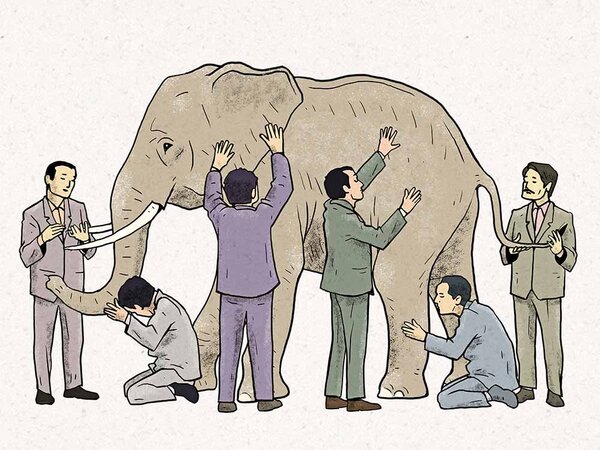

The last five months have been so confusing for most investors and certainly for most analysts that sometimes I feel that some people may just have given up on equity investing and just kept their money in the bank. Those who had just started dipping their toes into equities are likeliest to do so. Equity investing resembles the tale of the six blind men and the elephant. Every one of the blind people people touches a different part of the elephant and comes away with a different impression of what the animal is like. I'm sure you've heard the story.

This is the case even at the best of times. All of us who analyse stocks and invest in them are like the blind men. We all have a different view of what the shape of the animal called a 'good investment' is like. Some of us come across the PE ratio first and decide that's all there is to it. Others get convinced that the rate of growth of revenue is most important. Others swear on margins and so on. Some get obsessed with dividend yield. Punters think that there is nothing more to making money than to detect and react to momentum. Unlike the elephant, this animal is actually even more complex.

In normal times, most of these people sort of get along. Investing at lower valuations does tend to be an advantage. Higher dividend yield does have a positive correlation to better investments. Higher growth of revenues is definitely important.

And yet, each has a counterpoint. Valuations can be low because a company undervalued or because it's on a decline and the market knows that. Dividend yield can be high because the company is generating a lot of distributable profits, or because of some external need of the promoter. Growth is good, but it may be jacked up artificially as with so many startups. By itself, everything can be misleading. In normal times, there are always other clues that some parameter or the other can be misleading. By and large, most experienced investors can detect such clues and take evasive action.

However, at this point of time, a large proportion of the indicators can be specially misleading. There has been severe price volatility and there is now severe earnings volatility. That itself makes valuations unusually volatile. Moreover, the earnings volatility itself may have unusual characteristics. For many companies, it will recover in the foreseeable future. For others, the situation is not yet clear. Some companies will come out of it better as their competitors will be covided worse than they will be.

In the latest issue of Wealth Insight, our team has put together a 360- degree view of what is happening in the equity markets, which events and observations are relevant and which are irrelevant. Most importantly, one needs to accept the uncertainty and the lack of visibility. There is nothing exact in our actual experience as investors and analysts that has prepared us to judge the events that are happening. Perhaps we'll be better prepared for the next pandemic but right now, I can't be sure. However, we can be certain of one thing - the principles of investing will not change. The principles of business will not change. Managements which have a track record of running their companies well and sharing wealth with shareholders will continue to do so. Managements which have a track record of doing the opposite will continue to do the opposite.

As the volatility continues, we are continuously dedicated to exploring what is changing and how it will impact stocks while keeping an eye on what stays the same. In a time like this, when everyone is screaming change-change-change at every available opportunity, maintaining one's balance as an investor is the most important thing.