SIFCO Industries Is Boring, Safe, And Cheap

SIFCO's revenue, earnings, and book value haven't meaningfully changed over the last decade.

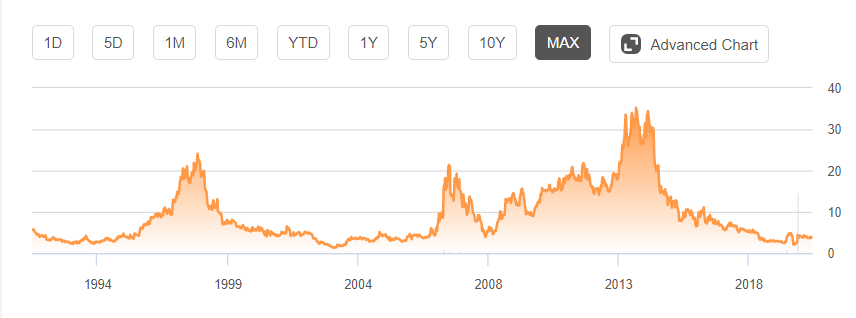

The company's valuation, in contrast, has fluctuated wildly.

SIFCO earned $1/share in 2014 and traded at a PE of 30; SIFCO is on track to earn $1/share in 2020 and is trading at a PE of 4.

I'm not a market timer, but I suspect SIFCO will trade at a higher earnings multiple in the next five years.

The company's balance sheet and historical performance offer an adequate margin of safety.

![]()

(Source: SIFCO)

The Elevator Pitch:

SIFCO Industries (SIF) is a microcap manufacturing company that the market doesn't seem to know how to value. Over the last 30 years, the company has been a 10-bagger three times and subsequently lost 75% of its value three times. The company is highly cyclical and is touching the bottom of a seven-year rotation. In fiscal year 2014, SIF earned $1 per share in net income and traded at a PE of 30 at the end of the year. In 2020, the company is on track for a similar $1 per share in earnings and is currently trading at a PE of 4. Despite the volatility in share price, the underlying fundamentals of the company have not changed dramatically in the last decade; results have been lumpy, but the company has averaged $3.5 million in annual free cash flow over the last twelve years. I am not a proponent of market timing, but history suggests that SIF will trade dramatically higher sometime in the next 3-5 years; I am considering starting a small position to take advantage of the sharp swings in investor sentiment.

Company Background

With all due respect to SIF, their business is boring. Founded over 100 years ago, the company manufactures turbines, turbine blades, and other aerospace components for military and commercial aircraft. Like clockwork, the company generates somewhere between $80 and $120 million a year in revenue, either earns a small profit or incurs a small loss, and generates a little bit of cash flow. Despite multiple acquisitions, dispositions, write-downs, and attempts at product diversification, the company's financials are virtually the same today as they were in the late 90s. Margins are slim in both good and bad times, with any given year's performance being determined primarily by the mix of contracts they receive (the breakdown of commercial vs. military revenue has stayed within 40-60% for the last decade or so). I see no evidence of pricing power in the company's financials, nor much of a moat around their product offerings, but SIF certainly has staying power and has been able to weather all the economic storms it has encountered thus far. Heck, the company made it through the Great Depression and turned a profit during the Great Recession.

Despite heavy exposure to the commercial airline industry, 2020 has been a good year for SIF. The company is on track to earn about $1 per share in net income for the year and $.50 in operating cash flow, against a share price of $3.90 at the time of this writing. Gross margins have improved significantly compared to 2019, with the improvement coming from both increased revenue and decreased expenses. SIF's balance sheet is in good shape, with a $41 million book value that includes brand new aluminum forge equipment in Orange, CA (the previous facility was destroyed in a fire in 2018; the new facility is running at 75% capacity and on track to be at 100% capacity by the end of the year). The company has steadily been decreasing its debt load since 2015 and pays only ~3.5% interest on its current balance of $12 million.

The Investment Opportunity

In contrast to SIF's financials, the company's valuation has fluctuated wildly over the last 30 years:

(Source: Seeking Alpha)

SIF has been a ten-bagger three times in this time frame, but has subsequently lost 75% of its value three times as well. Despite a relatively stable (if unimpressive) baseline, the market can't decide on an earnings multiple to assign the company. As case studies, consider that in 2007 the company earned $1.25 per share and received an earnings multiple of about 20, while the very next year the company earned $1 per share but received an earnings multiple of 5 despite having done well through the 2008 financial crisis. In a similar fashion, SIF brought in $1 per share in net income in 2014 and the market was willing to assign an earnings multiple of 30; the company is on track to earn that same $1 per share in 2020 and the market is currently assigning an earnings multiple below 4. The company reported negative earnings from 2016-2019, which explains some of the drop, but the company also generated $30 million in operating cash flow during that period and the company's share price is flat year-to-date in 2020 despite a solid return to profitability.

I am by no means saying that SIF is an outstanding company that I would want to hold for the long term, but it is clear that the market swings wildly between optimism and pessimism when it comes to the company's prospects and we are currently in a period of near-peak pessimism. Despite improving margins and solid earnings, the market appears to be overly concerned about the last five years of underperformance and has been slow to recalibrate in 2020. History suggests that this is a regular occurrence and I believe there is an opportunity to buy shares cheaply today and sell them for a considerable profit when the market swings back to an optimistic outlook for the company.

Setting a precise price target is difficult; it is entirely possible that SIF once again becomes a ten-bagger from these levels, but given the company's history of steep and abrupt declines, I don't have the stomach to hold the stock up to that level. I am happy to set a price target somewhere around $10 per share and take a 150% gain on my investment, even if the thesis takes multiple years to play out. A $10 price target supports a price to normalized free cash flow ratio of 15, which I think is a bit rich but not unreasonable.

Risks and Margin of Safety

Like many value investments, the SIF investment thesis relies heavily on the market assigning the company a higher earnings multiple. The largest risk is that the market decides to remain pessimistic about the company's prospects and does not assign a higher multiple. SIF also has a high level of customer concentration, with their four largest customers accounting for 50% of revenue in 2019. Finally, SIF has a net-debt position on their balance sheet and could face short-term liquidity issues if operations take a big step backwards. That being said, SIF is trading at a 50% discount to book value and has machinery assets of over $30 million; in a pinch, equipment could be sold to meet short-term debt obligations. The company also has about $20 million remaining on their credit revolver, which can be borrowed at an interest rate of only LIBOR + 1.5%. Finally, I think SIF's pedigree and ability to stay in business for over 100 years speaks to their resiliency. If the company had to liquidate today, I think they could get at least 50% back on the value of their assets and leave investors with a break-even scenario.

Conclusion

SIF is a mediocre business trading at a very cheap price. I am willing to start a small position at these levels to try and take advantage of the disconnect between the company's recent performance and investor sentiment. SIF is a tiny company (the current market cap is less than $30 million) with an average daily trading volume of less than $30 thousand that won't be investable for all readers, but if you can buy small companies, I think SIF is worth a look. I am planning to set a price target around $10 per share and be willing to wait up to 3-5 years for the thesis to play out; if it hits that level sooner, all the better. The company's balance sheet offers an acceptable margin of safety in case of disaster.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in SIF over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This article should not be taken as financial advice, it is only an expression of my own opinions as an individual investor