Dan Bilzerian Gives Ignite Huge Boost But Troubles Continue Behind The Facade

More interesting developments at Ignite as the company delivers Q2 results.

These results confirm that Ignite is running out of cash runway and need an injection of cash quickly.

Surprisingly, Dan Bilzerian has put up the cash.

Even with this, my previous thesis remains intact - avoid Ignite.

Note: I have written about Ignite previously, investors should see this as an update to my earlier article on the company

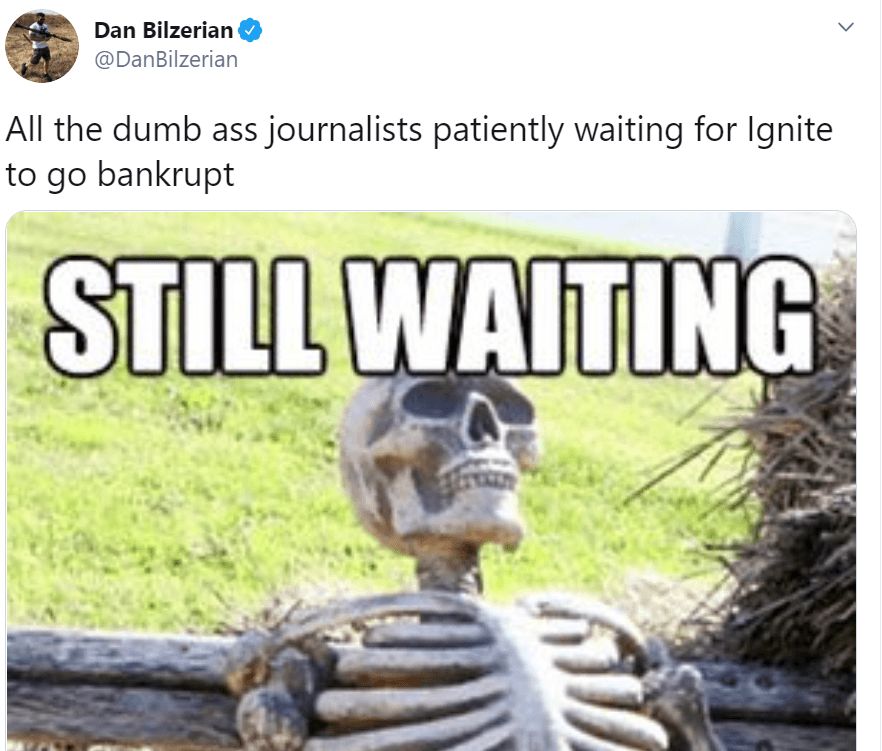

I wouldn't usually write on the same company multiple times in such a short period but the Ignite (OTCQX:BILZF) situation is very liquid right now and it appeared readers enjoyed my last article. Recent developments continue to paint a dim picture for Ignite and Dan Bilzerian who has remained eerily quiet recently on his social media platforms bar his Twitter (TWTR) account where he tweeted out a message regarding the Ignite Bankruptcy rumors:

Source: Dan Bilerzian's Twitter account

Although Dan seems to get Humor from the current Ignite rumors potentially hinting at the fact that Ignite will get through this, shares are standing at all-time lows. I have never seen a CEO less bothered about his own shareholders. This shouldn't really come as surprise though as Dan Bilzerian has primarily used shareholder money to help fuel his lifestyle through a number of capital raises for 'marketing' purposes.

Sadly for Bilzerian financial commentators and investors alike have access to something called financial statements that public companies must disclose to investors, these give us an idea of the health of Ignite at a given point in time. Well, the Q2 results were recently released and to no surprise show little improvement on previous quarters.

Q2 Results - troubles remain

For those interested, Ignite's Q2 results can be found on Sedar, these results were actually unaudited and therefore hadn't been reviewed by auditors. The Q2 results showed a dwindling cash pile for Ignite which stood at just CAD$5.8 million by the end of June. Over the previous year, Ignite has burned circa CAD$10 million worth of cash - a troubling amount. Total Stock has gone from CAD$6.1 million a year ago to CAD$8.1 million now, an increase of 33%. This means that Ignite is tying up further cash in inventory.

Some financial commentators have said that this leaves Ignite with just 6 months until they run out of cash but Ignite do have a bit longer than that as they have reduced the cash burn rate so to use the whole year as an assessment for burn rate wouldn't be a correct assessment. Comparing it to the Q1 results Ignite's cash pile has actually only decreased by CAD$0.1 million. This doesn't reflect Ignite's true cash burn rate but does suggest that the company has cut costs. Ignite mitigated the cash burn by, as you can probably guess, raising more capital. On June 9 2020 the company raised $5 million from the issue of convertible dentures (non-brokered, private placement) from International Investments limited at 10% per annum - extremely expensive debt, this will mature in June 2022. Prior to this, the company has the right to convert the amount owed into shares at $1.58 (at current prices that is looking unlikely).

To add to this spiraling debt pile, on June 12th the company issued an additional promissory note for US$3.35 million at an annual interest rate of 10%, maturing in 2022 in order to acquire the remaining balance of Ignite Distribution from International Investments Limited. Both of these agreements made with International Investments are extremely expensive debt made on unfavorable terms. In connection with the same transaction, the company issued an additional $500,000 promissory note, bearing an annual interest of 10% and maturing in December 2021 to ECVD/MMS Wholesale LLC. On June 18th Ignite received a US$500,000 loan from MMS wholesale which was converted into 443,000 shares at $1.53 a share.

In the last 6 months, the total liability for convertible debentures has risen from CAD$18 million at December 2019 to CAD $29 million on June 30th, 2020. The transactions I have laid out above don't even cover all those mentioned and undertaken by Ignite. As can be seen, this all appears like one massive game of financial chess to keep Ignite and Bilzerian's pocket full. The CFO is an extremely busy person.

However I am not too concerned for the CFO's workload as management compensation, even with the poor performance, has increased substantially. For the 3 months, management salary and bonuses were $721,000 up from $210,000 in 2019.

In other related transactions, Ignite has had to write off a bad debt from a related company Ignite Social worth $200,000. Whilst this isn't a substantial amount, I believe the principal has significance. It is the latest in a long list of related-party transactions that continue to cloud the operation of this CBD entity. I have previously highlighted in my last article many other suspicious related party transactions.

I previously covered Bilzerian and Ignite's quite ludicrous expenses in my last article and how much of it wasn't beneficial for Ignite but just to fuel Bilzerian's lifestyle. The Q2 results now provide more clarity on Ignite's property expenses. In May 2018, the company entered a 3-year option agreement that provided the option to buy a residential property, Ignite paid $5 million dollars for this option which allowed the company to buy the property at various purchase prices depending on the options exercised - Ignite was also leasing the property at this time ($200,000 a month). By the end of June 2020, the only option that remained was May 2021 to buy the house for $65 million. To opt-out of this agreement Igntie agreed on a settlement:

On July 10, 2020, the Company entered into a settlement agreement and release (the “Settlement Agreement”) with the owner of a property leased by the Company on May 27, 2018. The Settlement Agreement grants a division of proceeds relating to the Company’s Option to Purchase (note 16) for proceeds resulting from the sale of the property in excess of USD$55 million. The Company will receive the first USD$5 million above a USD$55 million sale price and an additional fifty percent (50%) of all net sales proceeds after its receipt of USD$5 million. In the event sales proceeds are less than USD$55 million, the Company will receive USD$2.5 million, which is the lowest amount to be received in a sale scenario

It is easy to forget that Ignite is a CBD company, but that also indulges in a large amount of property price speculation? To put this into perspective turnover for Ignite in the last 6 months was $4.8 million, Ignite spent more than 6 months of turnover on property speculation. Who is paying for this speculation? Shareholders.

Management also showed dissatisfaction in the company's statement made in accordance with the Q2 press release:

Though the Company’s present management is dissatisfied with the losses incurred by the Company during the second quarter prior to the internal reorganization, including John Schaefer becoming IGNITE’s President, it is pleased with the progress made in restructuring its operations to drive down operating costs, drive sales growth and improve overall financial performance.

It isn't surprising that management is 'dissatisfied' with the losses incurred which still amounted to a colossal $7 million over the period, compared to a gross profit of $865,000 - Ignite is struggling to turn the ship around. Losses were reduced from the previous quarter but only by circa $1 million, Ignite still has serious issues in trying to control costs.

Due to Ignite's extremely precarious financial position investors must give large attention to the statement of financial position and how liabilities are weighing up against assets. Particularly current liabilities which will come due within one year, these still remain substantial at $9.7 million. More specifically receivables (asset) which Ignite is owed on goods already delivered stood at $1.6 million compared to accounts payable and accrued liabilities of more than $4 million. In order to survive Ignite is going to have to restructure a large amount of these current liabilities and negotiate with lenders and partners to move them to longer-term, non-current liabilities, which will prove hard to achieve. Ignite actually deferred interest on the series A and series B convertible debentures, which was $193,000 in March and $800,000 in June. Instead Ignite has found another way to reduce this near term debt and increase cash - via Mr. Bilzerian himself.

Bilzerian buys in big

Source: insidehook.com

The matter of Dan Bilzerian running out of cash appears not to be true. On the 23rd of October Bilzerian showed intent to buy a huge 'headline' CAD$25 million worth of new and existing Ignite shares at a $0.5, a 39% premium to the closing price of the previous day. But digging deeper into the official announcement only CAD$5 million represents new cash and the remaining CAD$20 million is canceling existing debentures and liabilities ('shares for debt transaction'). So Mr. Bilzerian is purchasing these debentures from a creditor of the company and converting this into shares. This will mean Ignite receive a CAD $5 million cash boost and also deleverage their balance sheet as debt is significantly reduced. However, it is not known how much Bilzerian is spending on the debentures.

This looks to put to bed rumors of Bilzerian running out of cash and does come as a real surprise. This is a big confidence boost for shares (jumped 45% in trading) as you would presumably think that Dan Bilzerian isn't going to throw money down the drain and there, therefore, is a turnaround promise at Ignite. This will also provide Ignite with a significant cash boost giving them plenty of cash runway and more time to turn the ship - even though I do not believe they ever will successfully turn the ship around.

I believe this purchase was also done as a way of Bilzerian putting to bed rumors surrounding himself specifically and to keep his image as a 'businessman' and 'CEO' which he plays up on his social media. If Ignite was to fall apart this would significantly affect his image.

For the first time I have seen Dan Bilzerian actually made a comment on the press release too:

“As we announced last week, we project Ignite to have a profitable fourth quarter and I am very much looking forward to seeing what the Company can do in 2021, when it should be operating on all cylinders

Here Bilzerian is putting his (or investors) money where his mouth is and to that, I give credit, however, the fundamental weakness of Ignite is unchanged. I do not believe Ignite has any chance of turning a real profit in Q4 unless he aims to achieve this on a heavily adjusted basis - even then it would be near impossible from the state of Ignite currently. Perhaps Bilzerian is now a changed man and is going to completely cut expenses after exiting his mansion and will now actually focus on making Ignite a viable entity - which would make things interesting. However even then I couldn't see Ignite becoming profitable, previously all the company was known for was being Bilzerian CBD brand and he was of course known for his lavish lifestyle - if Ignite loses that there isn't much left. Ignite need to somehow strike a perfect balance of cutting costs but not losing the little traction it has - a balance that appears near impossible to reach over the long-run.

Conclusion

Maybe there is something more to Ignite than what is in the public domain. Don't get me wrong I still believe Ignite is an awful investment and would still steer well clear but Bilzerian giving his intent to buy a huge amount of shares at a premium does arise a large number of questions:

- How has he afforded this transaction?

- Are there near term catalysts that investors are unaware of that Bilzerian can see?

- Is Bilzerian purely acting recklessly?

- Are Ignite's Q4 forecasts actually accurate?

These and potentially many more are questions that we will not yet get answers to but should become more clear as time goes on. One thing that is for sure is the Ignite situation is incredibly fascinating. My previous thesis remains intact that investors shouldn't go near Ignite, even after Bilzerian's purchase. Whilst a confidence boost for investors, you can only invest based on what you see yourself and at the moment that is a company burning an incredible amount of cash with no real signs from public information that they can turnaround. The company is raising loads of cash (now primarily through debt), which will come to haunt them further down the line and is deferring interest payments as they come due. Investors can see this as 'kicking the can down the road'. Stay away from Ignite, but do stay tuned - from the sidelines.

If you enjoyed this article, make sure to hit the "Like" button, and if you want to see more coverage from me, then click on the "Follow" button at the top of the screen.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.