Oil & gas, metals to lift july-September earnings

Oil & gas

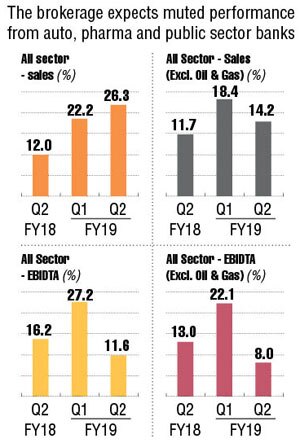

Led by oil and gas and metals, India Inc will post 26.7% sales growth in the second quarter (Q2). Aggregate margins will fall by 271 basis points, as per Prabhudas Lilladher

13.6% – Expected adjusted profit after tax

18.3% – The same in previous quarter

13.2% – A year ago

SECTOR SNAPSHOTS

SECTOR SNAPSHOTS

Automobiles

(On-year change)

28% - Fall in PAT

11% - Revenue growth (excluding Tata Motors)

117 bps - Fall in Ebitda margin

Cement

Earnings expected to grow in single digit due to weak margins

Consumer

11.8% - Sales will increase

13.3% - Jump in PAT

36 bps - Margin expansion

IT

0.7-3.5% - Constant currency revenue growth quarter on quarter (QoQ)

30 to 150 bps - Ebitda margins will improve QoQ