BioDelivery Sciences: $4 Biopharma Stock Is Still A Good Bet

Today, we revisit a small biopharma concern called BioDelivery Sciences that currently trades at just under $4 a share.

The company continues to deliver robust sales growth despite COVID-19 challenges and is becoming increasingly cash flow positive.

A full investment analysis on this undervalued small-cap growth play is provided in the paragraphs below.

It has been a while since we revisited BioDelivery Sciences (BDSI). The company has seen explosive revenue growth in its core flagship product, BELBUCA, since the end of 2017. Unfortunately, that huge sales ramp-up has drawn little applause from Wall Street. This makes BDSI an incredibly cheap growth play. We update our investment thesis on BioDelivery to include our current outlook, analyst commentary and recent quarterly results in the paragraphs below.

Company Overview

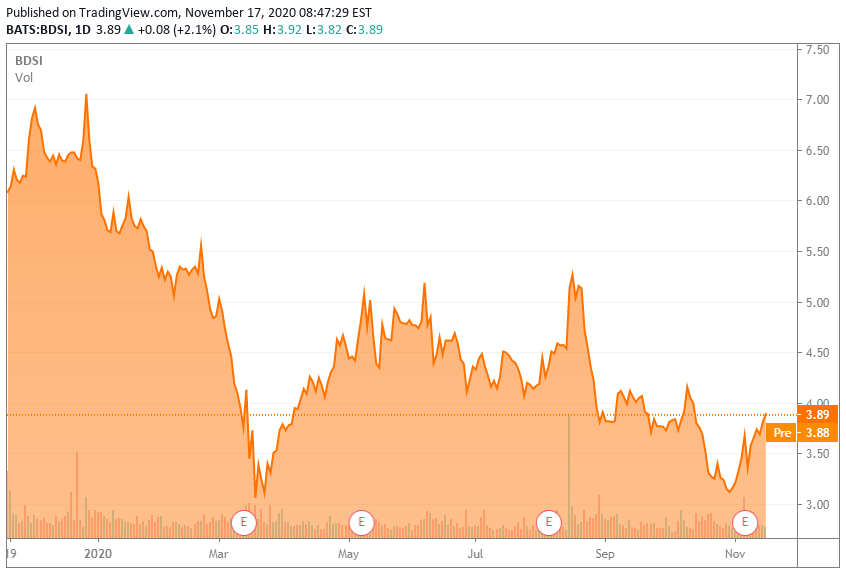

BioDelivery Sciences is a small biopharma concern out of North Carolina. It is focused on pain management, and its flagship product is BELBUCA. The compound provides pain relief and has a relatively low risk for developing dependence, which is in demand given the opioid crisis in the United States, which demands less-addictive pain management solutions. In 2019, BioDelivery picked up the rights to opioid-induced constipation med Symproic. The stock currently trades just under $4.00 a share and has a market cap just south of $400 million.

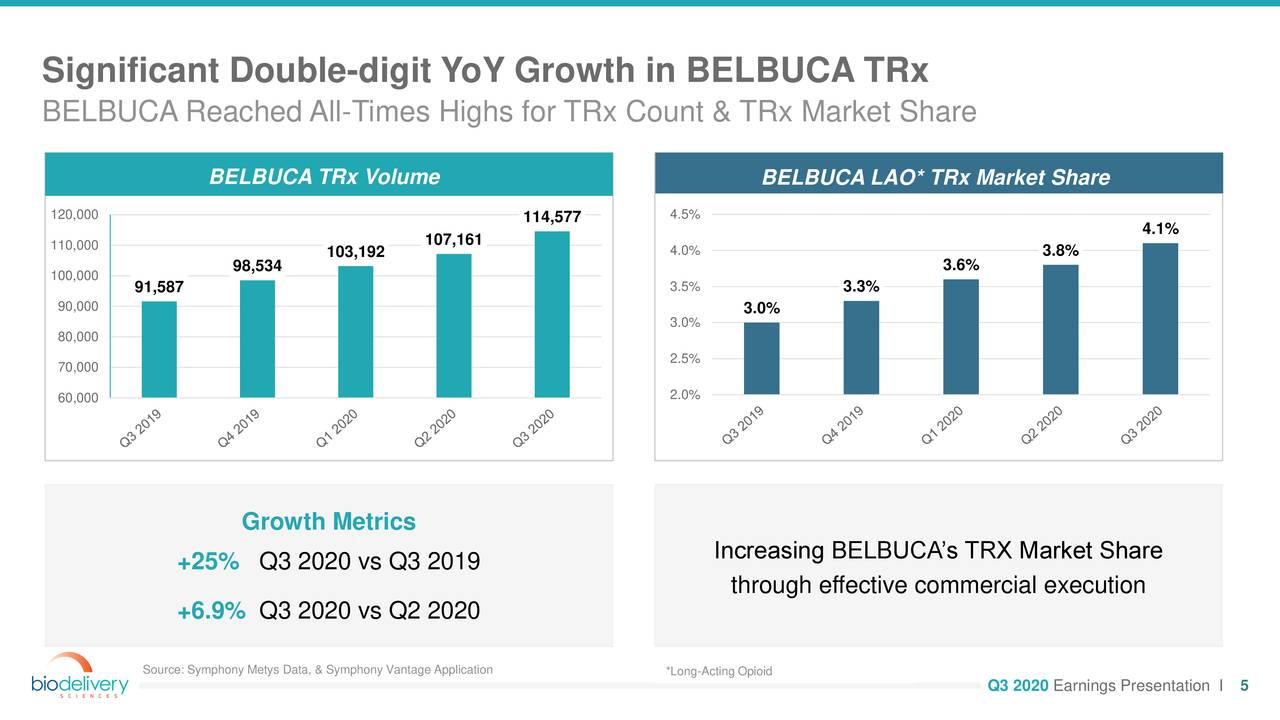

Source: Company Presentation

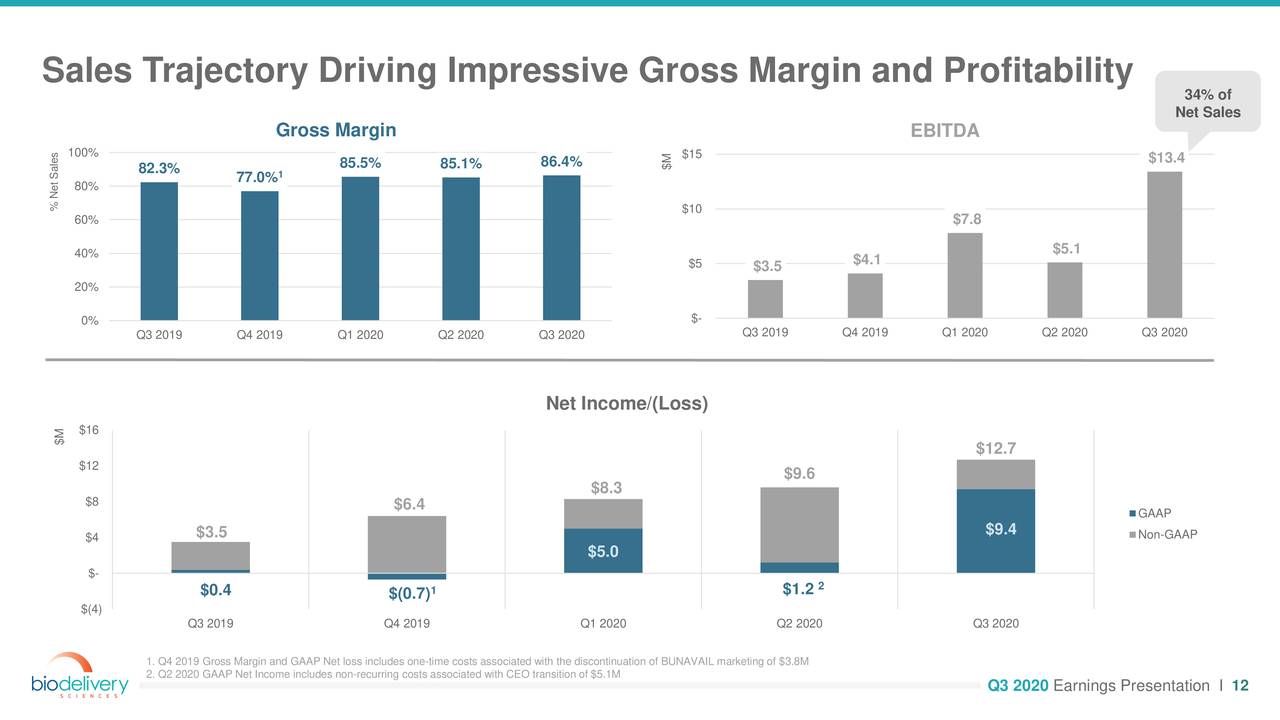

Despite the continuing COVID-19 pandemic, BELBUCA continues to deliver solid sales growth, as well as garnering an increasing market share in its niche. Earlier this month, this growth helped BDSI post earnings of nine cents a share, or $9.4 million worth of profits. This was four cents a share above estimates, and far above the $400,000 profit the company posted in the same period a year ago. Revenue growth came in at 30% on a year-over-year basis to $39.4 million.

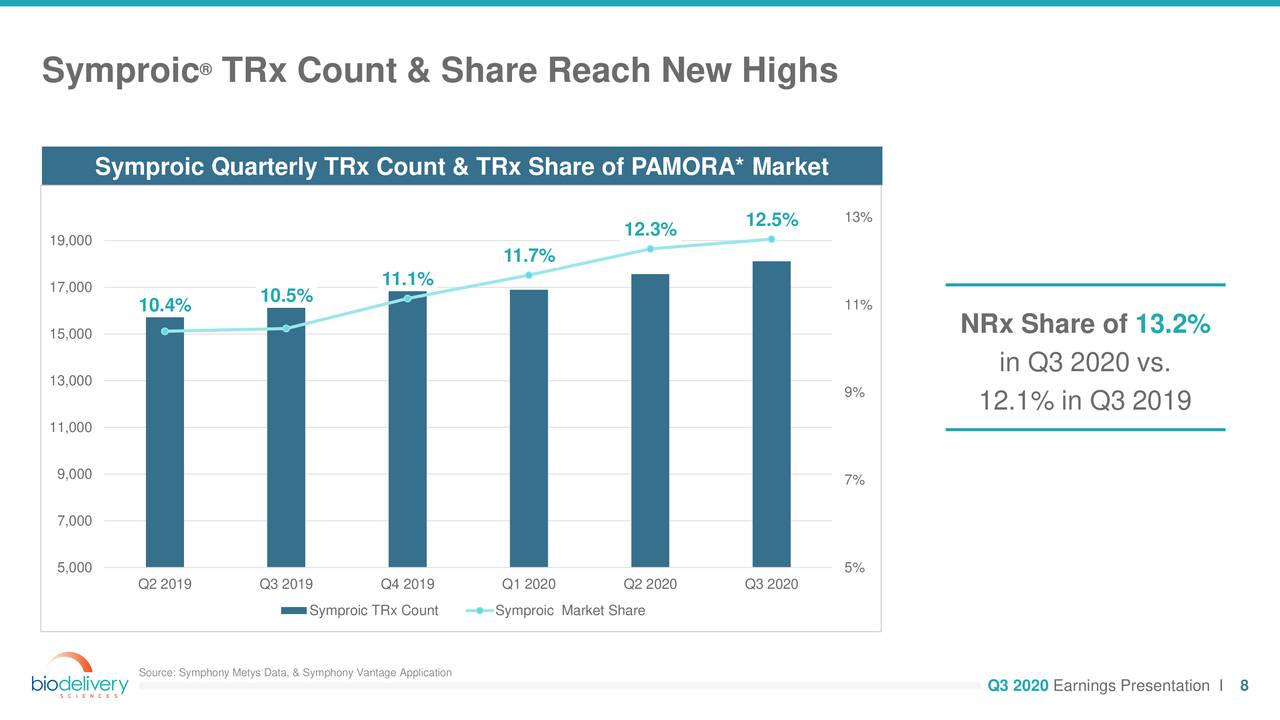

Source: Company Presentation

BELBUCA net sales came in at $34.8 million, an increase of 31% versus the prior-year period. Symproic delivered net sales of $3.5 million, which was an increase of 59% compared to the same period a year ago, as that compound also is gaining market share (see above). The company announced a new CEO during the quarter and also authorized an additional $25 million for its stock buyback program. At current trading levels, that would remove just over six percent of the outstanding float from circulation.

Analyst Commentary and Balance Sheet

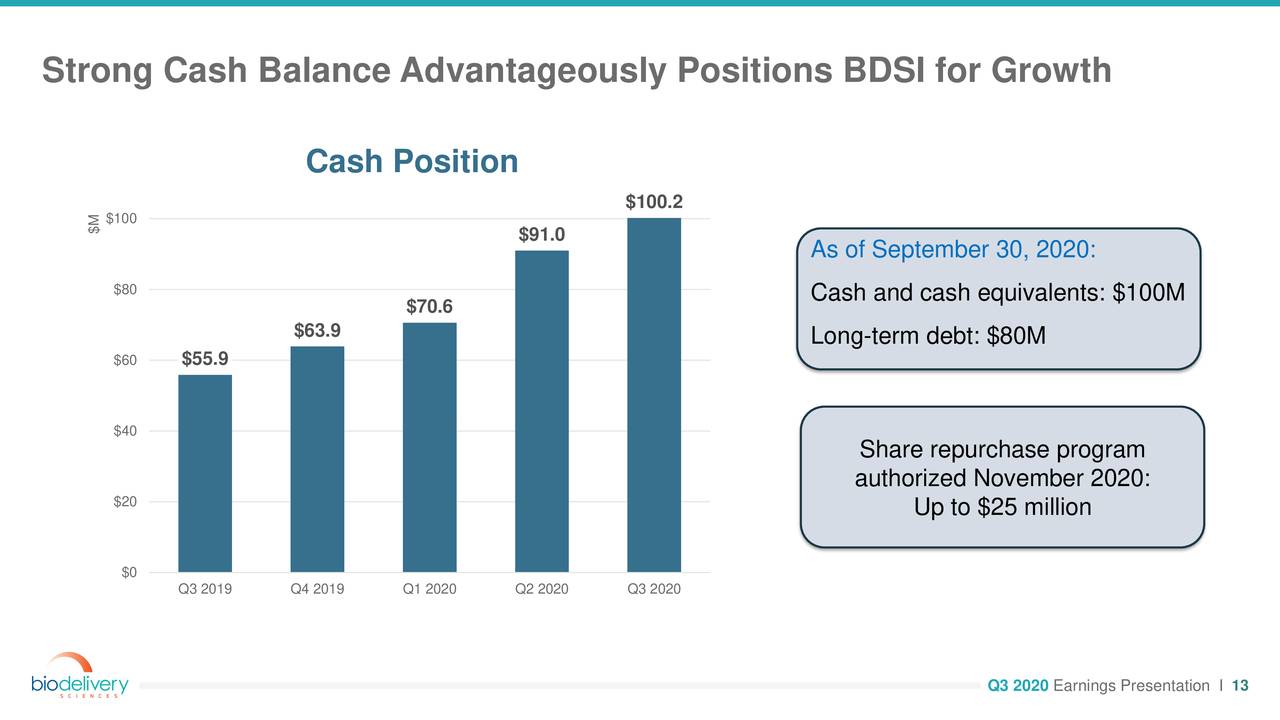

Source: Company Presentation

BioDelivery ended the third quarter with approximately $100 million on the balance flow and is just starting to produce significant free cash flow. This is showing up in improved margins and a big rise in EBITDA. The company has approximately $80 million in debt.

Source: Company Presentation

The analyst community is sanguine on BioDelivery's prospects and has a median analyst price target of $8.00 on the shares, just over twice their current trading levels. Post Q3 results, both H.C. Wainwright ($7 price target) and Northland Securities ($9 price target) reiterated Buy ratings on the stock.

Verdict

Thinks are heading in the right direction with BioDelivery. The company continues to garner market share and sales growth with both of its product offerings, despite the challenging environment of the continuing pandemic. Its balance sheet is rock-solid, and its margins and cash flow are improving significantly. The company has done a fantastic job growing its BELBUCA franchise since it reacquired the rights to this compound from previous marketing partner Endo International (ENDP) at the end of 2017.

BioDelivery's long-term risk/reward profile remains very attractive, even as the stock's performance over the past year has not reflected its improving metrics. This is why I continue to hold most of my core stake in BDSI within covered call positions.

Bret Jensen is the Founder of and authors articles for the Biotech Forum, Busted IPO Forum, and Insiders Forum.

Live Chat on The Biotech Forum has been dominated by discussion of these type of buy-write opportunities over the past several months. To see what I and the other season biotech investors are targeting as trading ideas real-time, just join our community at The Biotech Forum by clicking HERE.

Disclosure: I am/we are long BDSI. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.