We Still Like BOK Financial

No loan loss provisions in the quarter was a strength but keep and eye on energy and some COVID sensitive portfolio exposure.

BOK Financial's efficiency ratio has been strong, while return on assets and equity have improved markedly off this years lows.

Under $65 would be well below book value and only slightly above tangible book value, an attractive price, given our positive view for 2021 growth.

Prepared by Michael, junior analyst at BAD BEAT Investing, and Chris, CEO of Quad 7 Capital

BOK Financial Corporation (BOKF) is a diversified bank stock that we like if you can acquire shares under $65. The company recently reported Q3 earnings. Although our contrarian calls to buy financial stocks starting in in early fall was contrarian it paid and generated solid returns. With that said, bank stocks have still largely underperformed the market, even with the recent run higher. However, the overall outlook is getting better on hopes for improvement in 2021. It will likely be a volatile few months with the height of the COVID-19 case incidence ahead this winter but we think the stock moves higher beyond 2021. One of the things that we really like about BOK Financial is that it is a rather diversified bank. It has a sizable commercial lending segment which has faced a ton of pressure. It also has consumer lending which is hanging in there. Finally, it also offers some investment banking which has been excellent in the last few months with market volatility. We would love a pullback here, but the Q3 numbers were strong. Let us discuss

Q3 top and bottom line review

We have to tell you that we were unsure of how bank earnings would look this quarter, but we expected investment banking would continue to perform well. In Quad 7 Capital's earnings coverage of the financials, we have seen a real mix in the performance of banks based on whether they are more cosumer focused versus investment focused.

Well, BOK Financial reported net revenues of $506 million in Q3. This was solid outperformance. It was a 9% increase from last year's quarter. While we expected an increase and so did analysts, we were looking for $500 million, which we thought was a good target. We believed analysts were conservative in their expectations, particularly on the performance of consumer loans. Well, year-over-year, the top line surpassed analysts' consensus by $24 million. The top-line beat was a key driver which led to a bottom-line beat as well. The revenues were strong but we were most pleased to see a massive decline in loan loss provisions which boosted earnings.

Margins were down slightly in the quarter. Net interest margin was 2.81% compared to 2.83% the last quarter. The pressure on margins stems from the interest rate cuts put into place earlier this year. Now with the top line growth and still decent margins, coupled with absolutely no loan loss provisions in the quarter, we saw a big boost in net income compared to the sequential Q2. Net income was $154.0 million or $2.19 per share in Q3 2020 versus $64.7 million or $0.92 per share for Q2 2020. Closer look at revenue sources.

As we mentioned in the open the bank is a bit diversified. There are three main segments of business: commercial banking, consumer banking banking, and wealth management. Here is the thing. The earnings increase was driven in large part by the lack of loan loss provisions. Overall, all three of these segments saw declines in their contribution to net income versus the sequential quarter. Commercial banking saw a decrease of $5.9 million, consumer banking a decrease of $5.6 million, and wealth management a decrease of $2.2 million. While commercial deposits grew 5%, average commercial loans dropped 5%. The bank had done this intentionally to reduce exposure with some riskier customers/sectors. For consumer banking, it was another strong quarter for the mortgage banking business. The housing market is simply on fire. Low mortgage interest rates are driving this. However, the lower rates are killing the spreads. Wealth Management has kept up a strong level of trading, though not nearly as high as last quarter. ONe positive was that assets under management or administration totaled $82.4 billion, up $3.0 billion since the end of Q2.

We should be aware of what is in the loan portfolio. There is some exposure to risky sectors:

Source: Q3 earnings slides

As we can see, the exposure to energy is a risk, just given the awful price action in that entire sector and their commodities at large. Loan balances are being paid down, but the bank seems hesitant to find new deals worthwhile there. With healthcare, we see boosts from senior care and housing. Loans to individuals are benefiting from the mortgage market mostly. As we move into 2021, we suspect that there is improvement in energy, as well as strong mortgage origination volume.

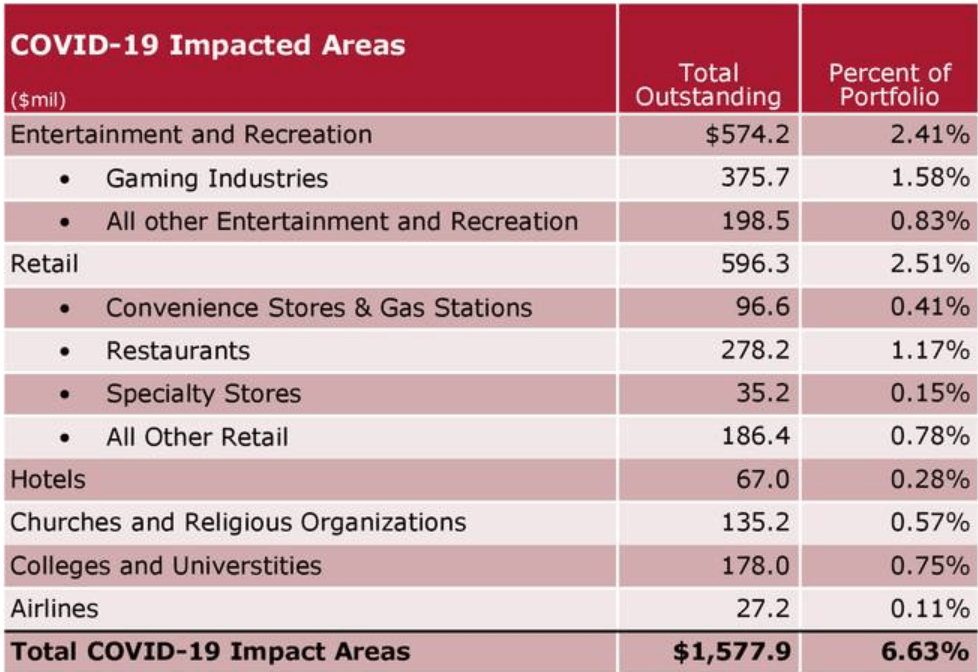

Are there risks?

Source: Q3 earnings slides

Aside from the general risks associated with lending, we really need to be cognizant of the loan portfolio's COVID exposure. COVID is still a very pressing risk for at least the next few quarters in our opinion until vaccines are available and we see a strong level of inoculation in the community. That said, about 6.6% of the portfolio is in COVID impacted areas. Energy is not listed given that while it has suffered, it is not 'directly' due to COVID. However gaming, hotels, travel, and restaurants have been crushed. These are the riskiest loans out there, since survival of many small businesses are in question. However, we do note that loan deferrals have declined 80% from their peak, which is very positive news.

So if all of the segments saw lower contributions to net income, how could net income rise? It was because Q2 saw a $135 million loan loss provision increase. In Q3, there were no provisions which is a big benefit. So, we need to watch performance here, but we are looking out to 2021. And that is why we see shares rising.

The bank's efficiency

As we have said in our coverage of other major financial institutions, the efficiency ratio is important to watch. We continue to argue that the strongest banks have an efficiency ratio under 60%. BOK Financial's efficiency ratio has long been strong. This quarter was a bit weak, with efficiency rising from Q2's 59.6% from 60.4%. That said, the bank saw a much better efficiency from last the start of the year, which was 63.7%. Keep an eye on this metric, but overall it is still strong. We will also point out that the return on average assets and equity both bounced back in the quarter coming in at 1.25%, and 11.89%, rising dramatically from Q2 on these metrics, which were 0.52% and 5.14%, respectively. We suspect the bottom is in performance wise, and while loan growth will be soft for the next few months as the COVID winter hits, we think there will be a strong 2021 ahead.

Paid to wait for a rebound

BOK financial has been a consistent dividend raiser. With the recent increase in shares, the forward yield is now 3.0%. In our opinion this is a respectable yield to be paid to wait for continued upside. What we think is more important is that the dividend itself has grown every year, and we see increases as likely going forward. We expect the dividend growth to continue. We think there will be continue raises.

While past performance was strong in Q3, 2021 looks great. Earnings are expected to increase at least 10% next year. The expected earnings increases are attractive if you want to buy. When we couple this with the fact that we expect the portfolio to improve moving forward particularly in the COVID-impacted sectors, it is likely that we see sizable book value expansion going forward. Book value last hit $74.23, and has been increasing all year. Tangible book value has also risen, last notching gains in Q3 to $57.64. Thus, we like a buy on a pull back to $65, which the market is likely to offer on the next selloff.

Take home

We see earnings remaining positive, and believe the biggest risks in the portfolio are becoming less of an issue. Loan deferrals are well off their highs. The outlook is improving for energy and retail, which BOK Financial has a lot of exposure too. The dividend yield is respectable, and the bank is operating well. If shares dip under $65, this would be well below book value and just above tangible book. Consider buying for a rebound in 2021.

If you like the material and want to see more, scroll to the top of the article and hit "Follow."

Holiday Month Special: Secure Your 65% Off Discount Now

Like our thought process here? Stop wasting time and join the community of 100's of traders at BAD BEAT Investing at an compounded 65% discount versus the regular monthly rate!

- Full access to an expert team of 5, available all day during market hours.

- Rapid-return trade ideas each week

- Target entries, profit taking, and stops rooted in technical and fundamental analysis

- Monthly deep value situations

- Stocks, options, trades, dividends, and member portfolio reviews

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in BOKF over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.