | Section 80EE | Section 80EEA |

| Property value | Up to Rs 50 lakhs | Up to Rs 45 lakhs |

| Loan amount | Up to Rs 35 lakhs | Not specified |

| Loan period covered | April 1, 2016 to March 31, 2017 | April 1, 2019 to March 31, 2021 |

| Maximum rebate | Rs 50,000 | Rs 1.50 lakhs |

| Lock-in period | None | None |

How home buyers can use Section 80EEA to claim maximum deduction?

Since Section 80EEA has been introduced to help the middle-income group to own a home by way of higher monetary support, let us see how much of his income a person can make non-taxable, if he were to buy his first home today.

Tax calculation example

| Rahul Khanna works at an IT company in Noida and his annual salary package is Rs 15 lakhs. Let us assume that he is not enjoying any tax deductions so far. At the current tax slab, his total taxable income would be:

Rs 15 lakhs – Rs 40,000 (This is the standard deduction all tax payers in India enjoy) = Rs 14.60 lakhs Khanna falls in the Rs 12.5 lakhs-Rs 15 lakhs tax bracket. So, the highest rate at which his income will be taxed is 30%.

Split of Rs 14.60 lakhs for tax calculations Rs 2.5 lakhs (@0%) = 0 Rs 2.5 lakhs (@5%) = Rs 12,500 Rs 5 lakhs (@20%) = Rs 1,00,000 Rs 4.6 lakhs (@30%) = Rs 1,38,000 Total = Rs 2,50,500 + cess (@4%) = Rs 10,020

Khanna’s total tax outgo = Rs 2,60,520

Now, let us assume that Khanna invests in his maiden property to lower his tax outgo. He is buying a property worth Rs 45 lakhs, for which he is taking 80% of the property value (Rs 36 lakh) as loan from a scheduled bank at an 8% interest rate.

Key numbers Loan amount: Rs 36 lakhs Tenure: 15 years Interest rate: 8%

This would lead to: EMI of Rs 34,403 Total interest (in 15 years): Rs 25,92,624 Total payable (in 15 years): Rs 61,90,624

If Khanna took the loan in December 2019, through 2020 (the first year of the loan tenure) he would be paying: Rs 1,29,522 as home loan principal Rs 2,83,319 as home loan interest

Under Section 80C, which offers rebate against specific investments, including home loan principal, Khanna can get Rs 1,29,522 from his income made tax-free (the upper limit under this Section is Rs 1.50 lakhs in a year).

Under Section 24(b), Khanna can claim Rs 2 lakhs as deduction against the interest paid.

Now, under Section 80EEA, Khanna can also claim the remaining Rs 83,319 as deduction from the overall limit of Rs 1.50 lakhs.

After applying all these deductions, here is the breakup of Khanna’s total taxable income:

Rs 15 lakh – Rs 40,000 (Standard deduction) = Rs 14.60 lakh

Deduction under Section 80C: Rs 1,29,522 Deduction under Section 24(b): Rs 2,00,000 Deduction under Section 80EEA: Rs 83,319 Total deductions: Rs 4,12,841

Total taxable income: Rs 14,60,000 – Rs 4,12,841 = Rs 10,47,159

Khanna still falls in the category of over Rs 10 lakh taxable income, so the highest rate at which his income is taxed remains 30%, but the amount to be taxed at 30% has come down significantly. Here is the split of his income for tax calculations:

Rs 2.5 lakhs (@0%) = 0 Rs 2.5 lakhs (@5%) = Rs 12,500 Rs 5 lakhs (@20%) = Rs 1,00,000 Rs 47,159 (@30%) = Rs 14,148

Total tax: Rs 1,26,648 + cess at 4% = Rs 5,066

Total tax outgo: Rs 1,31,714

Total savings as against the earlier outgo: Rs 2,60,520 – Rs 1,31,714 = Rs 1,28,806 |

Can I claim deduction under Section 80EEA if loan was taken in 2015?

Since the provision specifically mentions that the deduction will apply on only those loans that have been/would be granted between April 1, 2019, and March 31 2021, people whose loans have been sanctioned prior to or after this period, will not be eligible to claim the additional rebate under Section 80EEA.

ITR filing to claim deductions under Section 80EEA in 2020

While filing their income tax return for the assessment year 2020-21, the tax payer has to be careful, as the new form carries various new provisions that were introduced in Budget 2019. This is true for the extension of the validity of Section 80EEA till March 31, 2021. The new ITR provides tax payers with the option to claim deductions under Section 80EEA.

Also note that the time limit to file the ITR has been extended till December 31, 2020, keeping in view the Coronavirus pandemic-led complications for the general public.

FAQs on Section 80EEA

When did Section 80EEA come into force?

Section 80EEA was introduced in the Budget 2019. In the Budget 2020, its cover was increased for another year to March, 2021.

What is the deduction limit under Section 80EEA?

First-time home buyers can claim tax deduction of Rs 1.50 lakhs in a year against the home loan interest payment under this Section.

Who is eligible for tax deductions under Section 80EEA?

First-time home buyers can claim deductions under Section 80EEA, if: *The loan has been taken from a bank or housing finance company. *The stamp duty value of property is up to Rs 45 lakhs. *They are not claiming deductions under Section 80EE.

What should be the value of the flat, to avail of the benefits under Section 80EEA?

The stamp duty value of the property should not exceed Rs 45 lakhs.

Can I claim deductions under Section 80EE and Section 80EEA together?

The law clearly states that those claiming benefits under Section 80EE cannot claim rebate under Section 80EEA.

Can I claim deductions under Section 80EEA for plot purchase?

Deduction under Section 80EEA can only be claimed for purchase of housing units, including flats or apartments. The section is not applicable on the purchase of plots.

Can I claim deduction of principal repayment on home loan under Section 80EEA?

Deduction under Section 80EEA can only be claimed against home loan interest payment.

Can I claim deduction of interest payment on electric vehicle loan under Section 80EEA?

Deduction of interest payment on electric vehicle is allowed under Section 80EEB.

Can I claim deduction under Sections 24 and Section 80EEA simultaneously?

Buyers can claim deductions under both these sections and enhance their total non-taxable income to Rs 3.50 lakhs, if they meet the eligibility criterion. However, deductions under Section 80EEA can only be claimed after exhausting the limit of Rs 2 lakhs under Section 24(b).

For how many years is the deduction under Section 80EEA available?

Deductions can be claimed throughout the loan repayment tenure.

Can I claim deductions under Section 80EEA after I buy my second property?

Yes, deductions under the section are available on home loans that are taken when the tax payer had no property. Your future property ownership has no impact on this rebate.

Can my wife and I both claim deduction under Section 80EEA?

Yes, if the property is registered in both names and if she is also a co-borrower in the home loan.

Can I claim deductions under Section 80EEA if I take loan from family members/friends?

No, the loan has to be borrowed from a bank or HFC to claim this benefit.

What is stamp duty value of a property?

The value at which a property is registered in the government records is known as its stamp duty value.

What is the definition of affordable homes?

According to government-defined standards, affordable homes are units priced up to Rs 45 lakhs.

What documents will I have to give to my company to claim tax deduction under Section 80EEA?

The borrower will have to submit the interest certificate issued by his bank, to claim the rebate.

Related Posts

All about home loan income tax benefits.

Finance Act 2016: Tax benefits for home purchase and rent paid.

Budget 2020: Income tax laws that will affect home buyers and builders.

Budget 2021: Extension of ‘safe harbour’ limit to benefit buyers, inventory-hit builders.

How to save on taxes while buying a property.

Advantages of buying a property in joint names.

Comments