Highlights:

- Q3 volume growth was strong at nearly 14-15 percent

- Festive demand aided topline growth

- Management expects margins to recover in Q4

- Competitive intensity to increase going forward- Valuations offer little upside from current levels

-------------------------------------------------

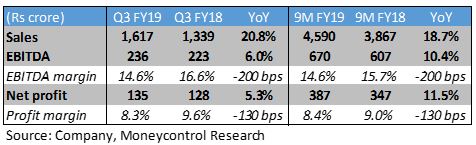

Berger Paints, India’s second-largest decorative paints company reported better-than-expected Q3FY19 topline. Volume growth was in high teens, at par with its larger peer Asian Paints. Operating margins, however, contracted as high crude oil prices expanded the cost base. The company appears to be on a secular growth path as it continues to grow faster than the industry, gaining market share from smaller and unorganised players.

Key Q3 positives

- Topline growth of 21 percent was driven by strong volume growth. The decorative volume growth estimates for the quarter stood at nearly 14 percent as strong consumer demand during the festive season along with a favourable base (timing of Diwali) aided the sales growth in October-December period.

- Operating profit margins recovered sequentially with successive price hikes partially alleviating the crude-oil and currency-related pressures. However, high-cost inventory kept margins under pressure on YoY basis.

- Apart from strong demand in the decorative business, there was decent traction in industrials, Nepal decorative business, and Saboo Coatings.

- The management expects a recovery in Q4 margins from softening crude prices and rupee stabilisation against the dollar.

Key Q3 Negatives

- Gross margins in industrial segment contracted over 400 bps to below 38 percent hitting multi-quarter low. Margins in this segment are lower versus the decorative business. However, the contraction was mostly due to delayed price hikes, high competition and lower pricing power.

- The competitive intensity remains high and could increase further as Asian Paints nears completion of its two new plants at Vizag and Mysuru. The plants will add six million kilo litre capacity to the sector and could put a cap on the pricing power of the industry for the near term.

- The demand for automotive business could taper as the outlook remains weak and the slowdown is expected to persist for at least 2-3 quarters.

Outlook

- The management is optimistic on demand in coming months and confident that recent price hikes will ease off margin pressures.

- At 47 times FY20 price-earnings multiple, the valuation multiple of Berger (CMP: 307, market cap: 29,848 crores) seems in line with that of FMCG front-runners and the sector leader Asian Paints. The current valuation seems to factor in near term positives and offers limited upside from current levels.

For more research articles, visit our Moneycontrol Research page