Cantel Medical: Further Upside Driven By Infection Control Consumables

Cantel Medical has the legs to reach historical growth levels over the coming periods, backed by a strong Q4 performance.

Q1 pre-announcements have indicated a stronger than expected sales recovery, and growth cadence has outpaced initial projections.

Key exposure to infection control consumables, backed by COVID-related demand, should fuel sales growth well into 2021.

Cost-targeting and liquidity preservation measures since Q3 have fortified the balance sheet, and taken pressure off operating leverage.

Shares are trading at respectable multiples, and we believe that further upside is likely based on a price target of $85-$87 in the blue-sky scenario.

Investment Summary

We are of the firm belief that Cantel Medical (CMD) has the legs to return to historical growth levels, whilst adding to margin growth over the coming years. Our thesis is backed by a strong Q4 performance and equally weighted by strong Q1 performance, evidenced by the pre-announcement showing the same last month.

Data Source: Author's Bloomberg Terminal

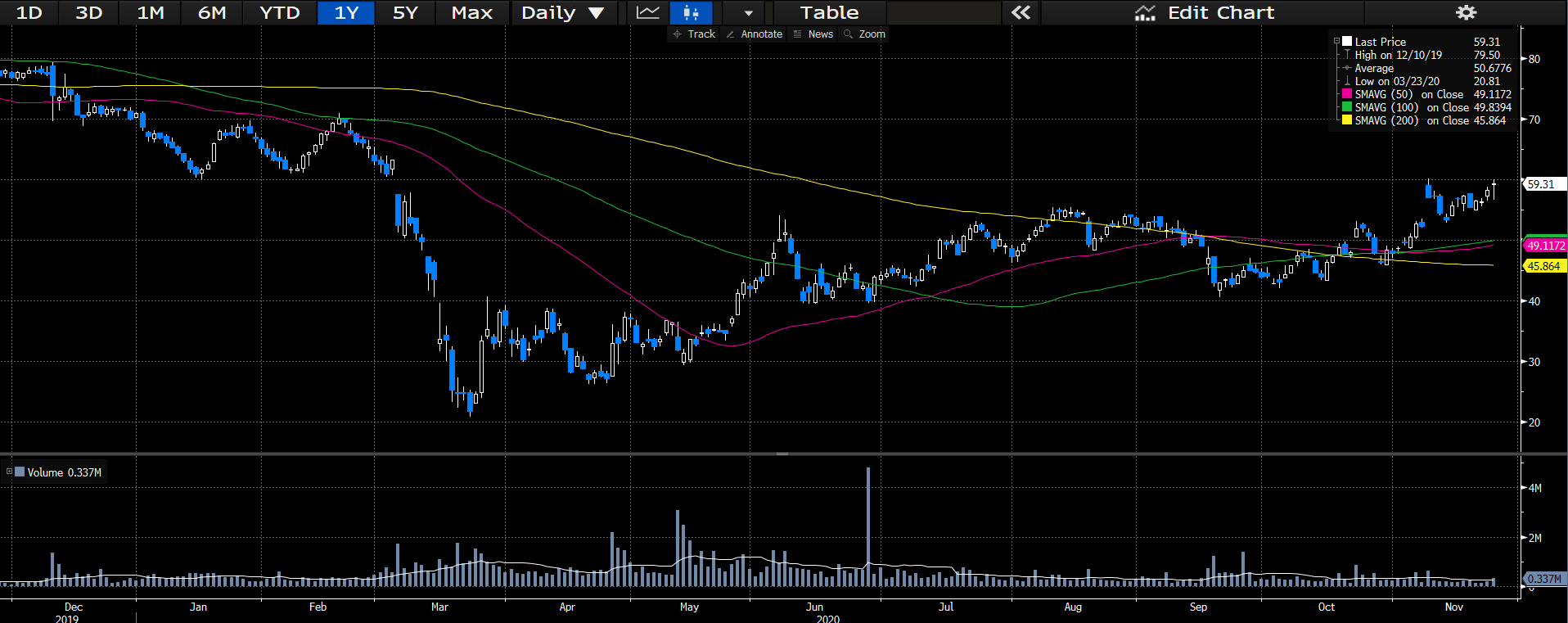

The infection control player will continue to leverage its exposure to COVID-19 and the narrative surrounding infection control moving into 2021 and beyond. Long term, we see a recovery towards 2017-2018 share levels, driven by consumables-led demand and unique market positioning. Here we link performance at the back end of 2020 to valuation and the long-term outlook of the company.

Strong Performance In The Back End of 2020

CMD have already released the pre-announcement for F1Q1 performance back in late October. Here, we've observed top-line earnings of $290-$295 million on a sequential growth pattern of 25% from Q4, coming in well above the consensus of ~$260 million. The results from the pre-announcement indicate that CMD is on a current run rate of just over $1 billion on annual revenues, which is a stellar outcome. The above figures also show a 14% YoY increase, which attests to CMD's performance this year. Management were eager to highlight that the underlying procedures in its medical and dental segments have recovered far quicker than first expected. Underscoring the performance this quarter has been the sustained demand for infection control consumables, likely via COVID-related tailwinds. Management have also held tight to liquidity preservation measures across the latter half of the year, which will drive growth to the bottom line also coming into 2021. We can expect the full release of FQ1 2021 results in early December.

Turning to Q4 results, performance at the top came in line with consensus, and organic growth had slowed to ~18%, although still an ~7 percentage point sequential increase quarter/quarter. COVID-related headwinds were apparent in the medical, dental and life-sciences segments, which have already been offset with Q1 performance as outlined above. Additionally, management highlighted to us that medical and dental average daily sales were at a higher cadence than first anticipated, and that utilization had already reached up to 85% of pre-pandemic levels by that point, thus, may already be back towards the 100% mark by now. Segmentally, medical was the key takeout from Q4, with ~$103 million in contributions across the quarter, whilst dental sales grew 21% YoY with a ~$75 million contribution to the top.

The dialysis segment was less affected by COVID-related headwinds, posting 21% YoY growth. This was probably from the applicability to off site treatments, and the necessity as an essential treatment. Operating leverage faced pressures across Q4, with a ~450bps headwind from deleveraging and COVID challenges, however, strong cost-targeting measures offset the full magnitude at the operating level. Gross margins therefore came in strong also at ~44%, helped by the top-line expansion and cost-targeting employed from Q3. An example of the cost savings was seen in R&D contraction, which came in at 3.6% of revenues, and was down ~1% YoY. Thus, the company ended the quarter with ~$280 million in cash, on a long-term debt load of $945 million, and ~$170 in convertible notes, which resulted in net leverage of just under 7x.

CMD also provided some color on its Cantel 2.0 program, saying that they have reconfigured the sales force in the US, which includes a new emphasis on selling the "Complete Circle of Protection", thereby including an entire scope of personnel in the field. These include hospital reps, an ambulatory surgery center, a full sales and marketing team, and beefing up internal sales capacity. This is coupled with the company consolidating many sites across the EU and the Middle East, alongside its German arm.

Therefore, it seems the headwinds that the medical and dental segments faced from COVID-19 have begun to diminish, and we believe that the company will return to its mid single-digit growth pattern by the end of this quarter. Interest expense remains covered by ~3x, down from the 14x coverage a year ago, whilst equity to assets remains at 35%, down from over 60% YoY. Debt to total capital is around 60%, although the company managed to pay down ~$75 million of the revolving facility in Q4, with more contribution likely in Q1. Accounts receivable turnover decreased slightly to 6.88x on the full year results, whilst the number of days for outstanding sales increased by around 1 day to 53 days. Inventory turnover was relatively flat, but the number of days inventory outstanding increased by 5 days to 96 days. This has impacted the cash conversion cycle which now is at ~125 days, an increase of ~1 week. These are the measures we will be heavily scrutinizing from the full Q1 release in early December, drawing comparisons on sequential performance.

Outlook Builds On Q1 Performance

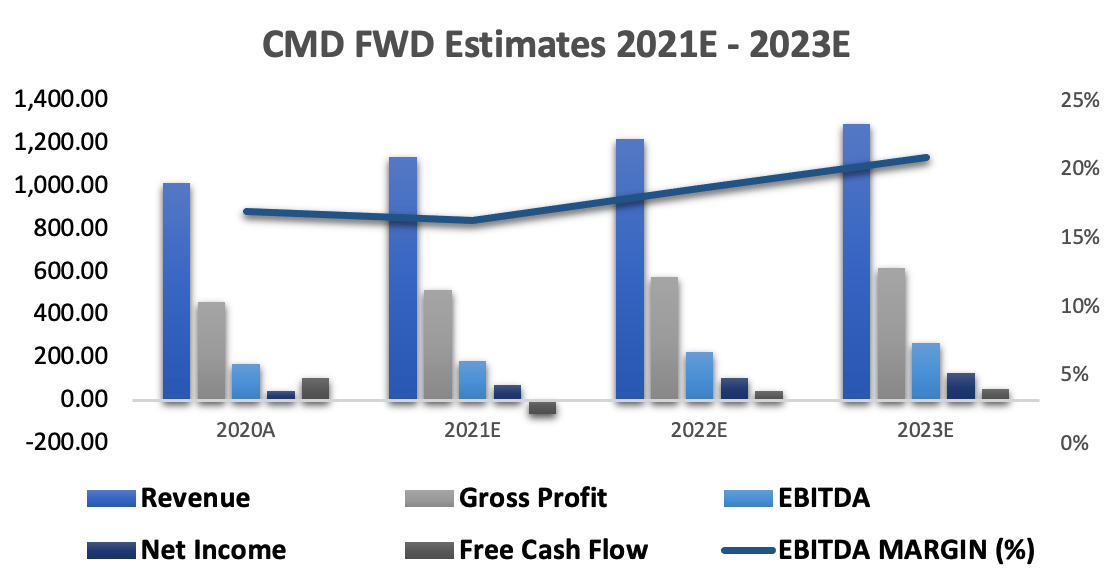

At the base level, we would forecast segmental revenue growth in the mid single digits over the coming 3 years, where the company expands on the strength in medical and dental, and sees growth at the operating level. We would foresee the current sales trajectory sustained over the coming quarters, and that management will continue in cost-targeting and liquidity preservation measures. We also foresee margin growth at the top and EBITDA levels over the coming 3-year period, alongside a sequential growth pattern in revenues and EBITDA over this period also. We do foresee free cash conversion taking a hit, with some of the cost-targeting measures and expansion of the salesforce, however, see a recovery by 2023 at 4% of turnover. Below, investors can view our base case assumptions, which have been outlined above.

Growth into 2023 at the top, free cash conversion will take a hit from cost-targeting and labor expansion, 4% of turnover by 2023:

Data Source: CMD SEC Filings; Author's Calculations

EBITDA margins improving, coupled with gross margin expansion over the next 3-years:

Data Source: CMD SEC Filings; Author's Calculations

Valuation

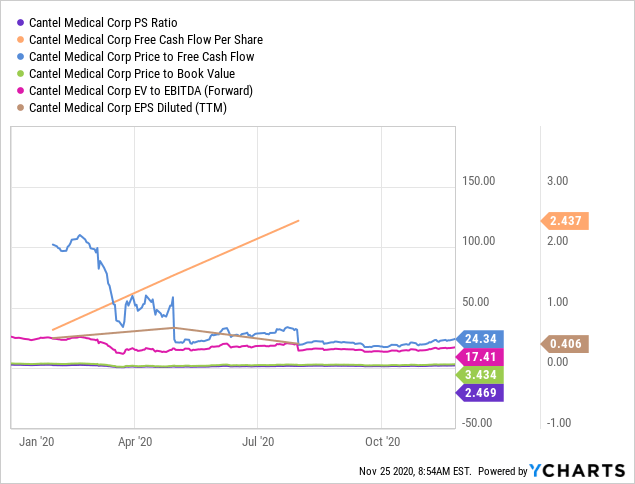

Shares are trading at ~25x free cash flow, and 57x P/E. Trading at ~3.4x book value signals decent value creation for shareholders, albeit at a reasonable standing relative to peers. Shares are also trading at ~27x Q4 EBITDA on a TTM basis, and we look forward to modelling EV/EBITDA progression in December at the earnings release. The company has roughly $2.40 in free cash per share, ~$7 in cash per share and over $24 in revenue/share, backed by ~$67 in EV per share. Considering these multiples and per share measures, we believe that the market may be under-reflecting CMD's inherent value at the current market price of $59. We are especially firm on this belief considering the strong sales recovery given in the Q1 pre-announcement, that may not yet be realized by the wider market.

At the base level, we believe that CMD commands a premium on YTD performance and the strong rebound in Q1. Thus, assigning a 1.5x premium to our forward P/E of 37x, and reflecting this to our 2021 EPS estimate of $1.54 we see a price target of $85 on today's trading in the upside case. Withholding the premium, and using today's 57x P/E to 2021 EPS estimates, we see a price target of $87 using the same methodology, ~46% upside on today's trading (subject to change with publication times). Thus, we believe that there is significant upside potential in CMD over the coming 12 months, that is already backed by Q1 performance.

Data by YCharts

Data by YCharts

Therefore, we also believe that CMD presents as a value proposition, where the underlying value may yet to be reflected in market pricing. In this vein, we look forward to the Q1 results in December to support this thesis.

Further Considerations

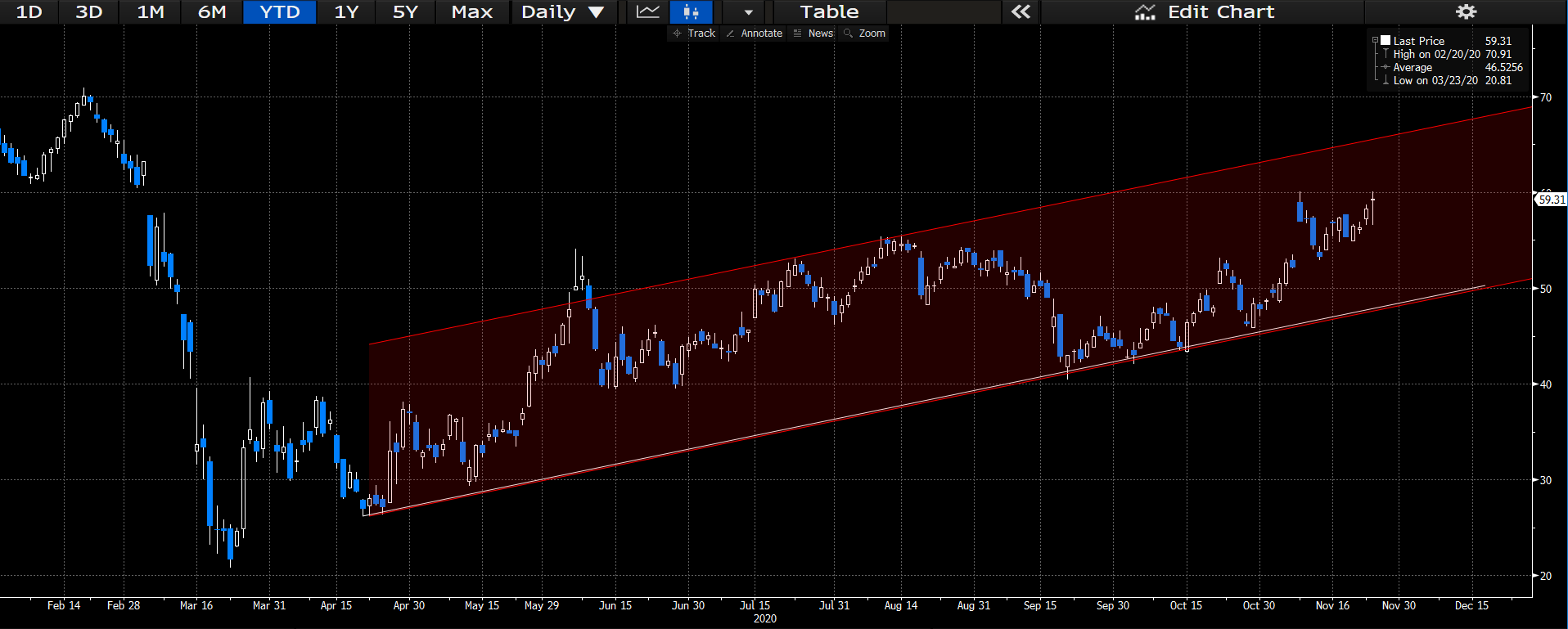

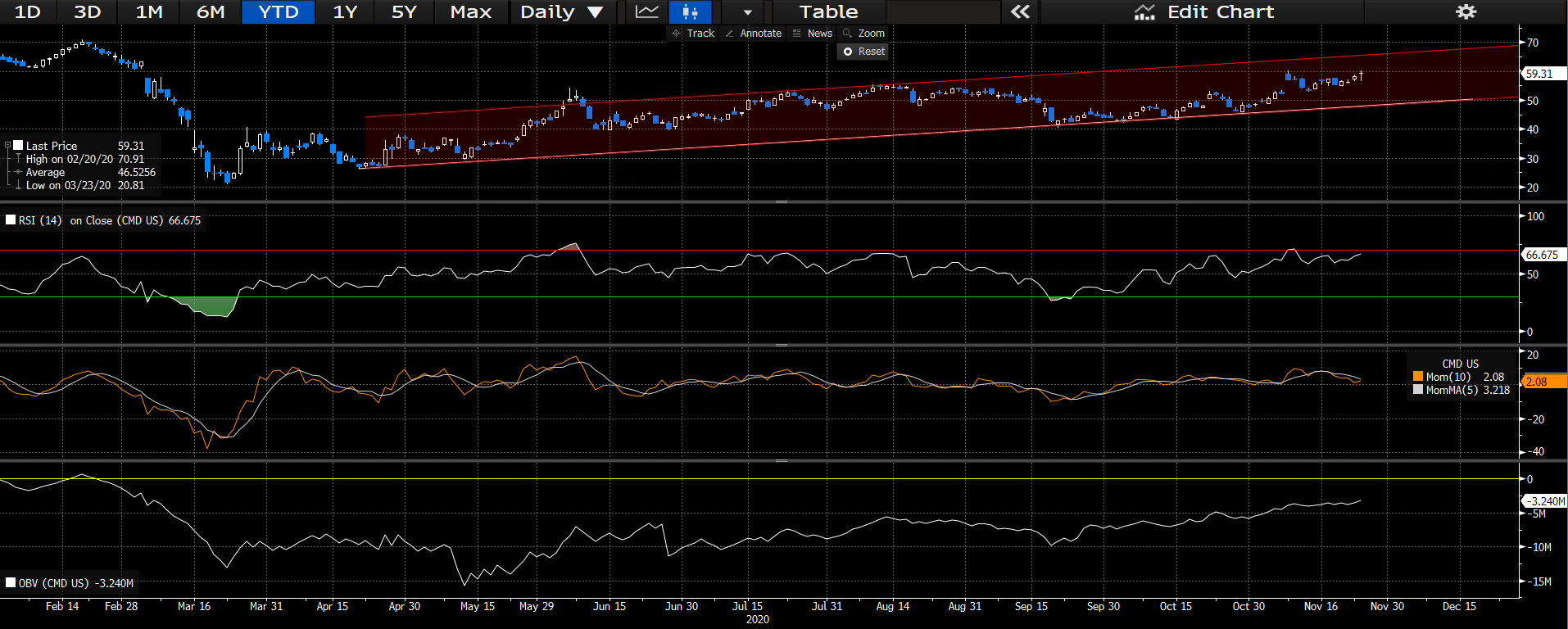

On the charts, shares have trended in an ascending channel since the selloff in March. Support has been defined since then, having broken away in October from the sawtooth pattern that had ensued since September. Shares have only broken the resistance level once back in May, and are approaching that level once again at the current trajectory. Investors can see this pricing activity YTD on the chart below.

Data Source: Author's Bloomberg Terminal

Momentum has remained relatively high and stable across this year, in keeping with the longer-term trend. Shares have just breached into overbought territory back in early November, however, have maintained on the up since, which is a good sign. There has been a decent causal relationship between RSI ranges, momentum and price outcomes on regression analysis, backed by the on balance volume making a gradual climb back since May. Investors can view these causal relationships on the chart below.

Data Source: Author's Bloomberg Terminal

In Short

CMD is in the early to mid stages of a strong sales recovery, evidenced by the Q1 pre-announcement last month. Here, management have highlighted strengths and better than expected results across all segments. The company left Q4 well capitalized with ~$277 million in cash, and have over 3.5x coverage on short-term obligations from liquid assets, plus adequate coverage at the cash level. We see further upside on today's trading based on our valuation, and believe that CMD presents as a value proposition, where the underlying value may not yet be reflected in market prices. We therefore set a price target of $85-$87, which signals just over 46% upside on today's trading. Additionally, we see strong sales growth over the coming 3 years, however free cash conversion may take a hit over this time period, with cost-targeting measures and labor force expansions.

In view of the healthy performance outlined, management have also given some color on the Cantel 2.0 program, which is already showing signs of life and benefit to the numbers. In addition to the measures undertaken this year to deal with COVID, the company will likely realize further upside over the coming periods, with demand for infection control consumables driving the underlying growth in that segment. This fits the current narrative in society at the moment, plus legislature and workplace policy will likely reflect this demand over the coming year at least, as the economy slowly reopens. Challenges to our thesis include the fact that end markets may suffer ongoing turbulence over the coming periods, and that demand for infection control consumables may come in weaker than expected. Therefore, we are cautiously optimistic with these things in mind. In any sense, we see further upside in this company, and look forward to providing additional coverage.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.