The Cooper Companies: Lumpy Sales YTD Offset By MiSight Potential

The Cooper Companies has had a lumpy year in terms of sequential growth and exposure to COVID-19.

Initially, it was thought that contact lens markets would remain insulated from COVID-19, but results YTD highlight the portfolio's exposure to the pandemic.

Q3 sales made a decent sequential recovery, although all came in lower on a YoY basis.

The MiSight segment has promise, with management claiming a $5 billion global addressable market in myopia-related treatments in this segment over years to come.

Based on tangible figures, we see a price target of $332, meaning long-term prospects may already be priced into the valuation.

Investment Summary

From lumpy results this year, The Cooper Companies' (COO) exposure to COVID-19 has been detailed, and the effects are more pronounced than initially estimated. COO had modeled projections based on the assumption that their core operating segments, in particular contact lenses, were immune to the effects of the pandemic. However, patient volumes and new patient uptakes have been weakened across the course of this year, compounded by reduced utilization of instillations of existing placements.

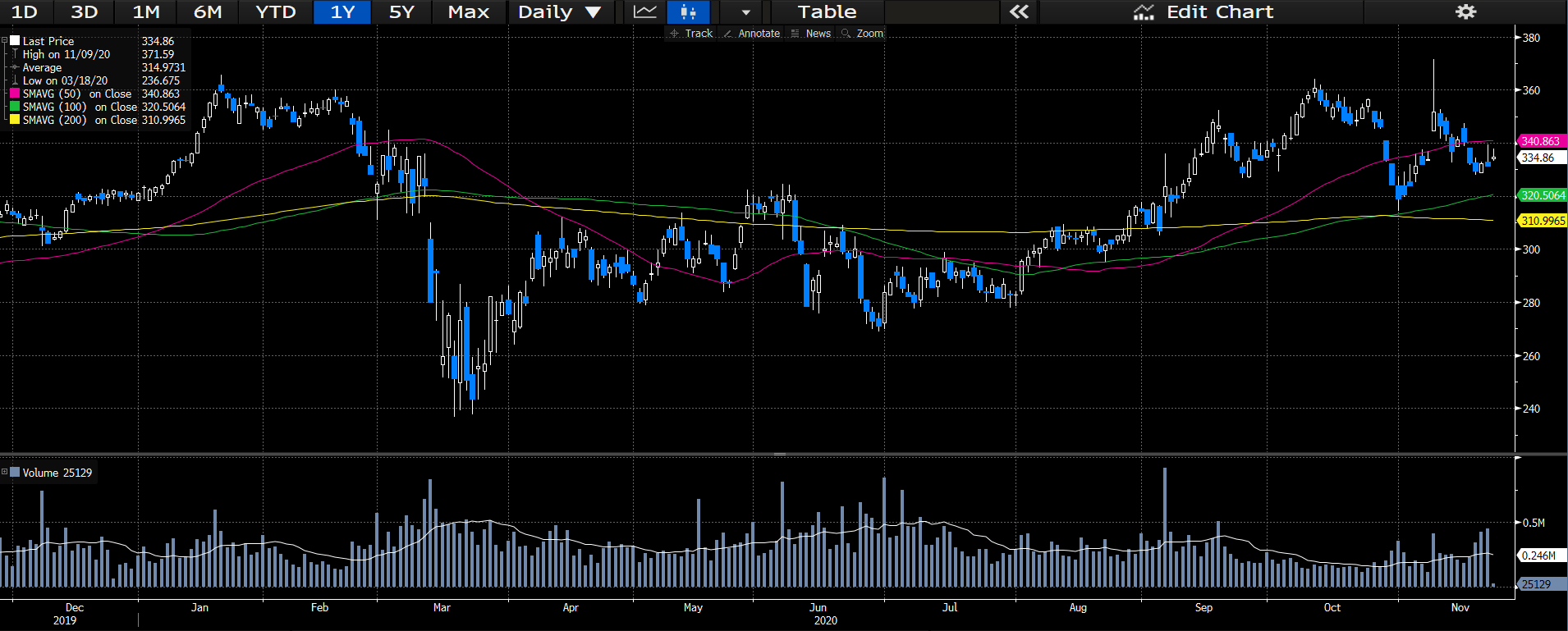

Chart YTD

Data Source: Author's Bloomberg Terminal

Extracting these COVID-19-related headwinds, it is clear that the lumpy performance has been backed by non-operational items on the income statement, and management have provided little savior in their outlook for expenditure requirements over the coming periods. Offsetting these points is the asset potential in MiSight, which could provide a remedial breakthrough in myopia, and reach a potential addressable market of around $5 billion over the coming years. With a high probability of conversion, the future value of this segment adds a positive skew to the distribution of returns in years to come. Thus, although the business model should make a recovery in the turnout of patient volumes and utilization of instillations, we hold a neutral view until we see greater evidence of performance in the core business, with or without COVID-19-related headwinds.

Q3 Walkthrough Gives Weight To COVID-19 Exposure

COO posted a better than expected quarter, beating consensus by ~$30 million in revenues, and there was some sequential recovery observed throughout the product mix. Nonetheless, YoY results were bleak, and highlighted the exposure to COVID-19-induced headwinds to COO's end markets. Overall, CooperVision sales were the real takeout, posting ~$450 million at the top. Breaking down segments for CooperVision, we saw strength in daily disposables, which came in line with consensus, alongside the multi-focal segment, which beat by ~$2 million. The silicone hydrogel saw a 10% constant currency decline, but management have pointed to the launch of MyDay toric to help drive underlying growth in Q4, and believe there will be significant earnings improvement on the back of this. Looking at other labels in the product mix, non-daily spheres were down -12%, alongside toric contact lenses, which saw a ~10% decrease on a constant currency basis.

Speaking to the COO's other segment in the portfolio, CooperSurgical, sales of ~$130 million were driven by a decent recovery of office and surgical volumes, which scored $82 million, a 23% YoY decrease. The Insorb segment in the product mix also showed a strong recovery, which was driven by in office procedures resultant from operating room deferrals. Expanding to the fertility segment, sales declined 26% YoY, but again showed some signs of life on the back of clinic re-openings and stability in IVF cycles, particularly throughout the EU and in the US. In terms of location, Q3 growth was underscored by strength throughout the Americas, although was still down 9% YoY, and was below market performance. Weakness was also observed throughout APAC regions, and was also down 9% YoY, and well below consensus by ~$15 million.

On the margin level, gross leverage was ~66% and underscored by the cadence of CooperVision and CooperSurgical combined. However, we would point to investors that the non-GAAP margins highlighted on the earnings call exclude excess manufacturing expenses related to MiSight and other segments, in addition to ~$25 million in COVID-19 headwinds. Margins at the top-level were also impacted by US currency forex exposures, which resulted in a 2.4% headwind to revenue growth over the quarter. Management have also indicated that margin expansion may be halted on the back of increased manufacturing expenditure requirements for MyDay Torics and MiSight.

Offsetting The Near-Term Headwinds

Management have highlighted the "halo effect" from the launch of MiSight, which is a daily wear, single use contact lens, indicated in children from 8-12 years old, to slow the progression of myopia. MiSight has the potential to provide a remedial breakthrough in candidates for myopia, particularly addressing the younger age group. Management detailed an addressable market of $1.5 billion in the 8-12 year old demographic in the US alone, on a typical sale price of around $750 a year. Tucking in Europe and APAC, management are confident on a $5 billion total addressable market at that average sale price, which gives good insight into the peak sales projections for the years to come, in that segment. Management have walked us through the math behind their valuation on the earnings call.

To illustrate, ~40% of all people in the US are myopic, and management estimate the percentage of children in the ages 8-12 to have the condition, to be around 20%. With 20 million children within that age range in the US, 4 million children will develop the condition. Management therefore see a probability of ~50% of this market as targetable, which leads to the total addressable market of $1.5 billion in the US. The same logic is applied for the EU and APAC. Management expect ~$50 million in sales for MiSight over the course of 2021/2022, and the number of optometrists utilizing the technology has expanded to over 1,000, well above initial expectations. We give COO a high probability of success in this segment, and are just below management's projections in our own modeling of MiSight. Nonetheless, considering the probability of conversion, the value of this segment adds a positive skew to the distribution of returns that investors may realize over the coming periods.

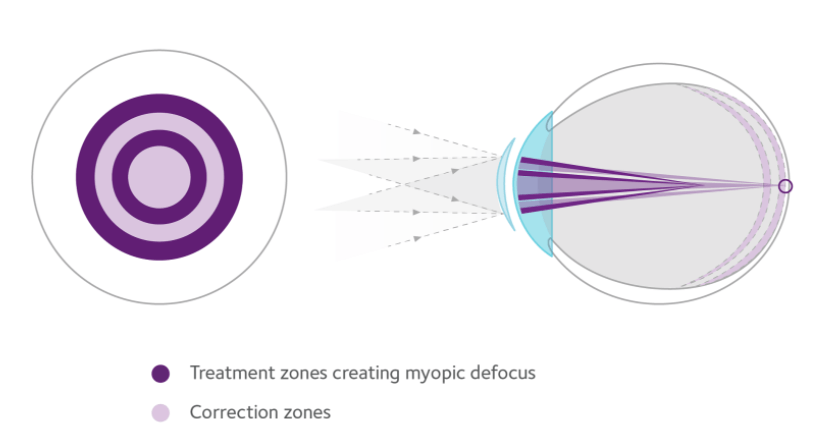

MiSight Mechanism Of Action

Data Source: CooperVision

The earnings call did give some flavor on the path to full sales recovery, however, considering performance YTD, this balances the equation. Positive recovery in the scope of contact lenses, can be drawn from children returning to school either earlier or in greater numbers than first expected by FY2020 end, which leverages COO's screening volumes and enables higher conversions from the screening process. We would anticipate to see some convergence to pre-pandemic conversion rates should schools begin to open in their entirety, both in the US, APAC and Europe, although the latter seems uncertain for the time being. Similar sentiment can be drawn from clinic re-openings, that would allow for higher utilization of current instillations, and capitalize on the rebound in procedure deferrals. We would anticipate the majority of the strength in the rebound to be driven from the APAC regions, especially as restrictions have eased drastically there, alongside COVID-19 case numbers.

Guidance and Valuation

Interestingly, Q3 performance was partially underscored by a $10 million pull-forward of restocking sales due for Q4, and this has therefore impacted guidance for Q4. Management hinted at a range of $665-$693 million for Q4, a downgrade of ~2%-6%. The breakdown of this seems to be $500 million - $520 million for CooperVision, and the rest from CooperSurgical. This extends total year sales in a range of $2.41 billion at the lower bound, which outpaces consensus estimates. The downgrade in guidance certainly reflects the pull-forward in restockings, and with additional COVID-19-related headwinds imminent in Europe and the US, low single-digit growth at the top is certainly expected.

Shares are trading at 91x free cash flow, and ~22x Q4 EBITDA, plus just under 4.5x book value. Shares do trade at a discount to peers, but with flat performance this year, one cannot align value to the discount. Shares are also trading at ~27x P/E, with ~$3.65 in free cash per share, and ~$2.60 in cash per share. In the valuation scenario, we must consider the potential asset value of the MiSight segment. Let's use management's (apparently conservative) figure of $5 billion over the coming years, which they've narrowed down to just 8-12 year olds, and excluded teenagers and other age demographics. In the interests of assumption, we'll diminish the $5 billion over the next 8 years in a straight line expenditure, to complete a DCF scenario with a discount rate of 15.2%, which is a 2x premium to COO's WACC estimates, and assuming a 75% probability of success.

Discounting the potential asset value for MiSight using this methodology gives a NPV of ~$72 per share. The company has an estimated enterprise value of $18.6 billion, meaning they hold ~$324 in EV per share. Thus, considering the current market value and asset potential of MiSight, one could assign a $396 valuation to the company using a sum of the parts ("SOTP") framework. Performing the same methodology on the $5 billion (straight line expenditure, probability of success) however with a 50% probability of success, then MiSight has a theoretical asset value of ~$43 a share, giving a valuation of $367 using SOTP. However, investors must realize that the above calculations are largely speculative, and that without additional traction to go by in MiSight, it may be better to seek multiples and the price target outlined below for a more robust valuation.

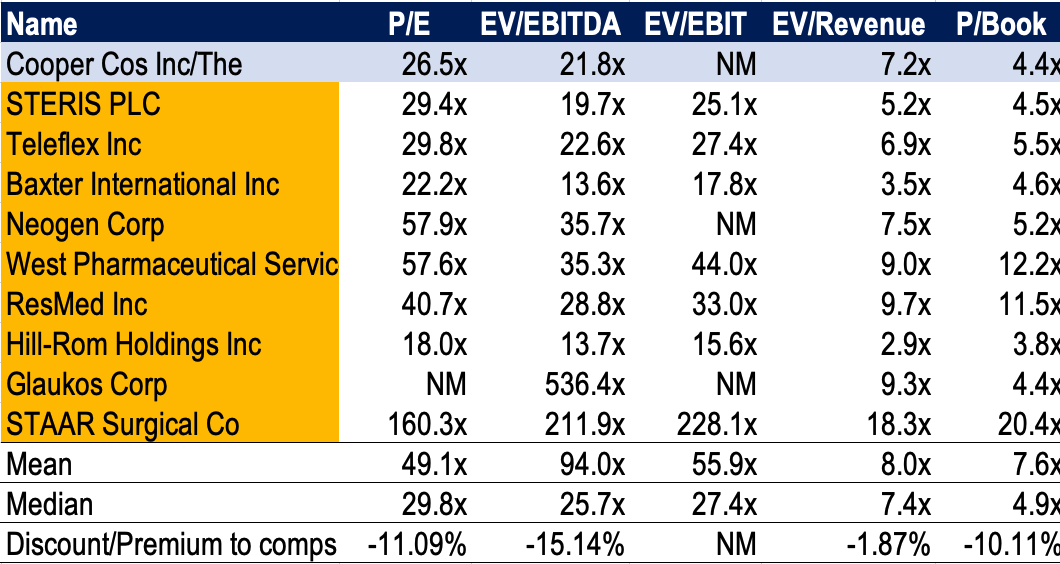

COO Trades At A Discount To Peers, But Is Not A Value Proposition

Data Source: Author's Bloomberg Terminal; Author's Calculations

From a price target perspective, assigning our 12 month P/E estimates to 2021 EPS estimates of $9.48, we see a price target of $332. Based on these calculations, we would put forward that the long-term growth aspects are already priced into the valuation. We would note that COO currently trades below the medical technology peer group median we've observed above, however, considering the company's lackluster ROIC and flat YTD, we believe this is an appropriate figure to use in terms of a price target on tangible figures, excluding the MiSight opportunity.

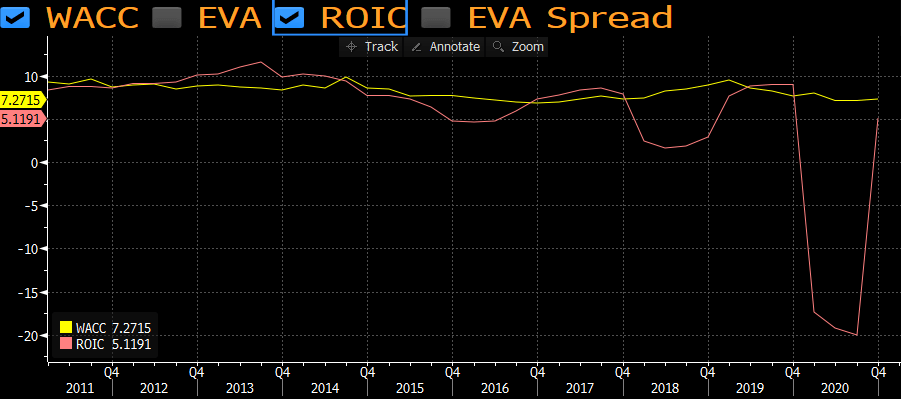

ROIC Of 5.2% Well Below Cost Of Capital (7.6%)

Data Source: Author's Bloomberg Terminal

Thus, we are happy to value COO lower than peers on a forward multiples basis, as the current bolus of information does not warrant a premium to valuation at this stage. Additionally, it would be preferable to have more traction to work with, in order to include the MiSight segment into a robust valuation framework.

In Short - Risks and Conclusion

COO has faced headwinds from COVID-19 and this has highlighted the exposure of their operations to the pandemic. Initially, it was thought that CooperVision in particular would remain immunized from the effects of COVID-19, however, reduced patient volumes and deferred clinician visits have ultimately impacted sequential growth opportunities over the YTD. What's more, this has transcended into utilization numbers at current instillations, alongside a reduction in conversions from screening programs performed at schools. What would cause a rebound in certainty is a swift recovery in the contact lens market, backed by high patient turnover and clinic visits, in addition to the early adoption of MiSight throughout key regions. This would certainly offset our neutral thesis, and add weight to the company's resilience outside of the pandemic. However, in this vein, challenges from product launches, alongside additional headwinds in the contact lens segment as a whole into 2021, would only add to the dampened sales growth this year.

Nonetheless, management are confident in a large addressable market for MiSight, alongside a recovery in contact lens and CooperSurgical business segments over the coming periods. Certainly, the case can be made as soon as COVID-19 case numbers begin to dwindle, and health authorities get a grasp on policy and legislature, that enables clinicians to return to normal practice. This will undoubtedly come in time. However, balancing this view is the variable cost margins that accompany manufacturing spend tied MiSight scale, alongside additional ~$25 million in COVID-19-related headwinds, as reported by management, over the coming periods. So investors will continue to scrutinize COO's operating leverage over the coming periods, coupled with conversion numbers from key sales drivers, such as screening programs and clinician diagnostics. Nonetheless, we see a price target of $332 on today's trading (subject to change with publication times), which further balances the neutral view of our thesis. We look forward to providing additional coverage.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.