Investing In The Post-Pandemic World - An Update

The financial markets are anticipating the end of the pandemic as a result of the successful vaccine trials.

Comparisons involving the post-WWII period and the coming post-pandemic period may be useful.

The federal budget deficit will exceed $3 trillion yearly in 2020-2021, and debt-to-GDP ratios are approaching the prior WWII-induced peak.

During WWII, the surge in federal government spending was for defense-related goods and services. The pandemic-related federal government spending was mostly for transfer payments.

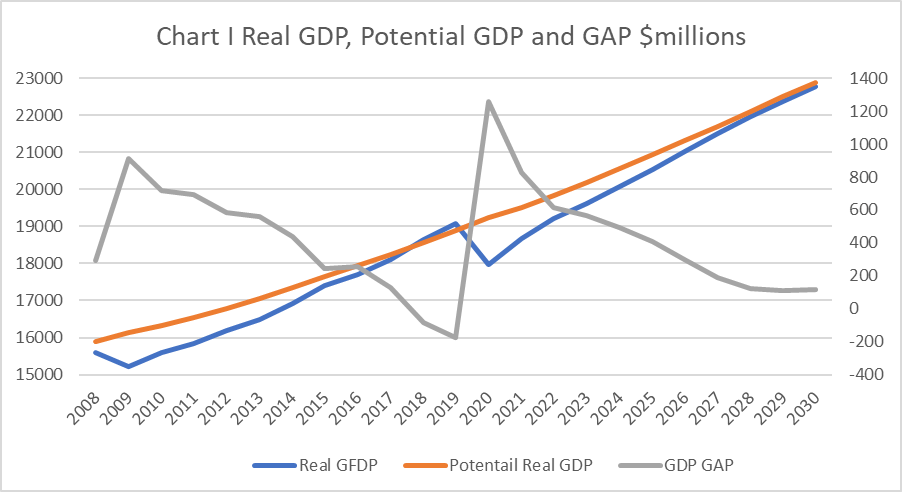

The gap between actual GDP and potential GDP will likely close very quickly in the post-pandemic period. In contrast, that gap lasted until 2018 after the 2007-09 recession.

As the endgame of the COVID-19 pandemic approaches, financial markets are busy sorting out the characteristics of a post-pandemic society. To date, the consequences of the enormous debt incurred to fight the pandemic is not getting attention, but it eventually will. Ironically, during the entire post-World War II period, business cycles have largely been defined by swings in the goods-producing economy, while the services sector enjoyed uninterrupted secular growth. This time, the goods economy has been remarkably resilient in 2020, while the bulk of the pandemic-induced disruption was and still is in the services sector.

There is no comparable historical analysis to fall back on. However, in terms of the massive increase in government debt incurred to fight the pandemic, an examination of World War II and its aftermath may be useful. All the countries that fought in World War II borrowed significant portions of their respective GDP to finance the war effort. This debt was resolved in the three ways that excessive sovereign debt is typically resolved: some countries, like the USA, grew their way out; some countries, like the UK, inflated their way out; and some countries, like the Axis powers, defaulted on their debt.

Focusing on the USA, similarities between the war and the pandemic are striking. American combat deaths from World War II totaled 291,557. To date, American deaths from COVID-19 are about 272K and counting. World War II was a war pitting human against human, while today, the war is between humans and a virus.

The culmination of WWII became apparent on July 16, 1945, when the technology of the first atom bomb was successfully tested in New Mexico. The endgame of the COVID -19 pandemic became apparent on November 9, 2020, when the technology surrounding the first successful trial of an mRNA-based vaccine was announced. This novel technology, which had never been successfully used to develop any vaccine, was used to create at least two new vaccines. The fact that they demonstrated 95% efficacy against the virus is an added bonus.

Back in the day, there was considerable doubt that atomic bombs could be deployed in a way that would end the war. While the atom bomb was being dropped on Hiroshima, planning was well underway for Operation Downfall, the two-part invasion of Japan that was scheduled to begin in November 1945. The staff of War Secretary Henry Stimson estimated that invading Japan would result in 1.7-4 million American casualties, including 400K-800K fatalities. Even after the bomb was dropped, the American military doubted Japan would capitulate. It was estimated that at least seven more bombs would need to explode during the invasion.

Like then, there is considerable uncertainty that the SARS-CoV-2 virus will join the polio and smallpox viruses, as losers in the conflict between humans and science. The aftereffects of the vaccination are largely unknown, and thus, striking fear in the minds of many potential recipients. There is thus uncertainty about the degree to which the vaccine will be accepted by the general public until a successful track record can be demonstrated. And there is a cohort of so-called anti-vaxxers that would abstain regardless of its effectiveness. That being said - and these concerns are real - we would be first in line to receive a dose when we are eligible.

While the humanitarian comparison between WWII and the pandemic are similar, the financial and economic effects are much different. In WWII, the federal government debt-to-GDP peaked at about 119% in 1946, and in 2020, the pandemic-induced debt-to-GDP ratio will approach 100%. In WWII, federal spending was mainly for goods, especially for military hardware. This caused both nominal and real GDP to increase sharply, ultimately exceeding the economy’s potential GDP, and thus creating a positive output gap. The output gap being defined as the difference between potential GDP, which is the economy’s noninflationary growth rate at full employment, and actual GDP.

In contrast to the war period, most pandemic spending has been mandatory in the form of income security programs. With dispatch, the CARES Act legislation became law in the spring, appropriating $4 trillion for expanded unemployment benefits, small business rescue loans, etc. to counteract economic effects of the pandemic. In September 2020, the Congressional Budget Office (CBO) pegged the 2020 federal deficit at $3.3 trillion versus $984 billion for 2019. Total federal outlays were estimated at $6.6 trillion versus $4.4 trillion in 2019. Of this $2.2 trillion increase, mandatory programs were projected to absorb $1.9 trillion, or most of the increase.

Mandatory spending - i.e., transfer payments - does not cause a direct immediate increase in GDP. Indeed, CBO and private forecasters estimate that nominal GDP will fall to about $20.6 trillion this year from $21.4 trillion in 2019. And real GDP at the current year end is likely to be about 5% smaller than it was at the cyclical peak of last year’s final calendar quarter.

While the bulk of this mandatory spending increase was not for goods or services, it will gradually find its way into the spending stream. Indeed, the first-order effect was to raise the aggregate household saving rate to a historically high 33% in April, as income support was joined by a collapse in spending. The savings rate has been declining steadily as spending is recovering, and in October, it stood at a still extremely high 13.6% of income. A key question going forward surrounds the timing and the degree to which the savings rate will revert to its pre-pandemic norm of about 6%, and the degree of upward pressure it will eventually exert on resource utilization.

The end of the pandemic may be in sight, but a new wave of infections is in progress and is threatening renewed disruptions in economic activity worldwide. Last spring’s first pandemic phase caused the nation’s and the world’s aggregate supply and demand curves to contract, leaving a huge void between actual output and potential output as shown on Chart I below. The current second phase of the pandemic will not be nearly as severe, but it is before economies have had a chance to recover from the first shock of last spring.

History is replete with examples of significant declines in both aggregate demand and supply. In the fourteenth century, Europe fought the Black Death of bubonic plague, which decimated about one-third of its population. In its aftermath, wages for the majority of workers surged. The amount of tillable land owned by the aristocracy remained steady, while the supply of workers to till the land was reduced. The result was inflation.

Toward the end of WWII, a post-war depression and deflation were widely forecast, as the supply of new civilians was thought to overwhelm the labor market and exert downward pressure on wages and income. As it turned out, though, the vast amount of pent-up demand that was deferred during the war was financed by the government’s “52-20” legislation, which provided unemployed veterans with $20 per week for 52 weeks.

This stipend, combined with a wartime build-up of household savings, unleashed spending upon the war’s end. This spending was concentrated on durable goods and fixed investment, boosting both actual and potential GDP. About 7500 electronic TV sets were produced in the USA before the War Production Act halted manufacture in April 1942. Production resumed in August 1945, and whereas only 0.5% of households owned a TV in 1946, 55.7% owned one in 1954 and 90% were owners in 1962. These TV sets went into new homes, a component of fixed asset investment, as a housing boom was financed by a vast expansion of veterans’ loans. Meanwhile, factories were retooled to produce civilian goods, boosting the country’s capital stock.

So, the war precipitated a decline in both aggregate demand and supply, but post-war deflation was avoided by timely federal stimulus. And post-war inflation was largely avoided as the economy grew its way out of the debt overhang incurred in the war effort, such that the output gap never went negative. The USA experienced a positive output gap in the 1970s. Combined, oil and agricultural shocks increased costs and boosted food and fuel prices. This contributed to a wage price spiral that stifled aggregate demand and elicited a decade of stagflation.

More recently, an output gap occurred between 2000 and 2006 as an outgrowth of a recession, terrorist attacks and an undeclared war. The gap closed between 2006 and 2008, but then opened up again during the financial crisis as shown on Chart I. The gap lasted until 2018 as the economy endured the weakest recovery of the post-war period. Thus, inflation was constantly overestimated by many.

As we eagerly anticipate a post-pandemic environment, the interaction of aggregate demand and supply will be crucial. They will be a function of consumer and business psychology more so than finances. The duration of currently expansive monetary and fiscal policy will also be key.

As noted earlier, economic distress has largely been in the services sector, particularly education, entertainment, and travel and leisure. From this year’s third calendar quarter back to last year’s final quarter, real GDP fell by 3.5%. Personal consumption of goods rose by 7%, while services consumption declined by 7.8%.

It could be said that much of the excess saving that has been accumulated was from declining services consumption. For those whose income was maintained, there was nothing to spend it on. But once the pandemic is licked and vaccination is widespread, this deferred demand will be unlocked and trips to Disneyland, movie theaters, etc. will recover. To what degree, is a question. And we would argue that health concerns are likely to vanish slowly; social distancing is likely be a new normal; and new technologies will result in permanent shifts in behavior, whether it be remote work and learning or preferences for suburban versus urban living.

On the business side, investment decisions will also likely be skewed by the experience of the pandemic. Currently, business has no liability shield against virus-related workplace claims from customers or employees. This could be an impediment to full re-openings and, perhaps, new business formation.

Cost structures are also likely to be permanently affected. A by-product of the pandemic is a sharp reduction in fossil fuel demand, and thus, low energy prices. But as the late T. Boone Pickens would quip, the lower the price, the less you are likely to get of it. In 2014, the active drill rig count peaked at about 1600 units. In 2019, a secondary peak occurred at about 960 units, and currently, only about 240 rigs are in operation domestically.

This will directly and negatively impact production going forward, as will parallel declines in exploration and production budgets. Meanwhile, the incoming Biden administration does not hide its preference for renewables versus fossil fuel, so non-economic impediments to production are probably likely.

All else equal, domestic energy prices will likely rise from these developments on top of a post-pandemic demand recovery. But market power will likely gradually shift back to foreign producers; fossil fuel exports from the U.S. will gradually diminish; and consumer preferences will gradually change. To be sure, the renewables industry is likely to expand, even though renewables are a less-efficient energy source than fossil fuel, which means higher costs overall. And since renewables, i.e., wind, solar, and electric, are very intensive users of commercial metals, the entire commodity complex could see rising prices, putting added pressure on the business users of such commodities. How all this shakes out in a post-pandemic world is interesting and very speculative, although a look at recent trends in energy, copper, and lumber prices - to name a few - shows that markets are already registering their vote.

When policy preferences replace market dynamics, the result is usually lower productivity and higher business costs. Whether these translate into lower profits or a higher general price structure then becomes a function of the monetary and fiscal backdrop.

Both monetary and fiscal policy have been highly expansive during the pandemic. The federal budget deficit will exceed $3 trillion yearly in 2020-2021, and this is being monetized, as monetary growth is in excess 20% yearly. Moreover, additional fiscal stimulus is a priority of the new administration and it is at the behest of the Federal Reserve as well. With approximately 10 million workers still unemployed because of the pandemic, only the magnitude of more fiscal stimulus is a matter of debate.

Meanwhile, the Federal Reserve is vowing to continue an aggressively easy money policy beyond the end of the pandemic. But we know that monetary policy works with long and variable lags. And to date, while it has help stop hemorrhaging in the economy, its effectiveness has been blunted by a collapse of money velocity. In a post-pandemic world, money velocity could be expected to recover, albeit to an unknown degree, and unless monetary policy becomes less expansive, the result will be a surge in economic activity.

With the appointment of Janet Yellen as the new treasury secretary, there is no reason to expect pressure on the Fed to scale back accommodation. Indeed, considering the sorry state of fiscal finances and the Treasury Secretary’s reputation, we would expect the pressure for continued monetary accommodation to linger or even intensify. CBO is projecting the economy’s potential GDP growth path at about 2% yearly for the current decade. Consensus estimates are that actual GDP growth will be about 5% in 2021. Given current and likely monetary and fiscal policies, it would not be unreasonable to expect about 4% growth in both 2022 and 2023. In this scenario, the current output gap would disappear in 2023 and probably be negative in 2024, with the risk of bottlenecks and inflation.

How soon long-term bond investors would be willing to tolerate this is an unknown, but already there are rumblings as long-term interest rates hold above their recent historic lows and as the dollar exchange rate weakens. In the near term, we have no doubt that the Treasury and the Fed will operate in tandem to hold down long-term rates to support economic recovery. But by the time economic recovery is firmly in progress and continued accommodation is no longer urgent, the inflation genie may already be out of the battle.

For the past eighteen months, the Fed Chairman and his immediate predecessor have been promoting growth over inflation. Having been so wrong about inflation over the past decade, it is now proclaimed to be a brave new world. It is early in this new world, but our view is that policymakers should be careful what they wish for, because they may well end up getting it.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Please note that this article was written by Dr. Vincent J. Malanga and Dr. Lance Brofman with sponsorship by BEACH INVESTMENT COUNSEL, INC. and is used with the permission of both.